Moody’s RMS North Atlantic Hurricane Models: Five Reasons Why Version 23 is the Right Model to Navigate a Challenging Market

Julie Serakos

Jeff WatersSeptember 27, 2023

Earlier in 2023, Moody’s RMS® released a new version (Version 23) of its North Atlantic Hurricane (NAHU) Models. This model suite was released in time to assist the U.S. insurance industry in Florida, the coastal U.S. states, and the broader North Atlantic hurricane domain in addressing the significant challenges they face.

Within the U.S., market disruption is significant, with both insurance and reinsurance availability and affordability driven by the changing risk profile for hurricane risk.

At a time when the market needs a current, reliable, certified, and complete view of hurricane risk, we believe the latest Version 23 hurricane models are timely.

Current State of the U.S. (Re)Insurance Market: Focus on Florida

The property (re)insurance market is in a constant state of evolution, and the management of hurricane exposure and overall catastrophe risk are major influencing factors.

In recent years, a combination of exposure growth, inflationary trends, regulatory constraints, social inflation, and hurricane losses such as from Ian in 2022, has reshaped and hardened the Florida market. It has tested the resolve of insurers, reinsurers, and insurance-linked securities (ILS) investors alike.

Since 2021, seven carriers have gone insolvent in Florida, four carriers have announced plans to withdraw from the state and 15 have placed moratoriums on new business. The increased cost of risk and the inability to have premiums keep pace with this increased cost is a major contributor to this exodus.

Florida recently surpassed California as the state with the largest volume of non-admitted policy premiums, i.e., premiums from carriers that are not subject to the same regulations of rate and form as admitted carriers.

In addition, Florida’s Citizens (the insurer of last resort, where policyholders go when no carrier will insure them) has doubled their policy count over the past two years and currently has 1.4 million policyholders.

This figure is projected to grow to a sizeable 1.7 million policyholders (over 50 percent market share) by the end of 2023, and despite depopulation efforts, this is the largest number of Citizens policyholders since its creation in 2002.

From the reinsurer’s perspective, according to the Guy Carpenter Catastrophe Price Index, catastrophe reinsurance prices are at their highest levels since 2000, putting additional pressure on insurers to keep up with the expense in rate filings.

The current state of the Florida insurance market is a direct result of several factors including claim severity impacted by litigation and the previous Assignment of Benefits (AOB) language, affecting nearly 20 percent of all claims since 2017 (Irma and Michael included) according to Moody’s RMS research.

Compared to claims without influence from AOB and/or litigation, claim severity can increase up to three times for AOB and up to 100 times for claims that go through litigation.

In addition, rising inflation-related expenses place additional pressure on reconstruction costs and can prolong repair and recovery efforts.

Collectively, these costs all impact the size of claims and Moody’s RMS has estimated that modeled losses are impacted by as much as one and a half times due to the inflationary trends alone.

The combined impacts of all these factors have strained the ability of carriers to manage risk effectively – and remain in business, despite recent reforms and legislation aimed at stabilizing the market.

The market needs stability and confidence in defining its risk exposure, especially when the next hurricane happens. This is why we believe the current Moody’s RMS North Atlantic Hurricane Version 23 models are the right models to meet the challenges that the market faces today.

Here are five reasons:

1. Version 23: Latest View of Hurricane Risk in the Market

For our new Version 23 release, we made major investments into model science, informed by a wealth of new data and learnings from recent events.

This includes insights from over US$6.5 billion in new, detailed claims data from storms in the last ten years, new insights gained from in-person Moody’s RMS reconnaissance efforts for storms such as Ida (2021) and Ian (2022), and new research from organizations like the U.S. Federal Emergency Management Agency (FEMA) and the Insurance Institute for Business and Home Safety (IBHS), including the latest updates to the IBHS FORTIFIED program.

We have updated nearly all model components in some capacity, notably event frequencies, hazard, vulnerability, and post-event loss amplification.

By far the biggest area of investment and driver of change is the vulnerability component, with a scope that reflects the most comprehensive update since 2015.

It reflects not just the new data and research, but also recent legislative changes in Florida, including the adoption of a new vintage of the Florida Building Code (2020) and new legislation (Florida Senate Bill 4D) affecting the definition and applicability of the 25 percent roof replacement rule.

Other enhancements to this part of the model include damage relativities across different building characteristics and regions, updates to the building inventory database, and the choice of secondary modifiers, expanding the number of unique damage curves within the model to more than 2,800.

This expansion thus provides the means to capture, select, and differentiate risk with more granularity than ever before.

2. Version 23: Most Validated Hurricane Model in the Market

Moody’s RMS North Atlantic Hurricane models have a proven track record of reliably representing hurricane risk.

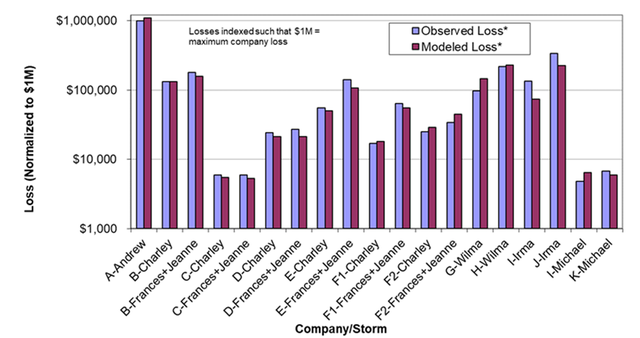

For the latest version, modeled losses are well validated against more than 175 portfolio-event combinations across residential, commercial, and industrial lines spanning more than 30 years (see Figure 1 for a comparison as shown in the latest Moody’s RMS FCHLPM submission document).

For the events shown in Figure 1 below, Version 23 modeled losses compared to client-observed losses are within three percent.

Figure 1: Comparison of modeled losses to incurred losses for Florida residential portfolios and events. Losses are normalized such that the maximum actual loss equals US$1,000,000.

* Losses include demand surge but does not include loss adjustment expense.

The models also validate well against overall industry losses. In total, modeled losses are validated against aggregate industry losses totaling more than US$700 billion in trended losses and spanning more than 40 years, including more than 30 key historical storms since 2004-2005.

Using historical reconstructions within the model itself, modeled industry loss estimates are within 10 percent for the recent hurricane events (2016-2020).

With a proven record of validating against both client-specific losses and aggregate industry losses, Moody’s RMS North Atlantic Hurricane Models provide the most reliable view of hurricane risk in the market.

3. Version 23: Certified by the Florida Commission on Hurricane Loss Projection Methodology

As of June 2023, Version 23 is certified by the Florida Commission on Hurricane Loss Projection Methodology (FCHLPM) and is available for more than two years until November 2025, providing stability for the market to use for business planning and rate making.

The models have been consistently and reliably certified for more than 25 consecutive years (since 1997), giving confidence to (re)insurers in using the latest view of risk for each hurricane season.

Moody’s RMS certification applies concurrently to Version 23 on both RiskLink® and Risk Modeler™, whether our clients use the model on-premise or on the cloud-native Intelligent Risk Platform™.

Moody’s RMS remains the first and only vendor to earn FCHLPM certification status simultaneously on multiple platforms, providing the market with the most choice in how the certified model is accessed and consumed. More information can be found here.

4. Version 23: Most Complete View of Hurricane Risk in the Market

Coupled with Moody’s RMS U.S. Inland Flood HD Model Version 1.2, our hurricane models provide a means to quantify a complete expression of hurricane risk – including wind, storm surge, and tropical cyclone precipitation-induced inland flood.

However, there are other factors that contribute to hurricane risk, including various non-modeled sources of loss and the effects of a changing climate.

Our models are the only ones in the market to offer the flexibility to test assumptions on how these factors may influence actual loss outcomes in a seamless manner.

a) Non-modeled Sources of Loss / Post-Event Loss Amplification: Dynamic and uncertain factors play into claim severity – such as the effects of recent legislation in Florida on reducing the impacts of litigation, or short-term volatility in construction costs.

These factors are quite uncertain at the time of an event and may not have been fully included in the models.

Version 23 includes flexibility to develop a more complete view of risk directly within our model framework.

This includes new analysis functionality to adjust for non-modeled sources of loss and to reflect your own view of Post-event Loss Amplification (PLA) due to economic demand surge, claims inflation, and super-cat effects.

b) Changing Climate Impacts: Portfolio management would not be complete without accounting for the future risk that is brought into a portfolio from the policies and treaties written and held today.

Policyholder or cedent relationships held for 5-10 years will bring future risk into the portfolio and prudent portfolio management suggests it should be accounted for today.

To gain insights into the explicit effects of climate change on hurricane risk profiles (including Florida), we offer climate-conditioned event rate sets (wind) and hazard sets (storm surge) that are completely aligned with Version 23 North Atlantic Hurricane Models and easily adopted into existing portfolio management workflows.

Climate-conditioned views of risk are also available for Moody’s RMS U.S. Inland Flood HD Model to quantify the impacts of climate change on precipitation frequency and intensity for both tropical cyclone and non-tropical cyclone inland flooding.

Together, these tools allow for sensitivity testing of wind, sea-level, and precipitation risk profile (frequency, severity, loss, and/or uncertainty) changes attributed to the changing climate.

These views support stress test requirements, business planning, portfolio management, and overall plans for the utilization of capital, both by insurers and reinsurers.

This is especially important as carriers and reinsurers alike aim to build the most stable and profitable portfolio of policyholders and cedants, respectively, considering the future risk they are taking on today is important now more than ever.

5. Version 23: Latest Industry Views of Risk

The latest Version 23 release not only updates the hurricane models. Similar advancements have been incorporated into our Industry Exposure Database (IED).

This database reflects a comprehensive update based on the latest building footprint data to estimate building stock, updated replacement cost per square foot to estimate overall exposure, updated insurance assumptions, and the latest inflationary trends affecting replacement costs of properties.

These updates ensure Moody's RMS IEDs and resulting Industry Loss Curves provide a current view and appropriate distribution of insured exposure in the U.S., supporting ongoing market share and risk assessment needs throughout the market.

In summary, the Florida and broader U.S. coastal insurance market is likely facing its biggest challenge due to the complexities of managing the changing dynamics of hurricane risk.

At Moody’s RMS, we develop the most reliable models that offer the ability to explore the depth and breadth of risk complexity, testing and reshaping portfolio management plans.

Our Version 23 North Atlantic Hurricane Models can help (re)insurers to confidently address these challenges through the most reliable, certified, current, and complete view of hurricane risk, and allow for informed business decisions so that the market can move into a period of stability.

For more information on the latest Version 23 models, click here.

Senior Vice President, Head of Model Product Management

Julie is Senior Vice President and Head of Model Product Management, responsible for global model product management across all climate, climate change, earthquake, and emerging risk models. Julie also oversees global government and regulatory affairs.

She brings over 30 years experience of working for reinsurance brokers and joined Moody's RMS from BMS Re where she led the catastrophic analytics team for over ten years, providing catastrophe analytics for reinsurance design, pricing, and marketing. Prior to this, Julie spent 14 years at Willis Re as Executive Vice President in various catastrophe management roles.

Julie is currently an Executive Director with the International Society of Catastrophe Managers where she chairs the Credentials Committee. She oversees the development of the Certified Specialist in Catastrophe Risk (CSCR) and Certified Catastrophe Risk Management Professional (CCRMP) exams, and Experienced Industry Professional Pathway (EIP) application reviews.

Staff Product Manager, Model Product Management, Moody's RMS

Jeff Waters joined Moody's RMS in 2011 and is based in Bethlehem, PA. As part of the Product Management team, he is responsible for product management of the Moody's RMS North Atlantic Hurricane Models.

Jeff provides technical expertise and support regarding catastrophe model solutions and their applications throughout the (re)insurance industry. He also generates product requirements for future updates and releases, and helps develop the overall product strategy, messaging, thought leadership, and collateral to ensure its commercial and technical success.

Waters’ background is meteorology and atmospheric science with a focus in tropical meteorology and climatology. Jeff holds a B.S. in Geography/Meteorology from Ohio University (’09), and a M.S. in Meteorology from Penn State University (’11). He is a member of the American Meteorological Society, the International Society of Catastrophe Managers, and the U.S. Reinsurance Under 40s Group, Inc