Major Hurricane Idalia: Risk Pricing Needs to Reflect Property Vulnerability

Oliver SmithSeptember 25, 2023

Hurricane Idalia made landfall as a Category 3 hurricane on August 30, 2023, near Keaton Beach, Florida, bringing with it damaging winds, heavy rainfall, and a devastating storm surge.

Now with Idalia, this is the fourth consecutive year that a major (Category 3 or greater) hurricane has made landfall in the U.S., and it was also the first major hurricane to directly impact Florida’s Big Bend region in over 125 years.

While very few individuals in the insurance market would push the argument that anywhere in Florida is low risk from a hurricane perspective, the lack of observed event history is often confused as representing little or no risk.

Idalia serves as an important reminder of the devastating impacts that natural catastrophes can have, even in previously largely unaffected areas. It also illustrates the importance of using analytics that can consider a full spectrum of possibilities.

No Single Building is the Same

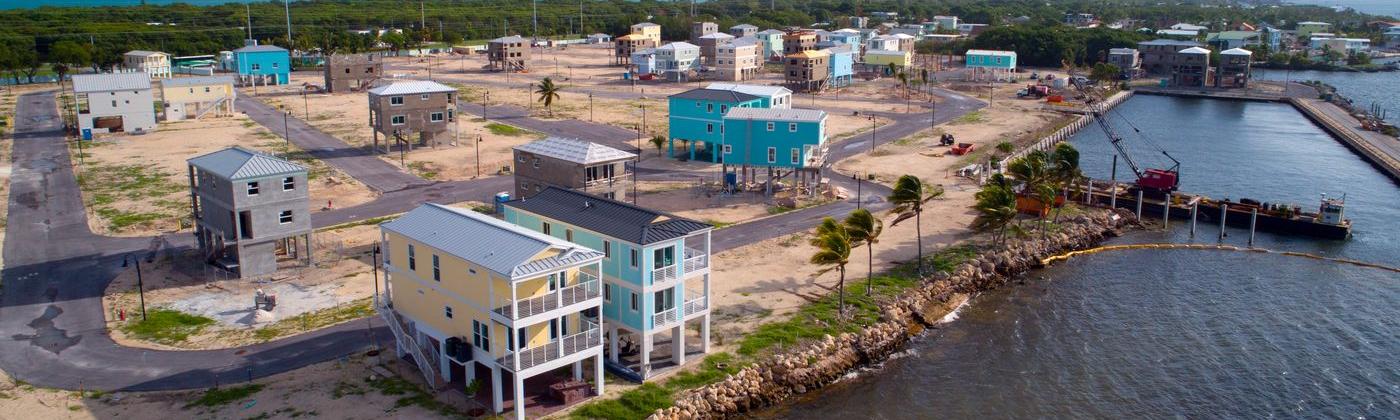

When exploring some of the worst affected areas along the northwest Florida Gulf coast, and towards the lower end of the Big Bend, including Keaton Beach, Cedar Key, and Horseshoe Beach, I was struck by the significant variability in building stock from property to property.

In one example, a residential wood-frame property resembling a treehouse-like structure would be elevated 10 feet (3.08 meters) above the ground on pile foundations, while next door there would be a property firmly built at grade.

In another example, an older-looking property with signs of distress to the roof would stand next to a property erected in the last few years built to the latest design standards, and equipped with shutters.

When exposed to maximum sustained winds greater than 125 miles per hour (201 kilometers per hour), or nine feet (2.7 meters) of storm surge such as with Idalia, variations between structures in terms of their age or their type of construction will matter greatly, as they will respond very differently.

For carriers using underwriting tools that are primarily or solely based on hazard metrics, there is the risk of being out-selected and exposed to adverse selection compared to carriers that use more insightful metrics that consider the implications of different building stocks.

An individual location’s susceptibility, whether from wind or surge or any other natural peril, will vary significantly based upon the attributes of the location even when exposed to the same hazard. Carriers that ignore this susceptibility will not get the full risk picture.

To ensure price adequacy on every policy, underwriters need to consider these characteristics and the implications they have on the premium required to cover the technical risk of a specific peril.

Applying Data-Driven Insights to the Underwriting Process

Catastrophe risk models have been used as a critical tool for the insurance industry to reflect these vulnerability differences and have been used for portfolio management and underwriting of complex risks for decades.

However, for point-of-quote decisions focused on the more commoditized side of the business, the use of risk model data has been seen as a major challenge.

Requirements around the speed of response and the need for integration into existing quoting systems for insurers writing homeowners and small commercial business has resulted in greater reliance on internal and third-party hazard metrics.

To address these challenges Moody’s RMS Location Intelligence API provides location-level loss data, with sub-second data responses that can be integrated into existing quoting systems.

It enables insurers to complement their internal expertise and benefit from utilizing key property characteristics – often already known – to tailor individual quotes for risk-specific decisions.

Available for all major cat-perils, Location Intelligence can be used by U.S. nationwide property underwriters managing all-perils policies, through to California earthquake or private flood market writers.

The tool leverages the same science that underpins our best-in-class probabilistic models to ensure consistent risk decisions across the risk lifecycle.

Here are two examples of the differences that Location Intelligence and its risk model data can make for insurers:

Example 1: Affected Location in Cedar Key, Florida

The impact of Idalia on the two properties pictured in Example 1 above immediately illustrates the importance of being able to make refined, location-level decisions. While both have exposure to surge hazard, the risk potential differs significantly between the two locations.

Both properties may have been assessed similarly but in the absence of considering such detail, the possibility for declining potentially ‘good’ risks, or not getting adequate premium on ‘bad’ risks is increased.

Using the Location Intelligence API, underwriters can instantly fine-tune risk pricing and adjust premiums accordingly, with the property on the right needing over twenty times the premium to cover the technical risk of flooding.

Example 2: Affected Location in Horseshoe Beach, Florida

Example 2 above shows two property locations with similar challenges in Horseshoe Beach. The top two images provide a ‘before’ and ‘after’ the storm view, while the two locations highlight those same properties.

It will be difficult to determine whether wind or surge was the proximate cause of the property’s destruction, but it acts as another example of the importance of accounting for key characteristics like the presence of shutters, and the condition of the roof.

Despite being exposed to the same windspeeds, the location destroyed would require nearly ten times the premium to cover the technical risk of wind risk.

Underwriting in Hardening Market Conditions

With the current hard market conditions, it is perhaps more critical than ever to make the most effective risk selection and pricing decisions.

According to Moody’s, an increasing number of insurers expect to purchase less reinsurance coverage for 2024 as a result of higher costs.

This, in turn, will result in primary insurers retaining even more risk, with the potential for increased volatility.

Considering these market dynamics, it is of paramount importance to leverage tools that help to limit the volatility in retained risk, provide greater control of location-level decisions, and improve predictability with modeled results and onward cost of reinsurance that is purchased.

Location Intelligence API helps to tackle the disconnect between how locations are selected and priced and how those same locations translate into portfolio modeling results and enable consistency across the insurance risk life cycle.

Consequently, this also enables reduced volatility in losses, greater control, and improved predictability during onward reinsurance purchases.

To find out more about Location Intelligence contact sales@rms.com or visit the Location Intelligence web page here.

Gain better underwriting perspective with instant…

Learn More

Oliver Smith

Senior Product Manager, Data Product Management

Based in London, Oliver is a Senior Product Manager within the data product management team, responsible for overseeing the development and release of RMS data offerings across multiple peril regions and delivery vehicles. Oliver joined RMS in 2013 and has held roles in the Global Knowledge Center and Model Product Strategy teams prior to joining Product Management in 2016. Oliver is a Certified Catastrophe Risk Analyst and holds a bachelor's degree in Economics and Finance from Keele University.