UnderwriteIQ: Unleash the Power of Marginal Impact Analysis for Optimal Risk Assessment and Greater Profitability

Alisha FazoJune 30, 2023

I am excited to share that integrated marginal impact analysis is now available within the Moody's RMS UnderwriteIQ™ application. Marginal impact analysis helps insurers to identify higher-risk policyholders who may require revised premiums or additional risk management measures.

By incorporating marginal impact analysis assessment, underwriters can more effectively allocate resources, minimize potential losses, and optimize profitability of their underwriting portfolios.

One method of conducting marginal impact analysis for an insurer’s portfolio is to first design a notional cat risk portfolio that simulates the catastrophic events that an insurer may potentially face and then incorporate the various risk factors associated with those catastrophe events.

By using the UnderwriteIQ application on Moody’s RMS Intelligent Risk Platform™, users can then evaluate multiple reference portfolios, which can represent either notional or booked portfolios.

Both types of reference portfolios – notional or booked – serve different purposes in the analysis and management of insurance underwriting and investment activities.

The booked portfolio represents the actual contracts and obligations, while the notional portfolio is a theoretical construct to represent the average risk level based on historical data, industry norms, or specific underwriting criteria.

Analyzing Marginal Impact with UnderwriteIQ

Underwriters using UnderwriteIQ will be able to analyze the marginal impact of changing individual risk factors in their risk profile by simply adjusting the parameters of their notional portfolio, such as increasing or decreasing exposure in specific regions, or by modifying coverage terms to measure the incremental effect on the insurer’s overall cat risk exposure, losses, and profitability.

This marginal impact information can then be used to refine underwriting guidelines, adjust pricing and coverage terms, optimize reinsurance strategies, and implement risk mitigation measures.

One of the many benefits of Moody’s RMS catastrophe modeling applications such as UnderwriteIQ being on the Intelligence Risk Platform is the availability of unified and interoperable data, which allows different functions across an insurance business to work on the same data set.

For instance, portfolio managers can use Moody's RMS Risk Modeler™ application to roll up their latest booked accounts as frequently as needed.

The latest booked portfolio analyses are then enabled within the marginal services function within UnderwriteIQ, so underwriters would immediately know when their capacity limits are reached.

UnderwriteIQ also unlocks new risk insights and opportunities for growth by leveraging cloud-native services on Moody’s RMS Intelligent Risk Platform, such as the unified data store, shared vulnerability assessments, and model versioning.

Users benefit from:

Real-time portfolio insights: Underwriters can understand the impact of adding new pre-bind risks to the most current view of the book of business.

Reduced business volatility by using the corporate view of risk when analyzing new risk: The use of analysis templates ensures underwriters run the right view in their workbench.

Governed access to the right set of portfolioswithin a single model run: Underwriters can analyze the impact of adding pre-bind policies to multiple reference portfolios within an analysis template, to prioritize their assessments, and streamline the underwriting process.

Robust insurance analytics: Share the same insights as your catastrophe modeling, such as Aggregate Exceedance Probability (AEP), Occurrence Exceedance Probability (OEP), and Tail Conditional Expectation (TCE) for AEP and TCE-OEP, and statistics such as Average Annual Loss (AAL), Coefficient of Variation (CV), and Standard Deviation (SD) at account and policy level resolution. Using the same insights makes it easier to identify high-risk policyholders who may require revised premiums or additional risk management measures.

Marginal Analysis Within an Ecosystem of Cloud-Native Risk Applications

Critical to the marginal impact analysis workflow is a tight collaboration between the UnderwriteIQ application and Risk Modeler, our cloud-native catastrophe modeling application. Marginal analysis within UnderwriteIQ is designed to deliver a fast and intuitive experience for an underwriter.

But underneath the hood is an advanced technical architecture that enables the catastrophe modeling team to build a unified view of risk that aligns technical underwriting with the overall business objectives.

This can be accomplished because UnderwriteIQ and Risk Modeler share the same exposure data, model settings, financial model, and analytical engines.

Let’s look at how this can be done today:

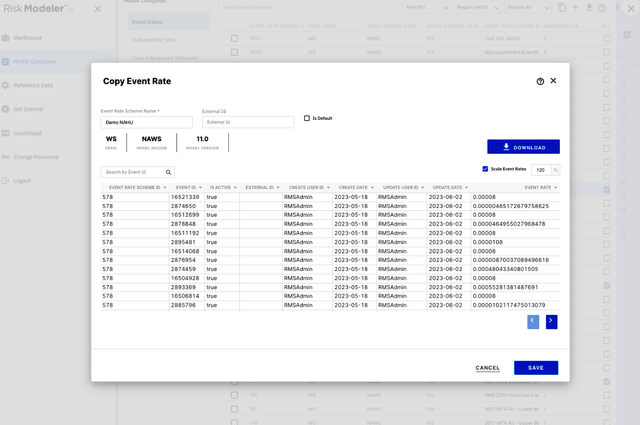

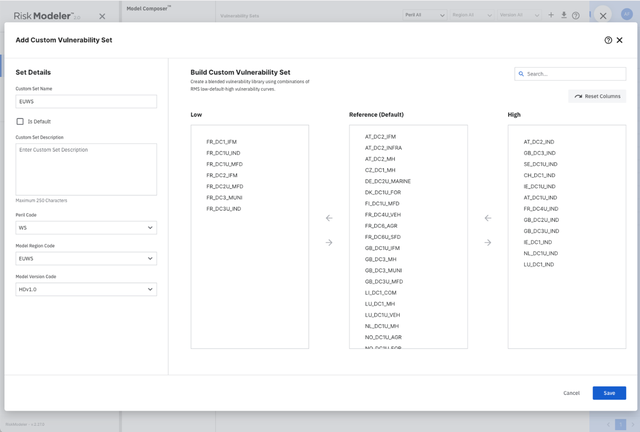

Step 1: Catastrophe modelers can either use Model Composer in Risk Modeler to create a customized corporate view of risk, to adjust model parameters like the model version, event frequencies, and vulnerability damage curves or can use the Moody’s RMS recommended model settings and create model profiles within UnderwriteIQ.

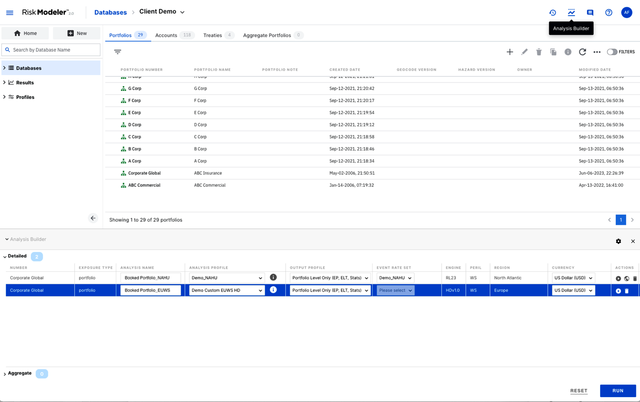

Step 2: The model profile is then executed against a portfolio, generating model portfolio results into the Intelligent Risk Platform’s unified loss store. These portfolio results are instantly integrated into UnderwriteIQ as the reference analysis.

For clients who do not license Risk Modeler, portfolio results from other applications can be manually uploaded from Results Data Modules (RDMs).

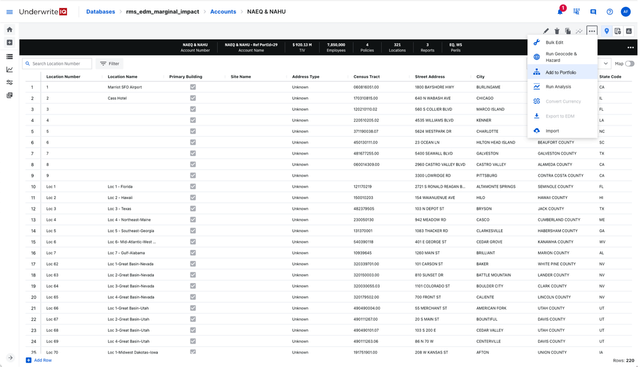

Figure 3: Booked portfolio individual model analysesFigure 4: Latest booked portfolio roll-up for reference analysis

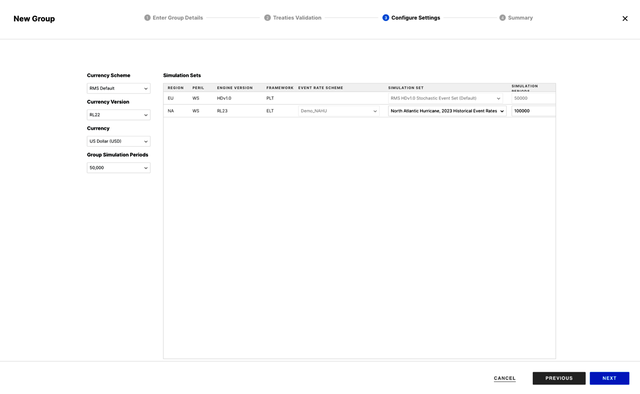

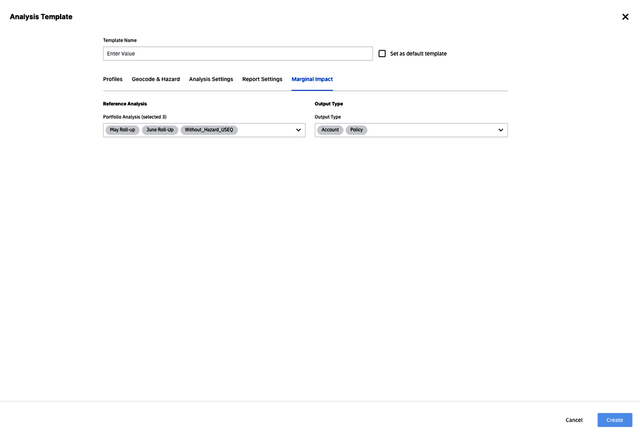

Step 3: Using UnderwriteIQ, catastrophe modelers can then build an analysis template based on the model profiles or use one created in Risk Modeler. Within the analysis template, you can select up to 15 reference analyses for the underwriter to evaluate pre-bind policies against.

Figure 5: Configuring selected customized views of risk at the point of underwriting

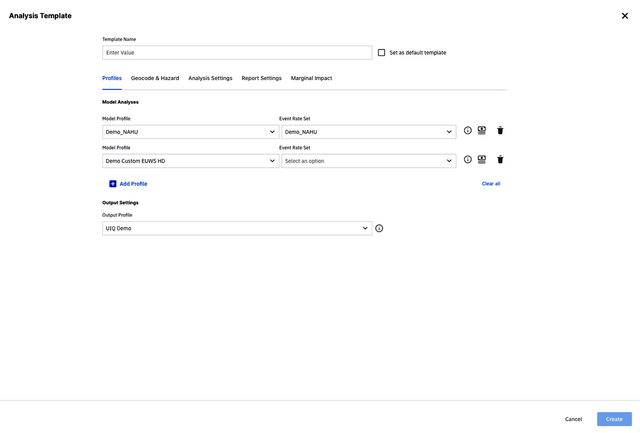

Step 4: When pre-bind policies or accounts are encountered on the underwriting workbench, underwriters can choose an analysis template to assess the associated risk. The analysis template will already contain the relevant portfolios reference analyses.

Figure 6: Configuring marginal settings with the latest reference analyses

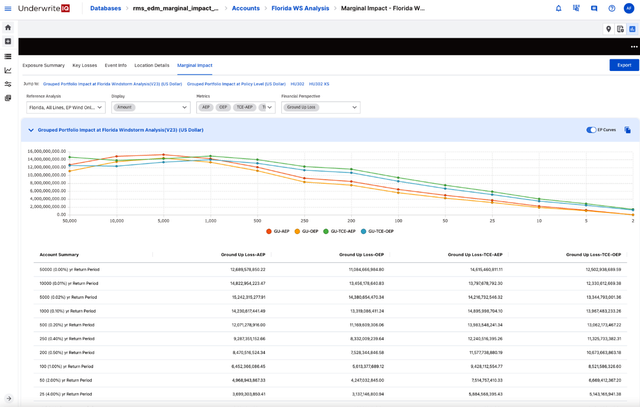

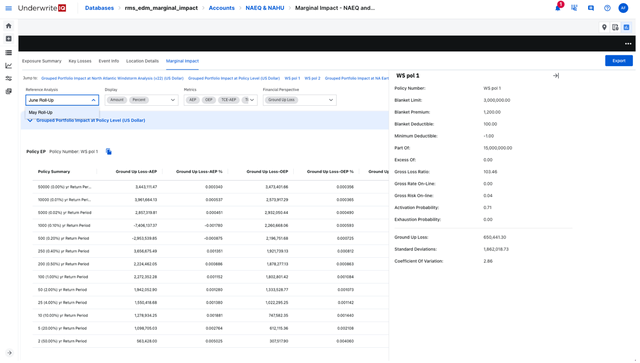

Step 5: The UnderwriteIQ application generates a marginal impact analysis report, presenting exposure analytics from all the selected reference portfolios.

Figure 7: Analyze impact across multiple reference analysis at policy level

Step 6: If the pre-bind policy meets the underwriting guidelines, underwriters have the option to bind the policy. Once bound, the portfolio is automatically updated across all applications, including Risk Modeler and the TreatyIQ application.

Step 7: The portfolio manager can add the newly bound policy, allowing them to analyze the portfolio and make any necessary adjustments.

Figure 8: Add Account into Booked Portfolio

Conclusion

The completion of the marginal analysis workflow highlights a new era of efficiency and empowerment for underwriting, catastrophe modeling, and exposure management teams.

The Intelligent Risk Platform's data architecture emerges as the linchpin, enabling firms to traverse the entire marginal impact analysis workflow across multiple teams and systems with impressive speed and scalability.

Within just a few short hours, from catastrophe modeling to underwriting to portfolio management, the process can be accomplished, with the marginal impact analysis reduced to just a few minutes.

Whether clients license the suite of applications hosted on the Intelligent Risk Platform, or integrate UnderwriteIQ into an existing workflow, UnderwriteIQ can equip an underwriting team with the tools and insights necessary to navigate the evolving risk landscape and pave the way for a future defined by informed choices and sustainable growth.

To learn more about UnderwriteIQ and how a unified platform solves many of the practical challenges of building workflows across multiple risk disciplines, click here.

Alisha is the Director of Product Management - Applications, responsible for Moody's RMS modeling application, Risk Modeler.

Alisha brings to Moody's RMS more than 10 years of experience managing software application product pipelines across private and public sectors. She oversaw operations for robotic engineering projects at NASA and was instrumental in designing Kaiser Permanente’s IT Clinical Call Center application. She holds a master’s degree in Information Systems and a bachelor’s degree in Economics from Santa Clara University.