UnderwriteIQ: Improve Underwriting Profitability and Achieve Greater Business Alignment

Justin BarrowMarch 01, 2023

Within their role as the economic engine for insurers, underwriters face an increasingly challenging market to navigate through. With escalating natural catastrophe losses, rising inflation, and increasing customer expectations to contend with, this has all placed additional pressure on the underwriting organization.

There is a need for underwriters to improve their risk selection and technical pricing, and to modernize their systems to support new digital workflows and advanced analytics capabilities. But despite increased investment in data and technology, more than 50 percent of insurance firms have failed to achieve a return on equity above the cost of capital in the past five years.

Promises from vendors of reaching higher premium business and greater profitability by investing in new underwriting systems often fall short of expectations, resulting in insurers having more systems to manage, new views of risk to maintain, and greater volatility in risk decisions.

We think there is a better way to get underwriting analytics. We have been building UnderwriteIQ to help address these gaps.

Introducing UnderwriteIQ

April 2023 will see the introduction of the Moody’s RMS UnderwriteIQ™ application, which takes advantage of Moody’s RMS industry-leading models, data products, and technology to deliver trusted, agile underwriting analytics to modernize underwriting systems for this new world of risk.

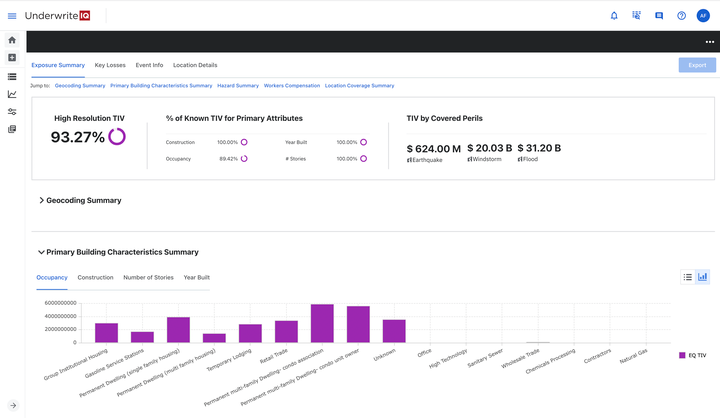

Moody's RMS UnderwriteIQ application screenshot

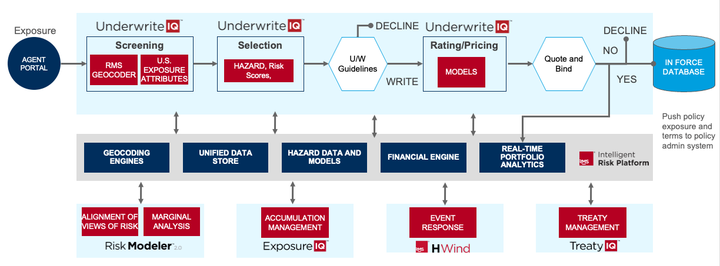

Leveraging the power, speed, and scale of the cloud-native Moody’s RMS Intelligent Risk Platform™ (IRP), UnderwriteIQ works fast and can seamlessly embed insights into new and existing workflows.

The fourth insurance application launched on the IRP since 2020, UnderwriteIQ is not just a powerful underwriting application, it is part of an ecosystem of collaborative applications that share the same science, exposure data, geocoding, and financial engines tailored to the unique needs of the users.

More than 105 property and casualty (P&C) insurance customers already taking advantage of Moody’s RMS Software-as-a-Service (SaaS) applications and services on the IRP.

Improve Risk Selection and Pricing in Challenging Market Conditions

The ability to confidently price and select risk is more important today than ever before. The reinsurance market experienced a significant hardening from the recent 2023 renewals. Many reinsurance firms are prioritizing profitability over revenue growth by reducing the size of their book of business and improving technical pricing.

The downstream impact of this prioritization on primary insurers could be significant now and in the future. Insurers could expect higher prices to cede risk, requiring them to reevaluate how much risk they should be taking on themselves.

While no firm will be immune to these market conditions, firms that have the greatest confidence in their technical pricing and underwriting processes will have a distinct competitive advantage.

To help firms improve risk selection and technical pricing, UnderwriteIQ utilizes the same industry-leading science, data, and modeling used in Moody's RMS Risk Modeler™ application.

UnderwriteIQ offers insights for specific perils that span across the global coverage provided by Moody’s RMS modeling portfolio, including new high-definition models for high gradient perils, such as flood and wildfire.

All Moody’s RMS models are rigorously tested and validated, are built with the best available hazard data, and utilize advanced financial modeling frameworks designed to capture a variety of unique terms and conditions at the coverage level.

In addition, for companies operating in different areas of the world, or those that want to expand into other parts, Moody's RMS offers hazard data across regions to help you evaluate risks broadly, save time, and gain efficiency, whether you need to evaluate wildfire risk in California, flood risk in the United Kingdom, or earthquake risk in New Zealand.

For over 30 years, Moody’s RMS models and risk analytics have been a cornerstone of the (re)insurance industry with Moody’s RMS partnering with eight of the top ten global insurance brokers, nine of the top 12 commercial insurers, and 17 of the top 20 reinsurers. Our modeling insights are trusted throughout the industry and UnderwriteIQ continues this tradition.

Increasing Underwriting Throughput

Underwriting that can leverage cloud-native technologies to automate key processes for risk screening and pricing workflows helps to maximize the effectiveness of underwriting across the business.

The most valuable underwriting systems are those that can serve as a traffic light to underwriters: make better, faster, and more profitable streamlined decisions to quote good risks (green), decline bad risks that clearly fall outside of underwriting guidelines (red), and refer risks that require additional analysis to underwriters (yellow).

For example, a submission may be in a geographic region where guidelines dictate further scrutiny; this account may potentially be profitable, but this would be difficult to ascertain without advanced analytics.

UnderwriteIQ is built on a fast, powerful, and highly scalable cloud-native architecture that ensures 24/7 availability and superior performance. I repeat, UnderwriteIQ is fast. It shares the same cloud-native infrastructure as Risk Modeler, which models risk up to 36x faster than equivalent on-premises infrastructure with Moody's RMS RiskLink®.

Using industry-standard REST APIs allows UnderwriteIQ to easily onboard risks, screen the risk with high-quality exposure data, apply underwriting guidelines, and price the risk with the Moody's RMS modeling portfolio.

Risks that clearly fall within or outside of the underwriting guidelines can bypass the underwriting workbench and go straight to binding and quoting the risk. For customers that can streamline the approval process, insurers can respond faster and more efficiently to their customers and provide superior service.

For submissions that require a more detailed review, UnderwriteIQ seamlessly incorporates into the underwriting workbench. Within your workbench, you will have access to powerful underwriting analytics such as global geocoding and hazard scoring, exposure analysis, average annual loss (AAL), and Exceedance Probability (EP) curves offering event and location level detail.

Enhance Decision-Making Between Risk Disciplines

Most underwriting applications run on different infrastructures for catastrophe modeling or portfolio management systems, and with potentially different exposure data, modeling approaches, and financial engines.

These siloed systems make collaboration between underwriting and portfolio management more difficult. Catastrophe modelers, who are supporting both underwriters and portfolio managers, are tasked with migrating post-bind policies into their portfolios as well as reconciling the underwriter’s view of risk with their own.

This saps productivity across risk management teams, diverting them from high-value work that helps them grow the business.

UnderwriteIQ shares the same platform services as both the Risk Modeler™ and ExposureIQ™ Moody’s RMS catastrophe modeling and exposure management applications, including geocoding services, financial engines, global hazard risk and exposure analytics, and portfolio data.

This integration between the different applications dramatically simplifies decisions to diversify portfolios, set capital requirements, and cede risks because all disciplines are working off a unified view of risk built on real-time portfolio data.

By sharing the same exposure data and modeling engines, portfolio managers and catastrophe modelers have confidence in the consistency of how risk is analyzed across the organization.

You can see the variation in loss results through the use of different geocoding engines in our blog focused on geocoding consistency with differences evident even when the model shares the same hazard analytics and financial engine.

With the release of UnderwriteIQ just around the corner, now is the time to better understand how you can modernize your underwriting system for the new world of risk. For firms already licensing Risk Modeler or ExposureIQ, deploying UnderwriteIQ will not require any new infrastructure, no complex data migration of exposure data, or complex installations.

To learn more about UnderwriteIQ and the Intelligent Risk Platform you can find out more here.

Justin is a Staff Application Product Manager for Moody’s RMS, responsible for the development of Moody’s RMS UnderwriteIQ application on the Intelligent Risk Platform. Prior to joining RMS, Justin was a product manager at two reinsurance brokers for a total of sixteen years, leading initiatives primarily regarding catastrophe modeling and actuarial, with the occasional sojourn into ancillary projects.

Earlier in his insurance career, Justin held roles in large account underwriting, actuarial, catastrophe modeling, captives, technology management, and underwriting operations. In between working in the reinsurance and primary sides of insurance, he was an RMSer – many years ago – with a product role on the RMS RiskBrowser team.

Justin holds a bachelor’s degree in Economic Theory and Quantitative Methods from the American University.