New Era of U.S. Wildfire Modeling Begins with Risk Modeler

Michael YoungOctober 14, 2019

The last two North America wildfire seasons have seen total insured losses skyrocket to over US$23 billion – compared to 1991-2010 where average annual losses totaled US$600 million. Wildfire has staked its claim as a major U.S. peril, with events now consistently topping the multi-billion dollar mark. Four of the five all-time biggest wildfire events occurred in 2017 and 2018, and seven wildfires exceeded the US$1 billion threshold in this timeframe.

When the WUI is Not Enough

Wildfire risk can no longer be managed through accumulation strategies, hazard zoning, or simple extrapolation of historical data because the fundamental drivers of wildfire risk are changing:

There are 30 percent more buildings at risk than there were 30 years ago

Recent weather patterns show that the fire season is getting hotter and drier than in the past

All these factors mean that past losses cannot be easily extrapolated to predict future risk levels. Instead, the industry needs tools from a probabilistic catastrophe model to properly capture future wildfire risk.

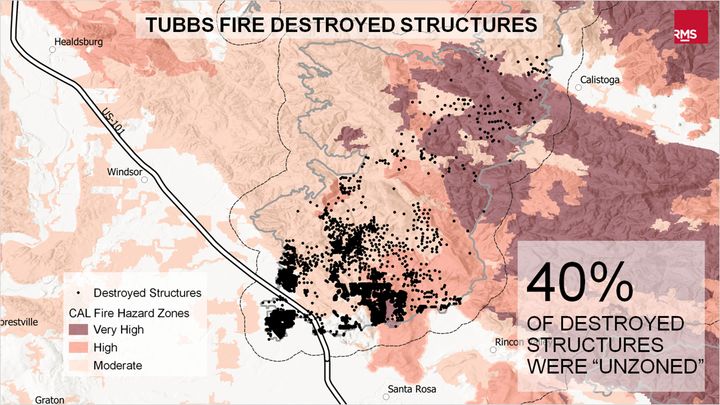

Wildfire risk is not limited to the Wildland Urban Interface (WUI) anymore. The figure below shows DINS (Damage Inspection) data from CAL FIRE overlaid on the burn perimeter for the 2017 Tubbs Fire in Northern California. Almost half of the destroyed structures in that fire came from areas considered to have no wildfire risk since they are in sub-urban areas classified as non-burnable by existing risk scoring methods. It is not sufficient to manage insurance portfolios with simple hazard zoning approaches.

Figure One: DINS (Damage Inspection) data from CAL FIRE overlaid on the burn perimeter for the 2017 Tubbs Fire in Northern California

High Definition Models Required for Forward-Looking View of Risk

The latest version 1.13 release of RMS® Risk Modeler now includes the RMS U.S. Wildfire High Definition (HD) Model version 1.0 to provide a robust fully probabilistic model of current fire wildfire risk supported by high-fidelity data sets. The HD modeling framework incorporates over 15 million individual wildfire footprints spread across the entire continental United States designed to capture spatial and seasonal correlations of wildfire risk today.

The model includes a forward-looking view of ignition probability, a fully dynamic fire spread module driven by extreme fire weather simulations, explicit simulations of ember transport and the likelihood of urban conflagration. All these elements are important in producing a forward-looking view of wildfire risk.

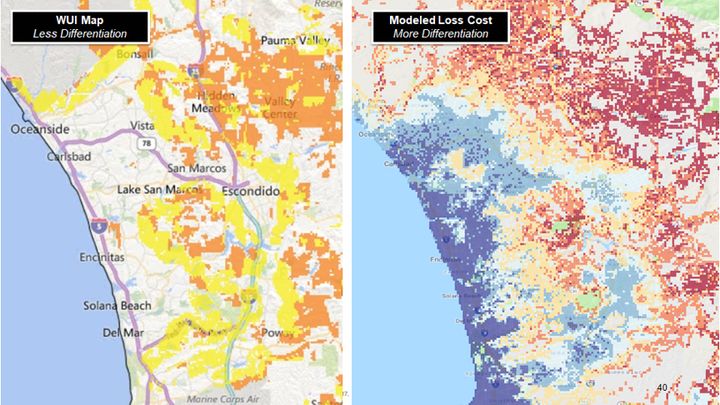

All of these features are captured in a high definition (HD) probabilistic framework to reflect its spatial nuances, and takes into account real-life, on-the-ground conditions. The figure below shows how the model provided a continuous varying loss cost ($ / $1000 of coverage) compared to the in/out classification based on WUI zones. The WUI leaves large areas of high density exposure out of its assessment, potential underestimating the potential solvency-level catastrophes that may affect the insurance portfolio.

Figure Two: Comparison of WUI maps (left) to model loss cost (right)

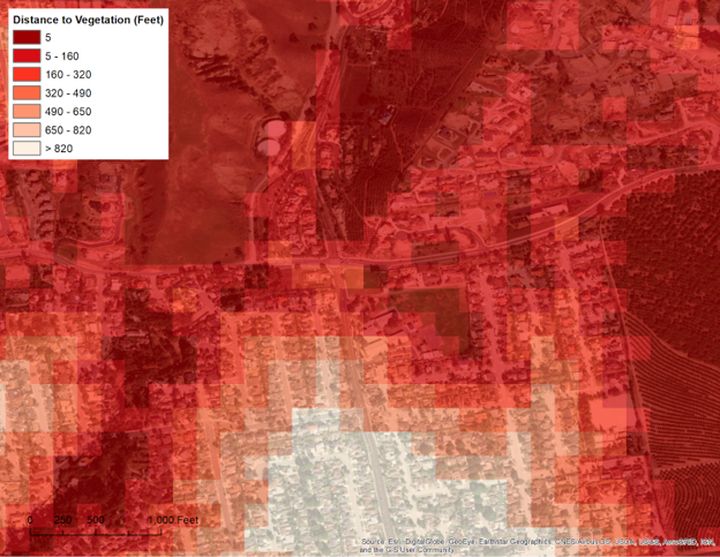

Wildfire is the latest model to benefit from the extensibility of the Risk Data Object (RDO) open data standard, which will be released to the industry in early 2020. To support the new model, the RDO was extended to include additional secondary modifiers and site hazard information specific to wildfire risks, such as fuel, slope, and distance to vegetation to help users better reflect the specific hazard affecting their loss potential.

One of the key variables in wildfire risk assessment is the distance to local vegetation and available fuel located around a subject property. Risk Modeler can estimate the distance to vegetation automatically for subject properties using proprietary databases compiled at a resolution of 50 meters. Risk Modeler also lets users test the sensitivity of this attribute as well as others. Users can refine the loss estimate by collecting and using their own values for these attributes, but if they are left unknown, the model calculates them using a 50-meter uniform resolution grid supplied by RMS.

The Notebook and/or Analytics Gateway can be leveraged to drill down further into the impact at the line of business, region, or even location level. This type of model investigation can help steer business and resourcing decisions on the collection and use of more detailed information in account and portfolio modeling. For example, companies that have invested in private fire-fighting services can use the Active Suppression modifier in the model to reduce their portfolio risk levels and risk-transfer expenses.

What Else is New in Risk Modeler 1.13

HD Models in Structure Analysis – Within Risk Modeler, users can conduct structure analyses, which groups analyses and model reinsurance structures (with hours clause) so that users can analyze the marginal impact of adding a new portfolio or model to a personalized view of risk. Within the new Risk Modeler 1.13, this structure “rollup” capability is supported for both the RMS U.S. Wildfire HD and RMS U.S. Inland Flood HD models and all existing RiskLink models.

Vice President, Model Product Management, Moody's RMS

Michael leads a team that establishes requirements and features for all of the Moody's RMS North and South America climate models. Michael's responsibilities include overseeing the submission of Moody's RMS products to regulatory reviewers, such as the Florida Commission on Hurricane Loss Projection Methodology (FCHLMP).

Michael has led studies of insurance mitigation programs for the state of Florida, as well as the World Bank. In his past 14 years at Moody's RMS, Michael has also worked as a lead wind vulnerability engineer, a director of claims and exposure development, and as the head of the mitigation practice. He has worked in commercial wind-tunnel laboratories doing studies on wind loads for a variety of buildings.

Before joining Moody's RMS, he was involved in the development of Federal Emergency Management Agency (FEMA) HAZUS-MH software for hurricane risk assessment, and he taught courses on the use of HAZUS hurricane and flood components. Michael has also led studies on mitigation cost effectiveness for building codes such as the 2001 Florida Building Code and the North Carolina Building Code.

Michael holds a bachelor's degree in Civil Engineering and a master's degree from the University of Western Ontario in Canada in Wind Engineering.