The 2013-14 European winter storm season has been pretty active so far. Early in the season, Windstorm Christian raced across northern Europe, followed by Xaver in early December, and then storms Dirk, Erich, Felix and Anne hit the U.K., Ireland, and northwest France over the Christmas and New Year period.

To date the season has been a great demonstration of how northern Europe is a common target for winter storms. However, this week sees the 5th anniversary of Windstorm Klaus, reminding us that storms can also impact southern Europe, affecting regions not acclimatized to extreme winds and causing severe damage.

What happened when Klaus hit and what have we learned from it?

Can such a storm occur again in the near future and more importantly, can we predict it, or at least estimate how bad it could be?

Windstorm Klaus sprung to life on January 23, 2009 in the central Atlantic, directly in line with southern France. The climate backdrop to this storm was pretty uncharacteristic. The large-scale Icelandic low-pressure system and the Azores high-pressure system were farther south than usual. Also, the North Atlantic Oscillation (NAO) was entering a negative phase.

A positive phase of the NAO creates favorable conditions for strong storms to pass over northern Europe, as Lothar and Anatol did in 1999. But a neutral or negative phase of the NAO can lead to storms that affect southern Europe and this is exactly what happened with Windstorm Klaus.

By midnight on January 24, as Klaus approached land, it had a central pressure of 963 hPa, comparable to Windstorm Lothar. Winds reached severe gale force in the southwest of France, peaking with gusts above 140 km/h at coastal locations near Bordeaux, accompanied by violent seas with wave heights of several meters. Local infrastructure was severely disrupted by fallen trees and electricity pylons.

Over 1.7 million households were without power immediately after the storm and over 60% of maritime pines in the Forêt des Landes were destroyed. Once the damage had been appraised, Klaus was estimated to have caused insured losses of €2.5billion (US$3.4 billion).

Shortly after the event, RMS scientists Dr. Navin Peiris and Dr. Christos Mitas conducted a reconnaissance survey, which helped to enhance our understanding of building vulnerability in this region. They observed frequent non-structural wind damage, such as the uplifting of roof tiles and collapsed chimneys, but also direct wind damages from tree fall, due to the high density of trees in close proximity to properties.

Source: RMS 2009 reconnaissance

Closer examination of the roof damage revealed little evidence of proper fixation, particularly along roof edges, leaving them more vulnerable to wind damage. Another observation was the use of canal-type tiles, which are prone to uplift from the build up of air pressure, caused by strong winds. Also, damage was more frequent in residential properties, compared to commercial or industrial buildings that are generally engineered in line with building codes.

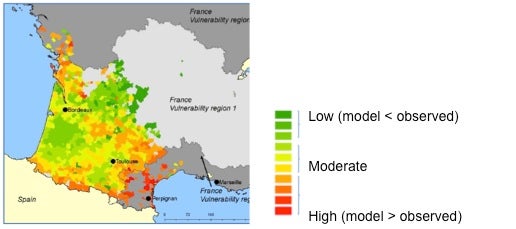

This survey, combined with an assessment of claims data, provided us with an enhanced understanding of regional vulnerability differences. For example, we observed a significantly lower fragility of buildings in the Perpignan area compared to the southwest of France.

Ratio of the modeled and observed losses by postcode using non-regionalized vulnerability functions. Variation supports need for distinct vulnerability regions.

This information is vital for us to continually develop and inform our models, in order to represent the risk accurately. Due to the inherent uncertainty in the climatic phenomena driving windstorms, it is not possible to forecast exactly when the next strong storm will hit southern Europe. Catastrophe models provide a range of possible events, which can help the insurance industry prepare for the next big event.

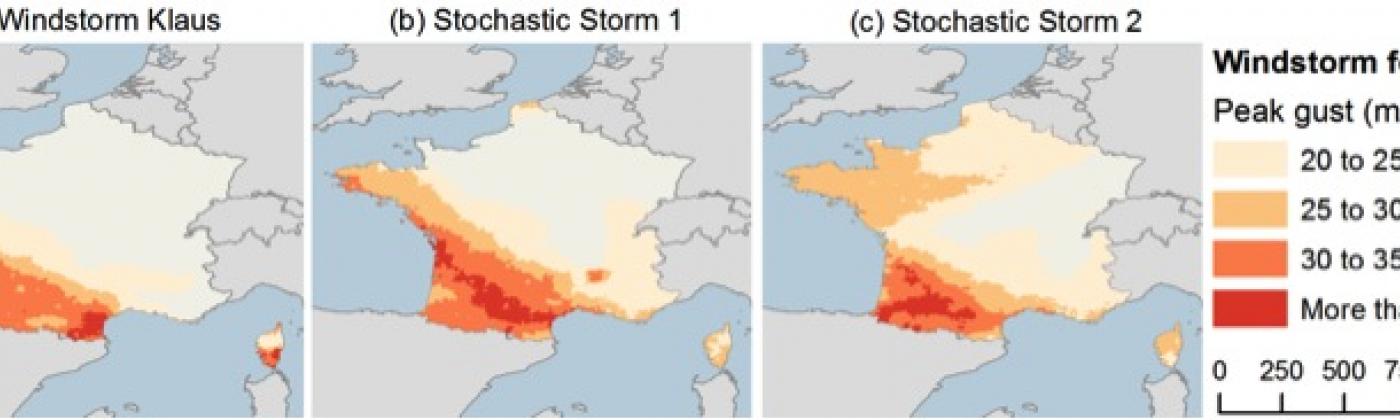

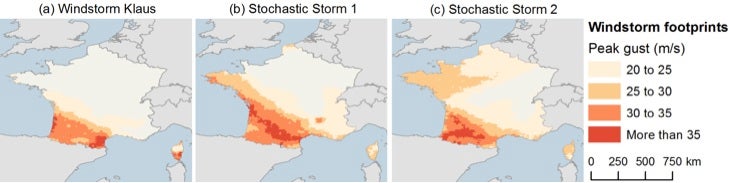

The RMS Europe Windstorm Model contains storms comparable to Klaus, including some that impart larger wind intensities and damages. The below image compares two examples of stochastic storms with the actual Klaus wind footprint to illustrate storms that could potentially cause insured losses similar to or higher than Klaus.

Currently we are in a close to neutral phase of the NAO, so does that mean a Klaus type storm could occur this winter? No one can answer that question for certain, but a model at least enables us to explore the possible worst-case scenarios and be prepared.

Share:

You May Also Like

November 06, 2020

Examining the European Windstorm Outlook This Winter

Senior Director, Market and Product Specialists, RMS

Laurent is a catastrophe risk management expert at RMS, advising some of the largest companies in the (re)insurance industry how to best manage their nat cat, agriculture, cyber and terrorism risks. He also interacts as an expert for governmental and regulatory authorities. Laurent initially joined RMS in 2008 as part of the account management team, servicing the European (re)insurance and ILS market. He then headed the model product management group for all EMEA and APAC climatic/weather risk perils, such as windstorm, typhoon, severe convective storm and flood, as well as RMS global agricultural risk.

Prior to RMS, Laurent worked 3 years at the Swiss Federal Institute of Technology Zurich (ETHZ) as a Research Associate and Lecturer, managing multidisciplinary research projects. Laurent still lectures regularly on catastrophe modeling and insurance risk quantification at universities and gives seminars and invited talks in international industry conferences. Laurent co-authored numerous industry publications, peer-reviewed scientific articles and proceeding papers. He holds an MSc in Geology from the University of Lausanne and a PhD in Geophysics from the University of Lausanne and the University of Nantes.