Recent research by RMS® in collaboration with the CIPR and IBHS is helping move the dial on wildfire risk assessment, providing a benefit-cost analysis of science-based mitigation strategies

The significant increase in the impact of wildfire activity in North America in the last four years has sparked an evolving insurance problem. Across California, for example, 235,250 homeowners’ insurance policies faced non-renewal in 2019, an increase of 31 percent over the previous year. In addition, areas of moderate to very-high risk saw a 61 percent increase – narrow that to the top 10 counties and the non-renewal rate exceeded 200 percent.

A consequence of this insurance availability and affordability emergency is that many residents have sought refuge in the California FAIR (Fair Access to Insurance Requirements) Plan, a statewide insurance pool that provides wildfire cover for dwellings and commercial properties. In recent years, the surge in wildfire events has driven a huge rise in people purchasing cover via the plan, with numbers more than doubling in highly exposed areas.

In November 2020, in an effort to temporarily help the private insurance market and alleviate pressure on the FAIR Plan, California Insurance Commissioner Ricardo Lara took the extraordinary step of introducing a mandatory one-year moratorium on insurance companies non-renewing or canceling residential property insurance policies. The move was designed to help the 18 percent of California’s residential insurance market affected by the record 2020 wildfire season.

The Challenge of Finding an Exit

“The FAIR Plan was only ever designed as a temporary landing spot for those struggling to find fire-related insurance cover, with homeowners ultimately expected to shift back into the private market after a period of time,” explains Jeff Czajkowski, director of the Center for Insurance Policy and Research (CIPR) at the National Association of Insurance Commissioners. “The challenge that they have now, however, is that the lack of affordable cover means for many of those who enter the plan there is potentially no real exit strategy.”

The FAIR Plan was only ever designed as a temporary landing spot for those struggling to find fire-related insurance cover, with homeowners ultimately expected to shift back into the private market after a period of time. The challenge that they have now, however, is that the lack of affordable cover means for many of those who enter the plan there is potentially no real exit strategy.

Jeff Czajkowski, director of the Center for Insurance Policy and Research (CIPR) at the National Association of Insurance Commissioners

These concerns are echoed by Matt Nielsen, senior director of global governmental and regulatory affairs at RMS. “Eventually you run into similar problems to those experienced in Florida when they sought to address the issue of hurricane cover. You simply end up with so many policies within the plan that you have to reassess the risk transfer mechanism itself and look at who is actually paying for it.”

The most expedient way to develop an exit strategy is to reduce wildfire exposure levels, which in turn will stimulate activity in the private insurance market and lead to the improved availability and affordability of cover in exposed regions. Yet therein lies the challenge. There is a fundamental stumbling block to this endeavor unique to California’s insurance market and enshrined in regulation.

California Code of Regulations, Article 4 – Determination of Reasonable Rates, §2644.5 – Catastrophe Adjustment: “In those insurance lines and coverages where catastrophes occur, the catastrophic losses of any one accident year in the recorded period are replaced by a loading based on a multi-year, long-term average of catastrophe claims. The number of years over which the average shall be calculated shall be at least 20 years for homeowners’ multiple peril fire. …”

In effect, this regulation prevents the use of predictive modeling, the mainstay of exposure assessment and accurate insurance pricing, and limits the scope of applicable data to the last 20 years. That might be acceptable if wildfire constituted a relatively stable exposure and if all aspects of the risk could be effectively captured in a period of two decades – but as the last few years have demonstrated, that is clearly not the case.

As Roy Wright, president and CEO of the Insurance Institute for Business & Home Safety (IBHS), states: “Simply looking back might be interesting, but is it relevant? I don’t mean that the data gathered over the last 20 years is irrelevant, but on its own it is insufficient to understand and get ahead of wildfire risk, particularly when you apply the last four years to the 20-year retrospective, which have significantly skewed the market. That is when catastrophe models provide the analytical means to rationalize such deviations and to anticipate how this threat might evolve.”

Simply looking back might be interesting, but is it relevant? I don’t mean that the data gathered over the last 20 years is irrelevant, but on its own it is insufficient to understand and get ahead of wildfire risk, particularly when you apply the last four years to the 20-year retrospective, which have significantly skewed the market.

Roy Wright, president and CEO, Insurance Institute for Business & Home Safety (IBHS)

The insurance industry has long viewed wildfire as an attritional risk, but such a perspective is no longer valid, believes Michael Young, senior director of product management at RMS. “It is only in the last five years that we are starting to see wildfire damaging thousands of buildings in a single event,” he says. “We are reaching the level where the technology associated with cat modeling has become critical because without that analysis you can’t predict future trends. The significant increase in related losses means that it has the potential to be a solvency-impacting peril as well as a rate-impacting one.”

Addressing the Insurance Equation

“Wildfire by its nature is a hyper-localized peril, which makes accurate assessment very data dependent,” Young continues. “Yet historically, insurers have relied upon wildfire risk scores to guide renewal decisions or to write new business in the wildland-urban interface (WUI). Such approaches often rely on zip-code-level data, which does not factor in environmental, community or structure-level mitigation measures. That lack of ground-level data to inform underwriting decisions means, often, non-renewal is the only feasible approach in highly exposed areas for insurers.”

California is unique as it is the only U.S. state to stipulate that predictive modeling cannot be applied to insurance rate adjustments. However, this limitation is currently coming under significant scrutiny from all angles. In recent months, the California Department of Insurance has convened two separate investigatory hearings to address areas including:

Insurance availability and affordability

Need for consistent home-hardening standards and insurance incentives for mitigation

Lack of transparency from insurers on wildfire risk scores and rate justification

In support of efforts to demonstrate the need for a more data-driven, model-based approach to stimulating a healthy private insurance market, the CIPR, in conjunction with IBHS and RMS, has worked to facilitate greater collaboration between regulators, the scientific community and risk modelers in an effort to raise awareness of the value that catastrophe models can bring.

“The Department of Insurance and all other stakeholders recognize that until we can create a well-functioning insurance market for wildfire risk, there will be no winners,” says Czajkowski. “That is why we are working as a conduit to bring all parties to the table to facilitate productive dialogue. A key part of this process is raising awareness on the part of the regulator both around the methodology and depth of science and data that underpins the cat model outputs.”

“The aim of the report is to demonstrate the ability of cat models to reflect structure-specific and community-level mitigation measures,” Czajkowski continues, “based on the mitigation recommendations of IBHS and the National Fire Protection Association’s Firewise USA recognition program. It details the model outputs showing the benefits of these mitigation activities for multiple locations across California, Oregon and Colorado. Based on that data, we also produced a basic benefit-cost analysis of these measures to illustrate the potential economic viability of home-hardening measures.”

Applying the Hard Science

The study aims to demonstrate that learnings from building science research can be reflected in a catastrophe model framework and proactively inform decision-making around the reduction of wildfire risk for residential homeowners in wildfire zones.

As Wright explains, the hard science that IBHS has developed around wildfire is critical to any model-based mitigation drive. “For any model to be successful, it needs to be based on the physical science. In the case of wildfire, for example, our research has shown that flame-driven ignitions account for approximately only a small portion of losses, while the vast majority are ember-driven.

“Our facilities at IBHS enable us to conduct full-scale testing using single- and multi-story buildings, assessing components that influence exposure such as roofing materials, vents, decks and fences, so we can generate hard data on the various impacts of flame, ember, smoke and radiant heat. We can provide the physical science that is needed to analyze secondary and tertiary modifiers—factors that drive so much of the output generated by the models.”

Our facilities at IBHS enable us to conduct full-scale testing using single- and multi-story buildings, assessing components that influence exposure such as roofing materials, vents, decks and fences, so we can generate hard data on the various impacts of flame, ember, smoke and radiant heat.

Roy Wright, president and CEO, Insurance Institute for Business & Home Safety (IBHS)

To quantify the benefits of various mitigation features, the report used the RMS® U.S. Wildfire HD Model to quantify hypothetical loss reduction benefits in nine communities across California, Colorado and Oregon. The simulated reductions in losses were compared to the costs associated with the mitigation measures, while a benefit-cost methodology was applied to assess the economic effectiveness of the two overall mitigation strategies modeled: structural mitigation and vegetation management.

The multitude of factors that influence the survivability of a structure exposed to wildfire, including the site hazard parameters and structural characteristics of the property, were assessed in the model for 1,161 locations across the communities, three in each state. Each structure was assigned a set of primary characteristics based on a series of assumptions.

For each property, RMS performed five separate mitigation case runs of the model, adjusting the vulnerability curves based on specific site hazard and secondary modifier model selections. This produced a neutral setting with all secondary modifiers set to zero—no penalty or credit applied—plus two structural mitigation scenarios and two vegetation management scenarios combined with the structural mitigation.

The Direct Value of Mitigation

Given the scale of the report, although relatively small in terms of the overall scope of wildfire losses, it is only possible to provide a snapshot of some of the key findings. The full report is available to download.

Focusing on the three communities in California—Upper Deerwood (high risk), Berry Creek (high risk) and Oroville (medium risk)—the neutral setting produced an average annual loss (AAL) per structure of $3,169, $637 and $35, respectively.

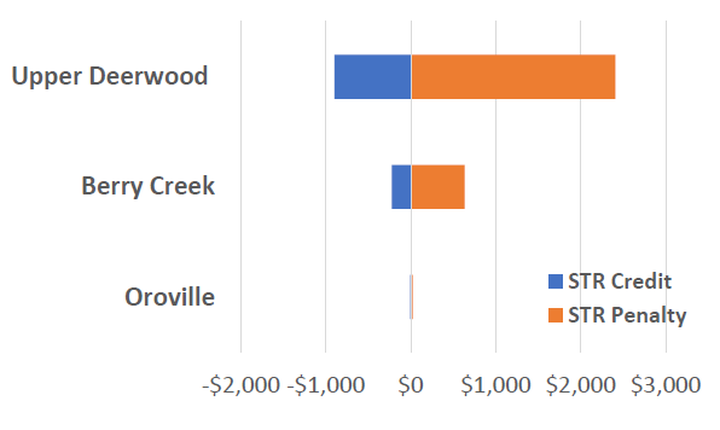

Figure 1: Financial impact of adjusting the secondary modifiers to produce both a structural (STR) credit and penalty

Figure 1 shows the impact of adjusting the secondary modifiers to produce a structural (STR) maximum credit (i.e., a well-built, wildfire-resistant structure) and a structural maximum penalty (i.e., a poorly built structure with limited resistance). In the case of Upper Deerwood, the applied credit saw an average reduction of $899 (i.e., wildfire-avoided losses) compared to the neutral setting, while conversely the penalty increased the AAL on average $2,409. For Berry Creek, the figures were a reduction of $222 and an increase of $633. And for Oroville, which had a relatively low neutral setting, the average reduction was $26.

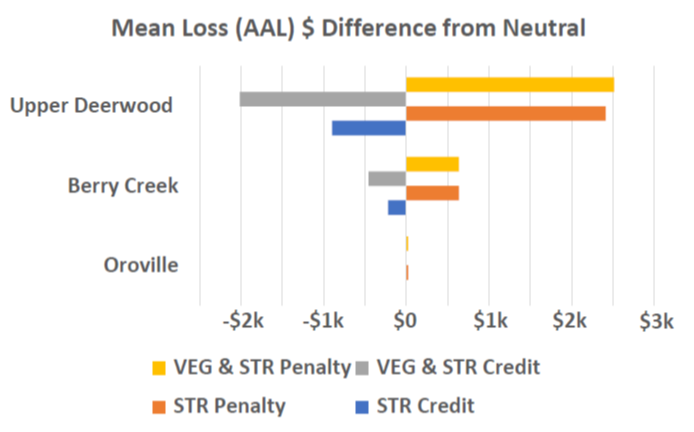

Figure 2: Financial analysis of the mean AAL difference for structural (STR) and vegetation (VEG) credit and penalty scenarios

In Figure 2 above, analyzing the mean AAL difference for structural and vegetation (VEG) credit and penalty scenarios revealed a reduction of $2,018 in Upper Deerwood and an increase of $2,511. The data, therefore, showed that moving from a poorly built to well-built structure on average reduced wildfire expected losses by $4,529. For Berry Creek, this shift resulted in an average savings of $1,092, while for Oroville there was no meaningful difference.

The authors then applied three cost scenarios based on a range of wildfire mitigation costs: low ($20,000 structural, $25,000 structural and vegetation); medium ($40,000 structural, $50,000 structural and vegetation); and high ($60,000 structural, $75,000 structural and vegetation).

Focusing again on the findings for California, the model outputs showed that in the low-cost scenario (and 1 percent discount rate) for 10-, 25- and 50-year time horizons, both structural only as well as structural and vegetation wildfire mitigation were economically efficient on average in the Upper Deerwood, California, community. For Berry Creek, California, economic efficiency for structural mitigation was achieved on average in the 50-year time horizon and in the 25- and 50-year time horizons for structural and vegetation mitigation.

Moving the Needle Forward

As Young recognizes, the scope of the report is insufficient to provide the depth of data necessary to drive a market shift, but it is valuable in the context of ongoing dialogue.

“This report is essentially a teaser to show that based on modeled data, the potential exists to reduce wildfire risk by adopting mitigation strategies in a way that is economically viable for all parties,” he says. “The key aspect about introducing mitigation appropriately in the context of insurance is to allow the right differential of rate. It is to give the right signals without allowing that differential to restrict the availability of insurance by pricing people out of the market.”

That ability to differentiate at the localized level will be critical to ending what he describes as the “peanut butter” approach—spreading the risk—and reducing the need to adopt a non-renewal strategy for highly exposed areas.

“You have to be able to operate at a much more granular level,” he explains, “both spatially and in terms of the attributes of the structure, given the hyperlocalized nature of the wildfire peril. Risk-based pricing at the individual location level will see a shift away from the peanut-butter approach and reduce the need for widespread non-renewals. You need to be able to factor in not only the physical attributes, but also the actions by the homeowner to reduce their risk.

Risk-based pricing at the individual location level will see a shift away from the peanut-butter approach and reduce the need for widespread non-renewals. You need to be able to factor in not only the physical attributes, but also the actions by the homeowner to reduce their risk.

Michael Young, senior director of product management at RMS

“It is imperative we create an environment in which mitigation measures are acknowledged, that the right incentives are applied and that credit is given for steps taken by the property owner and the community. But to reach that point, you must start with the modeled output. Without that analysis based on detailed, scientific data to guide the decision-making process, it will be incredibly difficult for the market to move forward.”

As Czajkowski concludes: “There is no doubt that more research is absolutely needed at a more granular level across a wider playing field to fully demonstrate the value of these risk mitigation measures. However, what this report does is provide a solid foundation upon which to stimulate further dialogue and provide the momentum for the continuation of the critical data-driven work that is required to help reduce exposure to wildfire.”

{kind=link}