Impact of Inconsistent Geocoding on Risk Transfer and Pricing

Owen Chamberlin

Evan CropperNovember 10, 2022

There is an expectation that an address within an insurance portfolio will represent a single distinct location, with only one possible set of coordinates. The deployment of different risk applications across the organization can result in an exposure’s location shifting, depending on the geocoding engine running in each risk application, from underwriting to catastrophe modeling or even exposure management.

How does a single address end up with different geocoordinates in different applications? The address could simply be wrong, either entered incorrectly or without all the relevant information, such as a property number, postal code, or even the correct country.

Some applications might only accept addresses in a specific format that is not common to some users. When errors occur, correcting them is typically a time-consuming manual process, first spotting the error and then correcting it – assuming the user even knows what is correct.

Geocoding engines try to help reconcile some of these address issues by guessing the coordinates for a “bad” address. However, depending on the application, different approaches can result in bad addresses translating into different coordinates. Rather than helping solve any issues, this could potentially make them worse.

Inaccurate locations are a huge problem, especially for an industry that does not like surprises or underwriting the wrong property – or if a policy experiences a total loss when it was supposed to be outside of a hazard area.

But insurers must deal with this uncertainty when different geocoding approaches are being applied to catastrophe modeling, underwriting, exposure management, or event response applications.

Accommodating geocoding uncertainty can impact risk transfer decisions across the entire life cycle. Inaccurate locations could mean taking a more cautious approach for fear of potentially underwriting the wrong location or a bad risk.

For portfolio and exposure management, small errors within individual properties build up to larger errors resulting in greater accumulations of unknown risk across portfolios. And when an event strikes, if properties are not accurately located, then event response could be misaligned.

How can consistent geocoding make an impact on reducing your risk? The RMS® Intelligent Risk Platform™ shares a common RMS geocoding engine that is purpose-built to work with the platform and operates seamlessly across all RMS applications such as ExposureIQ™ for exposure management.

Brief Summary of the Geocoding Process

The geocoding process begins when client portfolio address information is flowed into a user interface within one of the RMS applications. The geocoding engine logically segregates the address information (for example, postal code or city) into discrete fields, and standardizes address variations as required.

The geocoder then matches the location address information to the highest possible address resolution. If it is unable to match the address at the highest resolution, it intelligently reverts to the next lower resolution until an acceptable match is found.

This is a straightforward process when there is a full address, but as all insurers know, address data is rarely perfect and often contains data that is incomplete (missing fields), incorrect (typos, bad data), or poorly formatted. In this situation, most geocoders would not return a match or would need further information to be able to produce a location.

For insurers with a sizeable portfolio, providing this feedback is not possible when running portfolios of hundreds or thousands of locations

To account for this, the RMS geocoder is designed specifically for insurance locations and provides the correct information required for use in RMS applications.

Intentional features such as intelligent fallback, CRESTA zones, and exposure-weighted centroids allow the RMS geocoder to automatically select the exposure weight, regardless of the input data quality. As a result, the delivered location is best suited to provide the most accurate hazard and risk assessment based on the quality of the data provided.

Quantifying the Impact of Inconsistent Geocoding

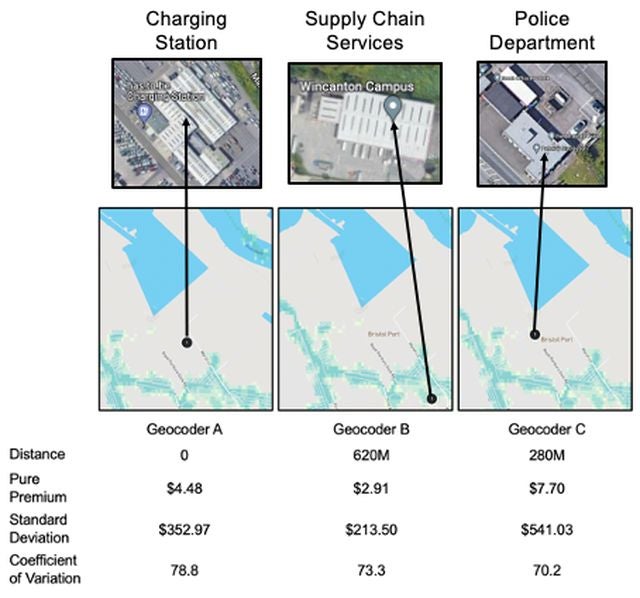

Let’s look at how inconsistent geocoding can impact a (re)insurer. Here’s an example address that would be challenging for a geocoding engine: PORTBURY DOCK, BRISTOL, BS20 9XL, U.K.

Although this address has many of the key inputs required for the geocoding engine to process, such as the postal code, city, and country, it is missing the street name and property number field. For a geocoding engine, this is very confusing. PORTBURY DOCK could refer to a location on the “Royal Portbury Dock Road,” the “Portbury Dock Harbor,” or even the “Portbury Docks Police Station.”

RMS ran an experiment using multiple geocoding engines, including in our own Risk Modeler™ application, to see how each would interpret the Portbury Dock addresses. After inputting the address into each geocoder, RMS collected the resulting latitude and longitude coordinates for each location.

We then ran each location in the Risk Modeler application with the RMS® U.K. Inland Flood High-Definition Model to see if there were meaningful differences between the risks of each geocoordinate.

Figure 1: Differing results of geocoders A, B, and C

Each geocoder returned a different set of coordinates for the same address, with up to 620 meters (nearly 0.5 mile) variation between geocoders A and C (Figure 1). The building characteristics for each location were quite different, and we saw three different hazard levels.

One location had a minimal flood risk, whereas two locations were in areas with an average annual loss (AAL) risk for a 1-in-200-year flood event. And there were three different views of risk, as the AAL for one location was more than two times that of another – and the standard deviation was even higher!

Evaluating Portfolio Risk

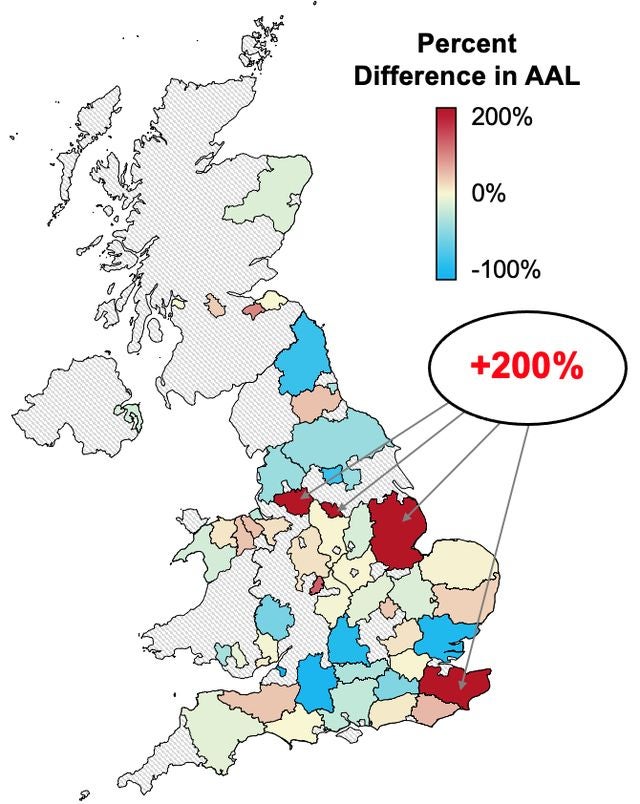

The first experiment was just for a single address, and many could assume that the differences in the geocoders would eventually normalize when running a larger portfolio. So, to better understand the impact of geocoding on a portfolio, we also conducted a similar experiment using the RMS geocoder and a non-RMS geocoder on a 150-location portfolio.

In the second experiment, we ran the 150 addresses into the non-RMS geocoding engine. Again, we collected the latitude and longitude coordinates of each location. We then ran two separate analyses using the RMS U.K. Inland Flood HD Model in the Risk Modeler application.

The first analysis was the portfolio with the original addresses without any geocoding enrichment. The second analysis was the coordinates of the non-RMS geocoder.

We found that the difference in AAL between the two portfolios was more than 25 percent. But, more importantly, 25 percent was not universal across all the properties. In fact, when looking at the AAL of individual properties or the cumulative AAL of the locations at the county level, less than half the counties were within +/-25 percent of each other and just over half of locations were within +/-25 percent of each other (55 percent).

Figure 2: Comparison of AAL at the county level of a 150-location U.K. flood portfolio for two different geocoding engines

Even more startling was the difference in AAL of some 15 properties across four counties: It was over 200 percent (Figure 2). When we dug into the portfolio, often only one or two locations were driving the largest discrepancies in the results. For example, the flood risk AAL for one location in Greater Manchester was US$12.40 with the Risk Modeler application geocoder, whereas it was US$51.26 for the non-RMS geocoder.

Prioritizing Consistent Geocoding

With a single geocoder across all your risk applications, users have confidence that each risk application will use the exact same location. This eliminates one of the key variables that can impact loss variance throughout the risk transfer workflow. In addition, the geocoder used in RMS Intelligent Risk Platform applications is built and maintained in-house by RMS for full control over change management.

This is important to ensure we can decide when and how the geocoder is updated to reduce the impact on our customers. Any updates or changes we make to the geocoder are documented in high detail and made available to customers to eliminate any surprises.

Compared to using multiple different geocoders, an industry-leading, flexible, and accessible geocoder allows you to reduce volatility across the risk transfer process. Whether underwriting an individual risk or ceding it across a portfolio of tens of thousands of locations, you can be confident that the address represents a single location across all your applications.

The RMS geocoder delivers a better total cost of ownership compared to separately licensed geocoders. In addition, it offers flexibility to include unlimited on-premises and cloud use and has insurance industry-specific features already built in, such as CRESTA zones, ACORD codes, variable resolution grid (VRG), and exposure-weighted centroids

Reducing Risk Volatility with a Consistent Geocoder

Insurers can reduce the volatility in how their risk applications are approaching addresses in a portfolio by using a consistent geocoder. The purpose-built RMS geocoding engine is:

Built with a common methodology: RMS applications leverage the same geocoding science for catastrophe modeling to underwriting, exposure management, or event response.

Purpose-built for insurers: Our geocoding engine is tailored to the unique needs of insurers and their exposure data.

Portable: Applications can swap engines based on models in production, allowing you to choose the same geocoding engine for your non-modeling applications, such as claims or processing.

All RMS applications – including Risk Modeler, ExposureIQ, TreatyIQ™, and RiskLink™– offer the purpose-built, industry-leading, flexible, accessible RMS geocoding engine, whether you are running your workloads in the cloud or in on-premises environments.

Combined with the ability to seamlessly embed the RMS geocoding engine into claims or processing applications, (re)insurers can have greater confidence in risk transfer decisions and servicing of customers.

Find out more about the RMS approach to improving risk operations, including consistent financial modeling, breaking down risk silos, and increasing automation of critical workflows.

Based in Phoenix, Arizona, Owen works as a Product Manager within the RMS Data Products Team to support RMS clients and applications with high-quality location information and geospatial data.

Owen holds a bachelor’s degree in Geography from the University of Colorado in Boulder and has over 10 years of experience in the mapping and geospatial industry.

Evan leads climate change and modeling product marketing for Moody's, where he helps customers develop more data-driven strategies using physical risk analytics. He has extensive experience scaling technology in the digital enterprise with a passion for using data to deliver better business outcomes.

Previously, Evan worked in various product management and marketing roles with Hitachi Vantara, Current - a subsidiary of GE Digital, and Cisco.

He holds a bachelor's degree in Political Science from Emory University and an MBA from Vanderbilt University’s Owen Graduate School of Business.