Five Ways RMS HD Modeling Helps You Manage European Windstorm Risk

Chloe Garrish

Giovanni LeonciniOctober 26, 2022

Windstorms remain the main driver of natural catastrophe insured loss in Europe, due in part to high levels of insurance penetration across the region. While individual claims might be small, the sheer size of these storms means multiple countries at a time are often impacted, resulting in significant cumulative costs to (re)insurers.

Regulatory focus is therefore high, with (re)insurers required to provide evidence that they hold adequate capital for these types of events.

The complex dynamics of extratropical cyclones make estimating losses a challenge. For example, these storms have the propensity to cluster, when a group of cyclones occur close in time. This complicates the application of per-event reinsurance coverage, such as hours clauses, and increases the volatility of aggregated loss figures. Along parts of Europe’s coast, the wind is not the only loss-causing peril as storm surge is also a major factor.

RMS® is expanding our portfolio of high-definition (HD) models to include the RMS Europe Windstorm HD Models, available in Spring 2023. Utilizing the latest science and data, the models have been fully rebuilt, and the storm surge domain has been extended across the entire U.K. coastline, Ireland, France, and Belgium.

This increased geographic coverage ensures customers can significantly reduce non-modeled risk, leading to better control of portfolio performance from earnings (short return periods) to capital (long return periods) risk metrics.

The HD-model framework delivers a more realistic representation of wind risk, empowering the (re)insurance industry to make informed decisions on portfolio and risk management. With more transparent and accurate calculations, organizations can gain a competitive advantage by better understanding windstorm risk.

The models provide an updated view of risk and include both recent claims data and the recent years of relatively low activity. Here are five clear ways RMS HD modeling helps you to manage European windstorm risk.

1. Modeling the Effect of Storm Clustering on Losses

Typically, catastrophe models incorporate either an event-based or a time-based stochastic set. Both capture the range of catastrophic event characteristics relevant to potential losses and their relative probability of occurrence. However, event-based stochastic sets assume that events are fully independent.

Yet, the year-on-year variability in climate patterns affects both the number of storms occurring within the same season and the proximity, increasing the volatility in losses and driving the tail of the aggregate exceedance probability distribution.

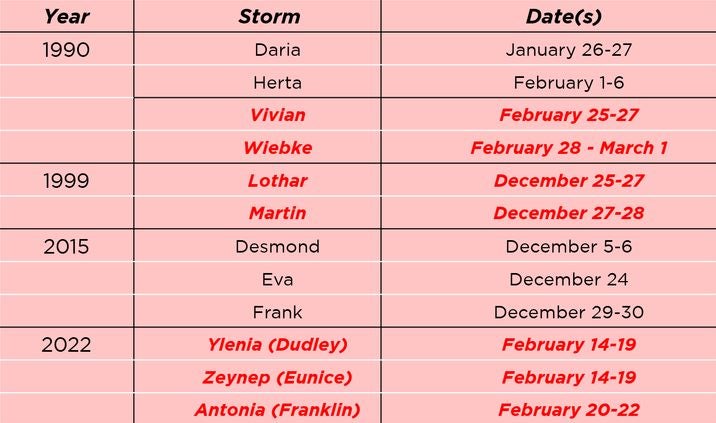

For example, this happened in 1990 (Daria, Herta, Vivian, and Wiebke), 1999 (Lothar and Martin), 2015 (Desmond, Eva, and Frank), and 2022 (Ylenia, Zeynep, and Antonia according to the Free University of Berlin, and Dudley, Eunice, and Franklin according to the U.K. Met Office). Event-based models, therefore, do not appropriately consider the impacts on losses of storm clustering.

The HD-model framework uses a full simulation engine allowing a detailed and explicit temporal evolution of each event within realistic multiannual periods, allowing for a better representation of seasonality and the native implementation of windstorm clustering. This leads to more realistic loss distributions helping you to better cost the risk, from pricing to accumulation and reinsurance.

2. Understanding the Potential Volume of Claims Before, During, and After an Event

Extratropical cyclones can impact areas exceeding 1,000 kilometers (621 miles) in scale, producing losses in multiple countries at a time. For example, almost two million insurance claims were made across nine countries following the February 2022 storm series of Ylenia, Zeynep, and Antonia (Dudley, Eunice, and Franklin).

The most damaging wind speeds are often found within only a few hundred kilometers of the storm center, meaning that due to the scale of these storms many claims can originate from areas that experienced lower wind speeds. There is a greater probability that buildings next to each other that are experiencing higher wind speeds will all be damaged, but this is not the case at lower wind speeds when only a subset of buildings will need to be repaired.

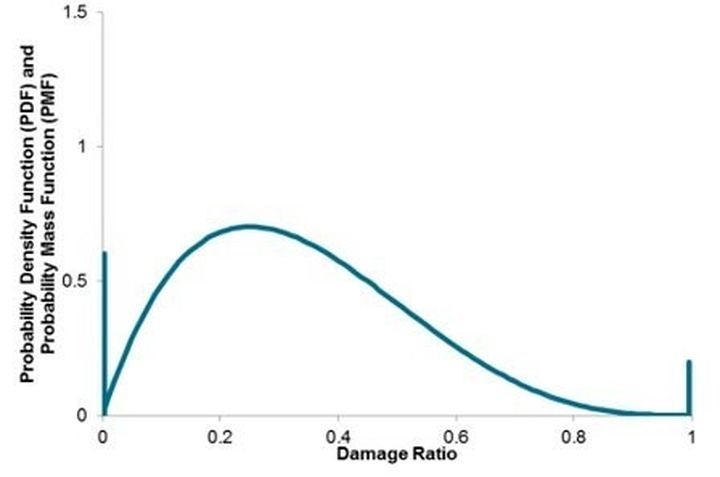

RMS HD Models™ have been built with a four-parameter vulnerability approach, which explicitly models the probability of zero damage or total damage for a given hazard intensity (see Figure 1).

Figure 1: Example of the four-parameter probability density function and probability mass function used to describe vulnerabilities

Coupled with a recalibrated vulnerability module for the Europe Windstorm HD Models, the innovative methodology delivers a more realistic view of claim frequency, that is fewer buildings are damaged and those that are, use a realistic damage ratio.

Having more realistic location- and coverage-level damage ratios also means generating more realistic gross loss distributions (after the application of limits and deductibles), which creates more confidence in modeling results.

Additionally, with HD modeling the potential volume of claims a portfolio could generate for a given storm is easier to understand, empowering you to know when and where to send claims adjusters for improved claims management.

3. Incorporating Time-Dependent Coverage Conditions into Your Pricing and Portfolio Management Decisions

European windstorm reinsurance coverage often contains an hours clause, which defines an insured loss occurrence as a period of time during an event. For windstorm, this is typically 72 hours. What makes this situation more complex is the tendency for storms to cluster, meaning losses within a 72-hour window could stem from more than one storm, increasing the likelihood that the hours clause coverage will cut off in the middle of an event.

For example, looking again at the multiple storm series experienced in 1990, 1999, 2015, and 2022, several storms occurred within 72 hours. This makes it challenging to aggregate losses into one (or more, in the case of reinstatements) loss occurrence (see Table 1).

Table 1: Storm series in 1990, 1999, 2015, 2022. Storms that occurred within 72 hours are highlighted in red.

Accurately applying the hours clause and the number of reinstatements can improve your understanding of which terms and conditions are most suitable and help reduce the amount of litigation following an event. Yet, many catastrophe models do not account for time-based conditions such as these.

With temporal simulation, RMS HD Models extend the catalog of reinsurance coverages you can model, including aggregated terms, multiyear contracts, bespoke hours clauses, and the number of reinstatements. The transparent and scientifically based approach to financial HD modeling helps you to improve your risk transfer processes.

4. Overcoming Gaps in Exposure Data in Storm-Surge Areas

For many regions, low-resolution or aggregate exposure data remains the norm. This implies that the location of the building is within a provided resolution or aggregation, for example, a postcode or CRESTA zone, but the exact location is unknown. For high-gradient perils, such as storm surge, this uncertainty can have a significant impact on losses.

HD models incorporate a new disaggregation methodology which ensures more realistic mapping between possible building geocoding and local hazard severity across different lines of business and resolutions. This methodology distributes exposure data from low resolution to high resolution using the latest geographic information system (GIS) and satellite technology.

Better modeling of local hazard severity leads to a more realistic claims distribution for aggregate data, and it ensures improved decision-making across all use cases from pricing to accumulation and reinsurance.

5. Unifying Your View of Climate Across Europe

The insurance penetration for windstorm is high across the continent, making wind one of the key drivers of catastrophe losses in Europe. Yet, in recent years, flood, hail, and convective storm losses have dominated the European market, driving (re)insurers to reevaluate their exposures to climate risks.

However, many catastrophe models do not have sufficient geographic coverage for all these perils, causing users to adapt to different methodologies across multiple vendor models, or in some cases, the risk remains unmodeled. The lack of cross-country and/or cross-vendor correlation can lead to highly uncertain modeling results, underestimation of risk volatility, and the possible underestimation of reinsurance protection and reinsurance pricing.

This situation is not unrealistic; it happened in 2021 when severe convective storms struck western and central Europe, closely followed by catastrophic flooding. This resulted in risk carriers being surprised by the need to buy extra protection in the middle of the year at very expensive rates.

To enable clients to unify their European climate analyses, RMS HD Models have been built on a consistent framework – utilizing the same exposure data, building inventory, simulation engine, vulnerability approach, and financial engine.

In addition, RMS HD Models give clients access to the most complete view of climate risk across Europe with geographic coverage of greater than 98 percent gross written premium (GWP) across 17 countries, the inclusion of all sub-perils, and a climate-conditioned view of risk.

Chloe is a senior product marketing manager at Moody's RMS, where she helps customers develop data-driven strategies to better understand their risk. She has more than a decade of experience in catastrophe modeling for the (re)insurance industry.

Previously, Chloe was a senior account director for CoreLogic, managing catastrophe modeling clients across Europe, Asia, and the U.S. Prior to CoreLogic, Chloe worked in various catastrophe modeling roles within a Lloyd’s Syndicate, AIG, and Aspen Re.

Chloe has a bachelor’s degree in Geography with Anthropology from Oxford Brookes University.

Giovanni has worked in the (re)insurance industry for the last 10 years with research and development roles for Property and Casualty at Zurich Insurance and Aspen Re. Previously he was a researcher at the Met Office and the University of Reading where he focused on convective scale ensembles.

He obtained his PhD in Meteorology from Colorado State University and a MSc from San Jose State University, and has earned his Laurea in Physics from the University of Bologna.