At this year’s RMS Terrorism Risk Summit, we focused attention on the U.S. landscape. The main issue these days in terrorism insurance discussions relates to the Terrorism Risk Insurance Protection and Reauthorization Act (TRIPRA), which will expire at the end of December 2020 if not reauthorized. This important legislation is also known by other acronyms including TRIA (Terrorism Risk Insurance Act) and TRIP (Terrorism Risk Insurance Program). In discussing the U.S. federal backstop for certified acts of terrorism, all these names are synonymous.

To help make sense of the speculation and various policy options, RMS was proud to host Scott Williamson, Vice President and Director of Financial Analytics at the Reinsurance Association of America (RAA). Mr. Williamson has developed legislative models to assist the RAA in its advocacy on issues such as TRIA.

At the RMS event, Mr. Williamson provided an overview of the current TRIA structure and explored some alternative modifications to the program that were considered to make a legislative recommendation. This included an evaluation of multiple ‘what-if’ scenarios, using a range of attack modes and targets, and various assumptions regarding the compounded average growth rate of the U.S. economy. For this study, RMS partnered with RAA to estimate economic losses due to a range of scenario terrorism events for property and workers’ compensation lines of businesses, using its latest Terrorism Model and Economic Exposure Data.

Understanding TRIA

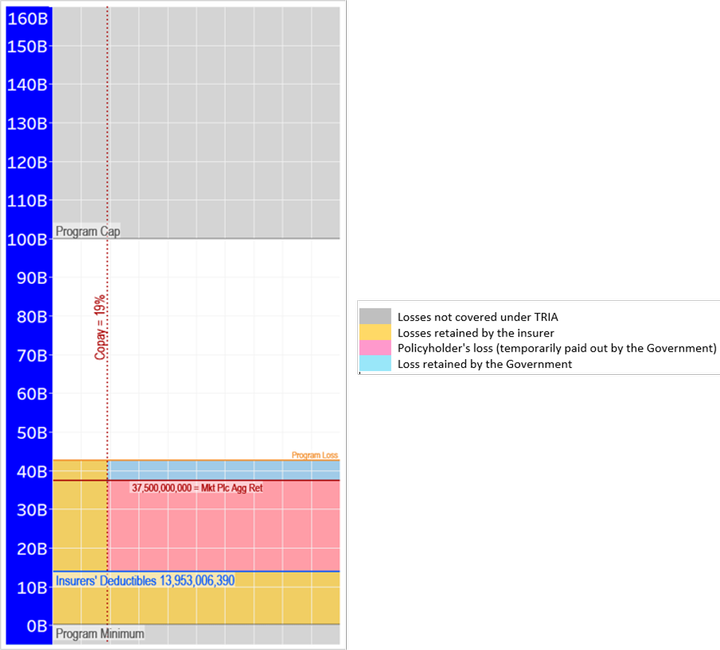

Per the TRIA legislation, each insurer has a deductible equivalent to 20 percent of its Direct Earned Premium of the previous year. Any loss above the deductible is co-shared between the insurer and the government (part of the government’s portion could be recouped under certain conditions). The percentage share varies by calendar year. The Insurance Marketplace Aggregate Retention Amount or IMARA is used as a threshold for the government to establish whether any government payments are liable for mandatory recoupment.

For losses below the IMARA, the government initially pays losses above the insurers’ aggregate deductibles (less the insurers’ copays). These government payments are later recouped from all TRIA covered lines policy holders at 140 percent. This process is called mandatory recoupment. For government loss payments that are above the IMARA, the government has the discretion to recoup all federal expenditures, but the assessment to policyholders in this layer are capped at a three percent policy surcharge per year. This process is called discretionary recoupment.

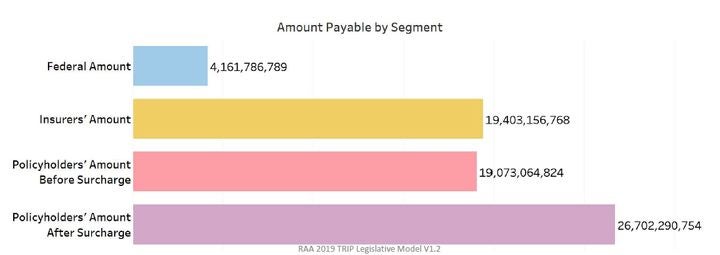

In his presentation, Mr. Williamson focused on cases causing mandatory recoupment. He explored a repeat of the 9/11/2001 terror attacks adjusted for inflation which equates to a total program loss of US$42 billion for calendar year 2019. In this scenario, the affected insurers retain about US$14 billion as deductible. Losses above the deductible are co-shared between the insurer (19 percent) and the government (81 percent).

However, the government recoups a major share of the amount it initially pays out, as part of the mandatory recoupment process (US$19 billion), i.e. 81 percent of the losses above the insurers’ deductible amount (US$14 billion) and below the IMARA (US$37.5 billion). Additionally, the government applies a surcharge that increases the recoupment amount to 140 percent of the government’s outlay below the IMARA, or about US$27 billon. Thus, the net amount retained by the government after consideration of the recoupment surcharge is actually less than zero. This scenario is illustrated below:

Figure 1: TRIA loss distribution diagram for a scenario terrorism event causing a US$42 billion insured loss

Though IMARA is US$37.5 billion in 2019, it is revised for 2020 (and beyond) as the average annual deductible from all insurers in the past three years. This average annual deductible will continue to increase in an economy with steady growth.

It was observed that even if the program structure remains unchanged, the market retains a significant amount of the risk – either in the form of the amount to be paid back to the government as part of recoupment process or the increasing deductible amount which is a function of the direct earned premium. Consequently, the share of losses retained by the government will decline, shifting more of the burden to insurers and policyholders.

Mr. Williamson concluded that RAA supports the as-is reauthorization of the TRIA program to avoid economic instability post a catastrophic terrorist event. In the absence of a stable private market, insuring economy and people against terrorism is a government responsibility which is co-shared by private market through the current partnership. Mr. Williamson did not imply that there was no room for improvements to TRIA, but that the reality is likely to be that any changes to the program will be difficult to pass during a Presidential election year.

RMS anticipates TRIA to continue in some form with possible changes to the current structure, in line with past reauthorizations. These changes could include updates to the loss trigger, shifts in the co-share percentages from government to insurers, changes in coverage to focus on more extreme Chemical, Biological, Radiological and Nuclear (CBRN) events and possible revision to the program limit. Without this support there would be significant gaps between terrorism insurance that is needed for a resilient economy versus what will be offered by the private market.

RMS strives to address the market’s quantification of terrorism risk. Our current model focuses on catastrophic or large-scale terrorism that could impact the solvency of an insurance firm and is well-suited for the type and magnitude of attack losses that might be covered by TRIA. In an ongoing effort to support some sort of reauthorization of TRIA, we welcome feedback on the federal program as well as RMS’ terrorism solution that can help to analyze its impact on insurance portfolios. Please reach out to RMS (support.rms.com) with any comments or questions.

Share:

You May Also Like

September 10, 2021

Twenty Years Since 9/11: Living With an Ever-Present Threat

Terrorism Risk for California Workers’ Compensation

The terrorism landscape has changed significantly since 9/11. There is a visible shift from large-scale attacks to a growing number of lone wolf attacks. Many believe there has not been a major terrorist event in the United States post 9/11, but one should not overlook the near-misses in the recent past which could have caused massive losses such as the 2016 New York-New Jersey bombings.

The unpredictable and catastrophic nature of terrorism led to the emergence and continued reauthorization of the U.S. Terrorism Risk Insurance Program or TRIPRA, a federal backstop for defined acts of terrorism, which facilitated insurers to continue to provide terrorism coverage after 9/11.

Assessing Workers’ Compensation Risk from Terror Attacks in California

Reflecting this changing landscape, RMS conducted a terrorism risk study for the Workers’ Compensation Insurance Rating Bureau of California (WCIRB). The WCIRB is an unincorporated, private, non-profit association comprised of all companies licensed to transact workers’ compensation insurance in California and has over 400 member companies.

This study has received considerable market recognition, following our previous successful engagement to provide California earthquake risk assessment.

The objective of our study was to estimate California’s workers’ compensation losses to be retained by insurers due to terrorist acts, under TRIPRA for calendar year 2019. Please find a link to the study here.

RMS utilized the latest RMS® Probabilistic Terrorism Model (PTM) v4.2, released in 2018, which captures the most recent terrorism trends worldwide. This includes a shift in targeting strategies and weapons selection, such as the relative increase in the likelihood of small-scale attacks using armed attack modes rather than large-scale attacks using conventional bombs. This release also updates the target set – adding new targets due to the construction of new, high-profile, urban properties, and the removal of targets that no longer meet the criteria for target selection.

RMS’ analysis of the WCIRB portfolio suggests that there is a 0.01 percent probability (corresponding to a 10,000-year return period) that one or more attacks occurring at peak time (11 a.m.) of exposure, may exceed US$5 billion in net-loss to insurers, while the government retains about US$13 billion of the overall workers’ compensation losses. Similarly, a 1-in-5,000-year return period could result in about US$4 billion net loss to insurers with government retaining more than double the losses.

The methodology used to generate the exceedance probability curve focuses on large-scale attacks which are less likely to occur but can have significant losses.

While one finds some respite under TRIPRA, with the government retaining a large share of the losses caused by massive attacks (in the long return periods); on an average annual basis, insurers retain the bulk of the losses, since events that cause losses to exceed the deductible have very low likelihood of occurrence (less than 0.26 percent), thanks to pervasive countersecurity measures.

Multiple small conventional attacks are more likely to occur over a period of a year, contributing a major chunk in the average annual losses. But individually, these attacks are not large enough to trigger TRIPRA or exceed the deductible.

Terrorism is a mandatory coverage for workers’ compensation insurers, hence it is essential to invest in statistically valid estimates of the probability of large-scale attacks and associated losses. This will help them to evaluate the impact, funding, and appropriate risk allocation, and we believe this study will assist California insurers to assess the continued risk of terrorism under TRIPRA.

If you are interested in discussing the study or have questions, please feel free to reach out to us at support@rms.com.…

Shruti is responsible for RMS Global Terrorism and Human Casualty models and is involved in all aspects of these solutions, including the occasional consulting engagement. Prior to joining the RMS Product Management team, Shruti worked for four years in the RMS Global Analytical Services team.