Look around and you see the financial services industry being transformed by a newfound ability to tap into a vast amount of data, right at their fingertips. Where business decisions were reliant on intuition and experience, and transactions underpinned by the strength of relationships, data analytics now drives everything from credit rating to complaint handling, from social media-driven marketing to employee performance monitoring.

The (re)insurance industry is looking to follow suit. A tough regulatory and operating environment sees renewed focus on outperforming the competition through the utilization of data analytics and technology. Senior insurance executives collectively see data as where the business future lies; as one CEO recently said “data is the new oil.” Plenty of data exists, but for many it is currently locked in the back office, and what is required is to architect the business around the delivery of analytics to the front office where it will have the most impact. So, can the (re)insurance industry realize the benefits achieved by banking and capital markets, and how well-placed is the industry to capitalize on the oil beneath its own feet?

It is widely recognized that technological change will sweep across conventional business norms. A recent PwC Global CEO survey, shows eighty-six percent of insurance CEOs believe technology will completely reshape competition or significantly impact their industry over the next five years. New entrants, closer to the customer and unburdened by back office legacy systems, will inevitably eat the lunch of those existing players whose technology and processes evolved sporadically, becoming boxed in by practical constraints restricting their ability to change, such as:

Fragile ecosystems: For many (re)insurers, if they had to design their systems and processes again, it would look nothing like what they had in place today, with aging central systems, lots of bolt-on “point” solutions, patches, workarounds, random connections, and confusion. If the “system” gets in the way of performing everyday business, re-examine why time and money is being invested on poorly performing infrastructure that has become a business burden.

Processing time robs analysis time: A common complaint is that expert analyst teams can’t really do much actual analyzing as data entry, preparation, file management, and delays – staring at slowly moving progress bars – eats eighty percent of their time. Analyst morale must dip when an eight-hour batch run fails. Providing systems designed for their roles could restore this eighty percent back, providing precious analyst resource and expertise.

Data sources stuck in silos: Combining data sources, the “2+2 = 5” value concept, drives much of the value from data. For instance, achieving a linear chain through exposure, premium and payouts, through combining modeling, exposure, contracts and claims has obvious advantages. But with incompatible data sets, struggling analysis tools, and sheer processing power required makes this physically hard to achieve on-premise.

For many, harnessing the vast storage and computing power of the cloud offers the remedy to overcome these constraints; it may save costs but the constraints will still exist, it simply moves them off-premise. A fragile, disparate set of inefficient analytical tools and processes may creak less often and less obtrusively on the cloud, but transferring – rather than transforming – data analytics will only ever return moderate additional value from the same data. Those who have been tempted by this approach in the past will attest to:

Unfit technologies: Solutions architected for on-premise environments differ materially from those designed “cloud-first”; these solutions optimize cloud use for scalability, performance, availability, and integration of the latest technological innovations in the industry. Cloud-first solutions will always be more future-proof and cost-effective than on-premise technologies re-housed on the cloud.

Identity crises: Are you a consumer or a developer? A (re)insurer or a software house? Workflow and processing issues can be compounded by patching together different solutions on the cloud, and although a bespoke solution retains the experience on-premise, fresh development effort, continued maintenance, and on-going investment all distracts from the main business objectives. Tailor-made systems that can orchestrate data, systems, and processes together, will focus on business benefit, rather than system maintenance.

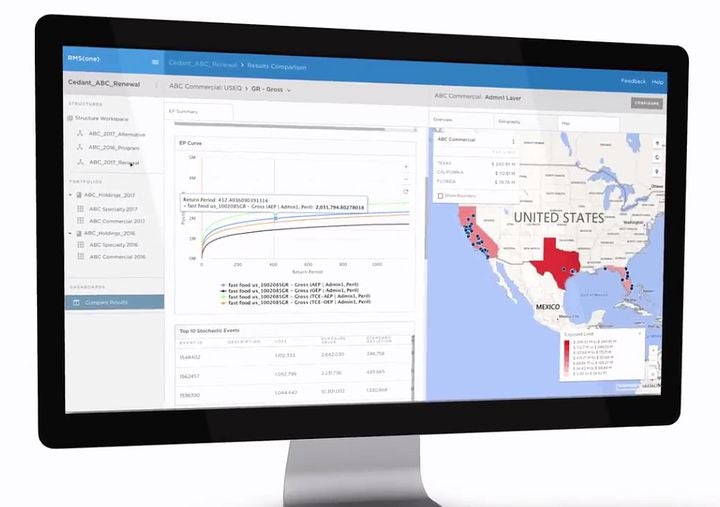

A low-change approach will take a long time to implement for minimal near or long-term business benefit. Getting serious about data means embracing new technology and new techniques, and pressures are mounting. RMS has recently announced the general availability of Risk Modeler. Risk Modeler is designed to support the (re)insurers’ quest to extract maximum insight from their risk data for underwriting, portfolio management and risk mitigation.

Risk Modeler screenshot

What are the benefits of supporting your underwriting nous with an analytic-driven approach? From the outset, it can deliver more informed underwriting and management decisions allowing better price adequacy assessment and more real-time understanding of portfolio threats. With the data to effectively assess new markets, products, and regions, responsiveness to accessing the right opportunities increases.

For users – the analytical experts in your midst – the paradigm of managing data, the cleansing, preparation, and transfer, is lifted, with timely insight straight to the decision makers who need it to make a difference to the business.

For your customers, a deeper understanding of the threats they are exposed to will help you consult on the most appropriate cover options. And from a capital adequacy viewpoint, you have real-time data to establish how much of your risk capital to “invest” in different opportunities, when to pull back participation and when to double-down in profitable activities.

Technological transformation in the industry is rapidly shifting from “why and when?” to “now and how?” The ones who will survive and thrive will see opportunities presented by innovation in technology and data analytics, and identify the right partners and solutions for their own objectives.

Those corporations will invest in the right resources and machinery to mine their riches – the alternative is trying to strike oil by sticking your head in the sand.

Share:

You May Also Like

January 23, 2023

Modernize Treaty Risk Analytics with Moody’s RMS TreatyIQ