Why the PRA’s stress test has pushed climate change to the top of (re)insurance company agendas

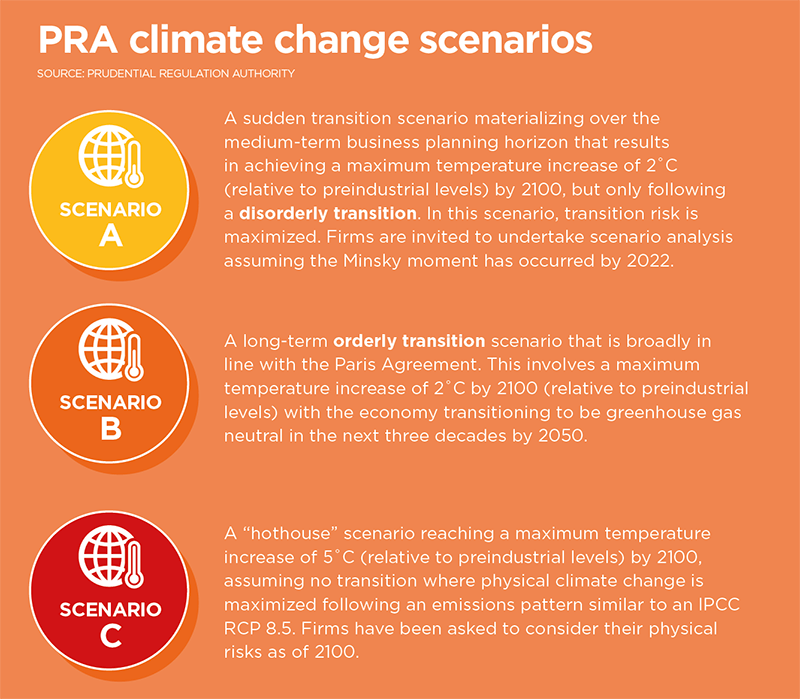

As part of its 2019 biennial insurance stress test, the U.K. insurance industry regulator — for the first time — asked insurers and reinsurers to conduct an exploratory exercise in relation to climate change. Using predictions published by the United Nations’ Intergovernmental Panel on Climate Change (IPCC) and in other academic literature, the Bank of England’s Prudential Regulation Authority (PRA) came up with a series of future climate change scenarios, which it asked (re)insurers to use as a basis for stress-testing the impact on their assets and liabilities.

The PRA stress test came at a time when pressure is building for commercial and financial services businesses around the world to assess the likely impact of climate change on their business, through initiatives such as the Task Force for Climate-Related Financial Disclosures (TCFD). The submission deadline for the stress-tested scenarios ended on October 31, 2019, following which the PRA will publish a summary of overall results.

From a property catastrophe (re)insurance industry perspective, the importance of assessing the potential impact, both in the near and long term, is clear. Companies must ensure their underwriting strategies and solvency levels are adequate so as to be able to account for additional losses from rising sea levels, more climate extremes, and potentially more frequent and/or intense natural catastrophes. Then there’s the more strategic considerations in the long term — how much coverages change and what will consumers demand in a changing climate?

The PRA stress test, explains Callum Higgins, product manager of global climate at RMS, is the regulator’s attempt to test the waters. The hypothetical narratives are designed to help companies think about how different plausible futures could impact their business models, according to the PRA. “The climate change scenarios are not designed to assess current financial resilience but rather to provide additional impetus in this area, with results comparable across firms to better understand the different approaches companies are using.”

“There was pressure on clients to respond to this because those that don’t participate will probably come under greater scrutiny”

Callum Higgins

RMS

RMS was particularly well placed to support (re)insurers in responding to the “Assumptions to Assess the Impact on an Insurer’s Liabilities” section of the climate change scenarios, with catastrophe models the perfect tools to evaluate such physical climate change risk to liabilities. This portion of the stress test examined how changes in both U.S. hurricane and U.K. weather risk under the different climate change scenarios may affect losses.

The assumptions around U.K. weather included shifts in U.K. inland and coastal flood hazard, looking at the potential loss changes from increased surface runoff and sea level rise. While in the U.S., the assumptions included a 10 percent and 20 percent increase in the frequency of major hurricanes by 2050 and 2100, respectively.

“While the assumptions and scenarios are hypothetical, it is important (re)insurers use this work to develop their capabilities to understand physical climate change risk,” says Higgins. “At the moment, it is exploratory work, but results will be used to guide future exercises that may put (re)insurers under pressure to provide more sophisticated responses.”

Given the short timescales involved, RMS promptly modified the necessary models in time for clients to benefit for their submissions. “To help clients start thinking about how to respond to the PRA request, we provided them with industrywide factors, which allowed for the approximation of losses under the PRA assumptions but will likely not accurately reflect the impact on their portfolios. For this reason, we could also run (re)insurers’ own exposures through the adjusted models, via RMS Analytical Services, better satisfying the PRA’s requirements for those who choose this approach.

“To reasonably represent these assumptions and scenarios, we think it does need help from vendor companies like RMS to adjust the model data appropriately, which is possibly out of scope for many businesses,” he adds.

Detailed results based on the outcome of the stress-test exercise can be applied to use cases beyond the regulatory submission for the PRA. These or other similar scenarios can be used to sensitivity test possible answers to questions such as how will technical pricing of U.K. flood be affected by climate change, how should U.S. underwriting strategy shift in response to sea level rise or how will capital adequacy requirements change as a result of climate change — and inform strategic decisions accordingly.

{kind=link}