Bank of England CBES: Five Thoughts on Tackling Climate Change Physical Risk Reporting

Joss MatthewmanMarch 08, 2021

The Bank of England’s Climate Biennial Exploratory Scenario (CBES) exercise launches in June, with submissions required by the end of September 2021. Less than four months remain until the official launch, so the Bank of England (BoE) is engaging early with invited insurers and banks to ensure they understand the direction and scope of the assessment.

Announced in December 2019, the BoE’s stated objective for the CBES is “to test the resilience of the current business models of the largest banks, insurers, and the financial system to the physical and transition risks from climate change. The exercise will provide a comprehensive assessment of the U.K. financial system’s exposure to climate-related risks and therefore the scale of adjustment that will need to be undertaken in coming decades for the system to remain resilient.”

In many respects, we believe this exercise takes the logical next step from the BoE’s 2019 General Insurance Stress Test (GIST), which included an exploratory exercise to establish the impact of three climate change scenarios on both the value of investments and potential liabilities arising from physical risk and transition risk from U.S. hurricanes and U.K. flood events. Each scenario varied in timescales and severity and was based on the global action to transition to a low- or no-carbon future.

Early details have emerged, including scope on the three climate scenarios (No Additional Policy Action, Early Policy Action, and Late Policy Action) and the variables to be used in the CBES. Knowing that the CBES will be released in June, what can the intended recipients do now to prepare?

Responding to Climate Change Regulations

The GIST presented a new challenge to many of our clients. We soon learned that thinking beyond that traditional risk period, even through to the year 2100, required a different approach. RMS partnered with many clients to help with their submissions to the BoE using risk models that were modified to reflect the specified criteria scenarios.

We expect that many lessons from the GIST will shape the upcoming CBES. Though details are still to be fully defined, it is safe to assume that the CBES will remain focused on testing the vulnerability of today’s balance sheets to climate change. In addition, it will likely evaluate how a business might adapt their business model over the length of a given scenario.

Participants can expect the CBES will be bigger and more complex and the demands will be greater. Climate science has also moved fast and, to match, so will the modeling capabilities. The scenarios will again focus on the impact from climate change on physical and transition risks, though they will be broader in scope. One key difference will include recognizing the wide-ranging impact of climate-related financial risks, through multiple possible pathways and climate outcomes. This will require participants to analyze multiple scenarios over a longer time frame.

Preparing for the CBES

RMS has been here before. In addition to helping clients with the GIST in 2019, we have also worked with (re)insurers and regulators to assess the impact climate change factors have on physical risk. Clients such as QBE wanted to understand how their insurance portfolio would be impacted by recognized IPCC climate change pathways, using adjustments to RMS models.

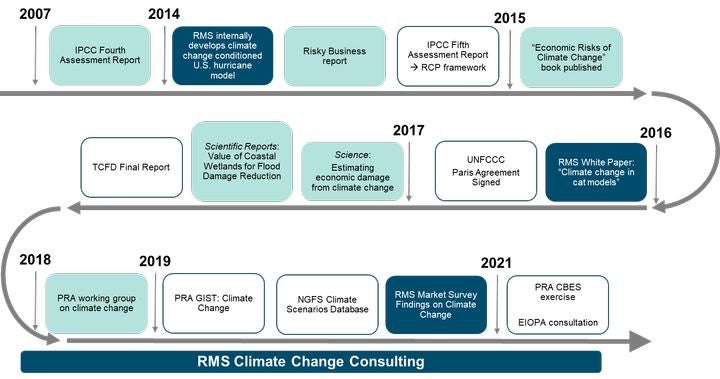

Figure 1: Key RMS climate change milestones

From our experience working with many clients, we have five thoughts on what all (re)insurers – not just those that have to respond to the CBES – should start to do now with regard to assessing the changes in physical risk from climate change:

Build for the future: Exercises such as the CBES aren’t the first and certainly won’t be the last climate change reporting demands from a regulator. Using a partner who can help build foundations for the longer term makes clear business sense. This partner can also provide expertise to accommodate new demands, introduce repeatable processes, and move away from just answering the test toward something much more sustainable.

Make it business as usual: Although perhaps novel at the moment, climate change needs to be embedded in your processes and in the mainstream. Use an approach that enables climate risk analytics to be folded into your day-to-day workflows, since at some point it is quickly going to be a core requirement.

Ensure consistency with your present-day views of risk: Separated views may work in the short term, but a single view of risk will help as you build sophistication in your approach, to understand future capital positions in a consistent manner.

Develop capacity and understanding of the problem: Many of our clients are moving along their climate change analytics journey to understand the issues, risk drivers, challenges to their business, and potential mitigation strategies. Now is the time to make smart investments to kick-start climate change knowledge capacity in your business.

Differentiate your business: Climate analytics can offer areas of competitive advantage, so use this as an opportunity to lead on climate change. Go beyond the standard requirements to generate views that reflect your portfolio, rather than industry averages. Risk varies by region, and correlation across portfolios is critical. Ours is an industry that prides itself on sophisticated climate risk management and can embrace climate change to move toward a gold standard.

There is not long to go until the CBES is published, so it’s time to start planning now. If you need any help, talk to us. Consider us a partner who has already had success responding to regulators and can help your business build a long-term strategy – so you can understand and start to address challenges posed by climate change.

From our numerous client conversations, climate change as a business issue has risen high on the agenda, and this has certainly escalated over the last twelve months. There is a growing recognition of the need to quantify the impact that climate change will have on your business. But – where do you start with this? One of the major challenges is knowing what question to ask. With the inclusion of climate change scenarios within the General Insurance Stress Test (GIST 2019), which the larger U.K. insurers and Lloyd’s syndicates are required to respond to, the Bank of England Prudential Regulation Authority (PRA) is outlining one approach.

RMS is particularly well placed to support insurers in responding to the “Assumptions to Assess the Impact on an Insurer’s Liabilities” portion of the climate change section within GIST, which examines how changes in U.S. hurricane and U.K. weather risk under different climate change scenarios may affect losses.

Stochastic models are the perfect tools to evaluate such physical climate change risk to liabilities, with the ability to reflect changes to the hazard under different climate change views and providing a clear link between cause and effect. Our contribution to the landmark “Risky Business” report in 2014 looking at sea-level rise in the U.S. to 2100 is a key example of this. As such, RMS has developed internally adjusted views of its U.S. hurricane, U.S. flood, U.K. windstorm and U.K. flood models to reflect most of the assumptions and scenarios from the PRA, detailed in the table below:

The PRA is asking for the potential impact of these assumptions and scenarios on the Annual Average Loss (AAL) and 1-in-100 Aggregate Exceedance Probability (AEP) loss for all relevant U.S. and U.K. insurance contracts. Getting to a reasonable assessment of these numbers however is not a trivial exercise, requiring the appropriate adjustment of model data in up to 18 possible assumption scenario combinations, and then the analyses of the relevant exposure against these.

To help insurers start thinking about how to respond to the PRA request, RMS can provide broad industry-wide factors derived by running industry exposure over the adjusted models. This “Industry Factors Package” will be made available to RMS clients, while others who wish to access these will be able to license them separately. The industry-wide factors will allow for the approximation of losses under the assumptions and scenarios laid out in the table above, however there could be significant limitations to this approach for individual companies and portfolios. Your exposure, or risk profile, will not reflect that of the industry and therefore the application of industry-wide factors may not reasonably reflect your own risk. The uncertainty around this approach means you may decide this is not a satisfactory solution for your submission.

For a more detailed bespoke view, we are offering to run insurers’ own exposures through the adjusted models, via RMS Analytical Services, to better satisfy the PRA’s requirements. This “PRA-ready Package” provides unique results for submission to the PRA which reflect your book of business and allow for comparisons with those of the industry.

Even if you fall out of the larger U.K. insurers and Lloyd’s syndicates for whom this applies, you should take note. This might be the start of a new wave of analytical rigor around climate change, and more regulators are likely to follow. Beyond regulation, it is also becoming fundamental to understand the impact of climate change for business decisions. For example, to answer what is insurable in 2050 and whether you need to adjust your underwriting and portfolio management strategy accordingly.

RMS can assist in getting answers to such questions through a customized climate change consulting engagement as part of an “Enhanced Climate Change Package”, utilizing advanced climate change analytics to provide more detailed results based on the PRA or other similar scenarios. This package can include the PRA-ready results and basic PRA climate change submission information or be a separate engagement depending upon your needs.

RMS clients who are interested in these solutions should reach out to their Client Success Manager for details on how they can be accessed, while other insurers can email sales@rms.com. With the submission date of October 31 looming, and many with tighter internal deadlines, it is important not to delay! Indeed, we are already engaging with several clients on how we can help them.

Senior Director, Product Management and Strategy, RMS

Joss Matthewman recently rejoined RMS as Senior Director of Product Management and Strategy, leading on RMS’s climate change activities. Prior to this, Joss was Head of Catastrophe Exposure Management at Hiscox, responsible for natural catastrophe, war, terror, and political violence exposure management and reporting across the group.

Before joining Hiscox, Joss spent seven years in model development at RMS, where he worked on the RMS North Atlantic Hurricane and Asia Typhoon models, before being appointed Head of Storm Surge Modeling. During this period Joss joined the PRA working group on climate change which he continues to engage with today.

Prior to entering the insurance industry Joss obtained a PhD in Applied Mathematics from UCL and worked as a postdoctoral researcher in climate science at the University of California, Irvine. His published areas of research during this time include stratospheric sudden warmings and the impact of sea-ice on global atmospheric teleconnections.