Unlike most U.S. property and casualty insurance, whose take-up rates range from ten percent (California residential earthquake) to greater than 90 percent (for fire insurance), workers’ compensation insurance is required by law. In California, nearly all of the 18.5 million employees across the state are covered by workers’ compensation, whether through an employer’s policy or self-insurance. This enormous exposure generates more than US$18 billion in premium annually, and because California is an “exclusive remedy” state, injuries arising out of and in the course of employment resulting from an earthquake are not excluded.But how can the cost of this obligatory, high risk exposure be measured?

The Workers’ Compensation Insurance Rating Bureau of California (WCIRB), an unincorporated, nonprofit association, has over four hundred member companies who are licensed to transact workers’ compensation insurance in California. For more than a century the WCIRB has built a reputation as California’s trusted, objective provider of actuarially-based information and research. Members rely on the WCIRB to help accurately measure the cost of providing workers’ compensation benefits, and in total the members are responsible for insuring annual business payroll amounting to US$544 billion.

We were delighted to be approached by the WCIRB and partner with them to help understand this risk. The deliverable was a report based on a high resolution, big data and probabilistic earthquake analysis on a risk portfolio containing the policy and exposure data for the business payroll insured by members of the WCIRB.

WCIRB Member Portfolio

The portfolio provided by the WCIRB contained exposure for more than 11 million full-time equivalent (FTE) employees, including information about the occupation of each employee. Los Angeles, Santa Clara, and Orange Counties had the highest concentrations of FTE and payroll, accounting for almost 50 percent of the total. These high concentrations of employees and payroll also tended to be in high hazard regions, close to major fault lines.

Modeling Approach

The earthquake analysis was performed using Version 17 of the RMS® North America Earthquake Casualty Model, released in May 2017, which incorporated the latest science in earthquake hazard and vulnerability research. This includes a robust implementation of Uniform California Earthquake Rupture Forecast Version 3 (UCERF-3); a comprehensive event set including severe “tail events” causing damage in both Northern and Southern California; new vulnerability functions for very tall buildings; and ultra-high resolution approaches to soil, liquefaction and landslide modeling.

Key Factors Considered

Some of the factors considered during this analysis included:

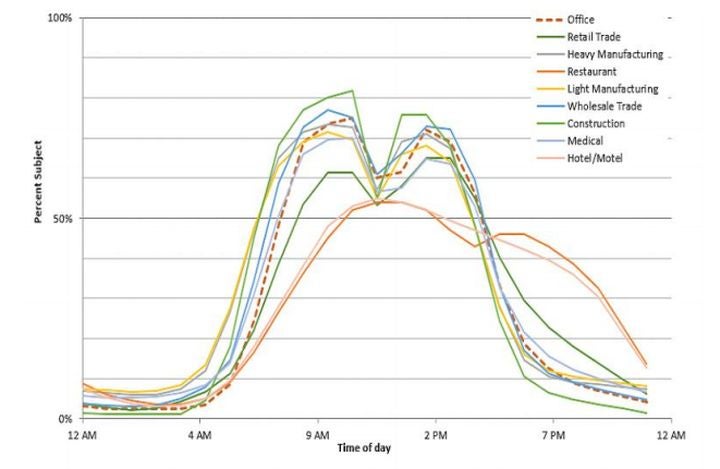

Time of day: The timing of an earthquake event is a critical factor when assessing the risk to employees. Recent earthquake events in California such as the Loma Prieta Earthquake (1989) and the Northridge Earthquake (1994) happened during off-peak hours; had the timing been different, the human impact could have been much worse.

Figure 1: Industry average occupancy levels by time of day – weekday

Exposure distribution: For California, the areas of highest workers’ compensation exposure also tend to be the areas of highest earthquake risk, which from an insurer’s viewpoint, makes it very hard to diversify.

Data quality: Given that injuries are dependent on building damage and collapse, modeled results are very sensitive to the underlying exposure data. Positional accuracy of an exposed location greatly influences the retrieval of geotechnical data (e.g., soil type). Building attributes govern the distribution of structural damage and potential for building collapse.

Results

From our analysis for the WCIRB, we calculated that the average annual estimated insured loss is US$29 million, which corresponds to 0.005 percent of total insured payroll and $2.52 per employee.

The 1 in 100-year insurance loss is expected to exceed US$300 million and 300 fatalities. If the 1 in 100-year event was assumed to occur in peak work-time hours, the estimated expected losses are approximately US$1.5 billion. The 1 in 250-year loss may exceed US$1.4 billion and more than 1,000 fatalities, at peak work-time hours, the estimated expected losses are approximately US$5.1 billion.

Due to the rare occurrence, high severity, and inherent uncertainty in earthquake casualty events, the tail risk (i.e. long return period loss) is high. The 1 in 500-year loss is at least US$3.5 billion; the 1 in 1,000-year loss is at least $6.4 billion.

Injuries involving “permanent total disability”, a rare form of injury which often requires lifetime wage replacement and medical care, were a major driver of overall estimated costs, accounting for more than 35 percent of expected annual loss.

RMS analysis suggests that there is a one percent probability (corresponding to the 100-year return period) that one or more events will cause at least US$300 million in ground-up (total) loss from 4,758 casualties, accounting for temporal work patterns of different occupations. There is a one percent probability of losses exceeding US$1.4 billion if an event were to occur during peak exposure.

On a long-term average basis, the WCIRB portfolio is expected to sustain about US$29 million in average loss per year (average annual loss), which corresponds to an average loss rate per $100 payroll of $0.005 and an average loss rate per FTE of $2.52. At peak exposure, the WCIRB portfolio is expected to sustain US$84 million in average loss per year, which corresponds to an average loss rate per $100 payroll of $0.016 and an average loss rate per FTE of $7.43.

Examining Past Events

In the report we also looked at past events to see what the impact these would have on the working population today — especially if the event occurred during the working day. On April 18, 1906, at 5:12 a.m. local time, an M7.8 earthquake shook the city of San Francisco and the surrounding region for approximately 45 to 60 seconds, and is by far the most destructive earthquake in North America for more than a hundred years. For the WCIRB portfolio, the total loss, accounting for the temporal work patterns of different occupations, would result in 7,261 injuries and US$1.04 billion of loss. At peak occupancy, losses could exceed US$3.176 billion from 22,070 injuries.

The compulsory inclusion of earthquake injury cover is unique to the workers’ compensation line of business. We are hopeful that this analysis will enable California comp writers to more comprehensively understand the earthquake risk (and uncertainty) facing their portfolios, and policymakers to gain a better view of the potential impact of an earthquake on the California economy.

Share:

You May Also Like

October 17, 2019

Is It Time to Break up With Your Deficient Risk Scoring Analytics?

Chris Folkman is a senior director of product management at RMS, where he is responsible for specialty lines including terrorism, casualty, wildfire, marine cargo, industrial facilities, and builders' risk. He has extensive experience on both the broker and carrier sides of insurance, where he has led many aspects of property and casualty operations including underwriting, pricing, predictive analytics, regulatory affairs, and third-party commercial coverage and claims.

Prior to RMS, he was a managing director at CompWest Insurance Company, a workers’ compensation start-up that was acquired by Blue Cross Blue Shield of Michigan. Chris holds a bachelor's degree from Stanford University. He is a licensed insurance broker and a Chartered Property and Casualty Underwriter (CPCU).