High-quality catastrophe exposure data is key to a resilient and competitive insurer’s business. It can improve a wide range of risk management decisions, from basic geographical risk diversification to more advanced deterministic and probabilistic modeling.

The need to capture and use high quality exposure data is not new to insurance veterans. It is often referred to as the “garbage-in-garbage-out” principle, highlighting the dependency of catastrophe model’s output on reliable, high quality exposure data.

The underlying logic of this principle is echoed in the EU directive Solvency II, which requires firms to have a quantitative understanding of the uncertainties in their catastrophe models; including a thorough understanding of the uncertainties propagated by the data that feeds the models.

The competitive advantage of better exposure data

The implementation of Solvency II will lead to a better understanding of risk, increasing the resilience and competitiveness of insurance companies.

Firms see this, and more insurers are no longer passively reacting to the changes brought about by Solvency II. Increasingly, firms see the changes as an opportunity to proactively implement measures that improve exposure data quality and exposure data management.

And there is good reason for doing so: The majority of reinsurers polled recently by EY (formerly known as Ernst & Young) said quality of exposure data was their biggest concern. As a result, many reinsurers apply significant surcharges to cedants that are perceived to have low-quality exposure data and exposure management standards. Conversely, reinsurers are more likely to provide premium credits of 5 to 10 percent or offer additional capacity to cedants that submit high-quality exposure data.

Rating agencies and investors also expect more stringent exposure management processes and higher exposure data standards. Sound exposure data practices are, therefore, increasingly a priority for senior management, and changes are driven with the mindset of benefiting from the competitive advantage that high-quality exposure data offers.

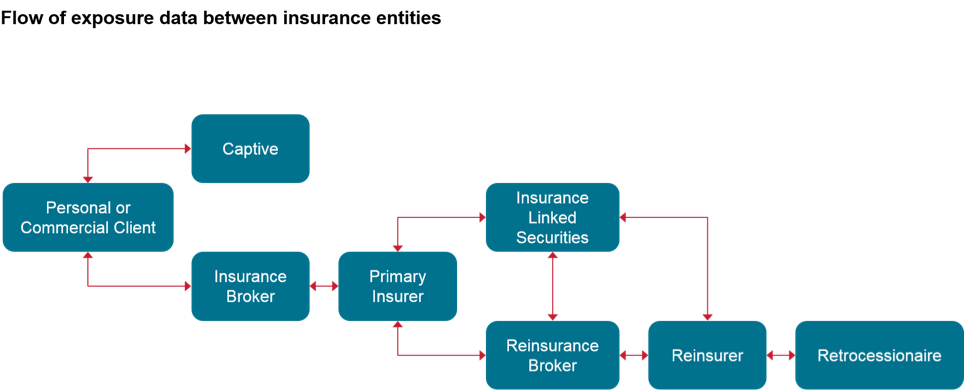

However, managing the quality of exposure data over time can be a challenge: During its life cycle, exposure data degrades as it’s frequently reformatted and re-entered while passed on between different insurance entities along the insurance chain.

To fight the decrease of data quality, insurers spend considerable time and resources to re-format and re-enter exposure data as its being passed on along the insurance chain (and between departments within each individual touch point on the chain). However, due to the different systems, data standards and contract definitions in place a lot of this work remains manual and repetitive, inviting human error.

In this context, RMS’ new data standards, exposure management systems, and contract definition languages will be of interest to many insurers; not only because it will help them to tackle the data quality issue, but also by bringing considerable savings through reduced overhead expenditure, enabling clients to focus on their core insurance business.