Overcoming the Practical Challenges in Operationalizing ESG Underwriting Analytics

Shaheen RazzaqJune 07, 2023

The insurance industry is undergoing a significant transformation in how it approaches environmental, social, and governance (ESG) factors as a framework that informs business strategy. There are two distinct approaches to ESG adoption within the industry, each with its own set of challenges.

At one end of the spectrum, some firms are taking a bottom-up approach to ESG. These firms may establish exclusionary business criteria for their underwriting, for example, oil and gas projects, and update their guidelines to align with specific sustainability objectives.

This allows them to begin their journey sooner, even though this approach tends to only focus on the ‘E’ of ESG. Getting underwriters to consider sustainability at the point of decision-making is the first step toward making a meaningful impact.

On the other end of the spectrum, there are firms that have holistically embraced ESG commitments but struggle to make tangible progress on them.

These companies tend to take a top-down approach, taking a balanced view across E, S, and G, with the C-suite making commitments to both internal and external stakeholders like shareholders.

Such commitments have raised the profile of ESG within the industry and sparked important conversations about the role of insurers in addressing issues like climate change and pay equity. However, we hear from a rapidly growing number of insurers who often lack the tools and capabilities necessary to operationalize these commitments.

According to a recent survey by Moody's RMS, 81 percent of insurers have made commitments to ESG principles, demonstrating their readiness to embrace ESG, and going beyond just exclusionary criteria. However, incorporating ESG into underwriting and portfolio management decision-making poses numerous practical challenges for (re)insurers.

In this blog, we will explore these challenges and how Moody's RMS designed ExposureIQ™, our cloud-native exposure management application, to address them. Let’s look at the challenges first.

Data Availability for Private Enterprises

Insurers often deal with diverse portfolios that include both private and public companies, with the number of private companies usually dwarfing the number of public ones. To underwrite effectively, (re)insurers need to assess ESG factors for all businesses they quote for, regardless of size. However, obtaining and analyzing ESG data for private companies is particularly challenging.

Unlike publicly quoted companies, private enterprises are under less obligation to publicly disclose sustainability information, leading to a reliance on proprietary data or methodologies that lack transparency.

Complex Workflow Integration

It’s rare to find an insurer’s sustainability organization and the underwriting or portfolio management disciplines working on the same floor, or even in the same office or building. These functions have historically operated in silos, each built upon independent IT infrastructure, making data accessibility and migration complex and challenging.

In this respect, the convergence of ESG data analytics with risk management presents unique obstacles for property and casualty (P&C) insurers. Incorporating ESG factors into underwriting or portfolio management workflows requires expertise in catastrophe risk and the underwriting process.

With sustainability and underwriting teams just beginning to collaborate on sustainable underwriting, how can we expect P&C insurers to operationalize ESG analytics into their complex, managed workflows in line with their external commitments?

Lack of Industry Frameworks

ESG is a priority for insurers but is still relatively new, and as a result, industry standards have not yet been fully developed or formalized. This lack of established frameworks and divergent approaches to measuring ESG performance makes it difficult for P&C insurers to evaluate their risk against their peers.

Without a clear set of standards, firms struggle to evaluate the impact of the 'E versus S versus G' in insurance underwriting in a consistent way, as insurers navigate a patchwork of reporting guidelines, which can vary based on which market they are in or whether they are participating in an ESG alliance.

Until standards develop, ESG data alone will not satisfy the requirements for building a comprehensive view of risk. Firms must take an iterative approach to how they are building their view of risk, with the ability to adapt the weight of different factors to ensure that they can align with evolving ESG guidelines. A simple ‘set it and forget it’ approach for evaluating ESG exposure will fail to capture how ESG is an evolving discipline.

Use of Credible ESG Data

The foundation of any effective ESG underwriting solution needs to be able to access credible company ESG data, and where any gaps occur, such as with private sector companies, robust, validated methodologies are needed to fill these gaps.

Moody’s ESG analytics in the ExposureIQ application uses Moody’s market-leading, granular ESG database with ratings for millions of businesses, together with methodologies that utilize this vast database to assess businesses not already included.

This extensively validated, detailed data provides confidence to (re)insurers for underwriting at the individual business level, and Moody’s ESG database is also continually evolving and improving.

Overcoming ESG Integration Issues Using a Unified Platform

To overcome ESG integration issues, P&C insurers require a unified platform. Incorporating ESG analytics into underwriting workflows should be seamless, akin to adding any new application or data set.

With ExposureIQ running on Moody's RMS Intelligent Risk Platform™, ESG analytics becomes just another risk factor to select within the application. And with the RMS unified data store, new post-bound policies seamlessly feed into ExposureIQ, ensuring minimal disruption to real-time exposure and portfolio management.

Maintaining Flexibility as Standards Develop

Recognizing that ESG data and standards will evolve, the ExposureIQ application using Moody’s ESG Insurance Underwriting Solution is built for the future.

As standards evolve, users can adapt the scoring of over 270 different ESG factors based on their risk perspective, including customizing weights for each factor. The current solution aligns ESG scores with the United Nations Sustainability Goals, allowing for flexibility in assigning weights.

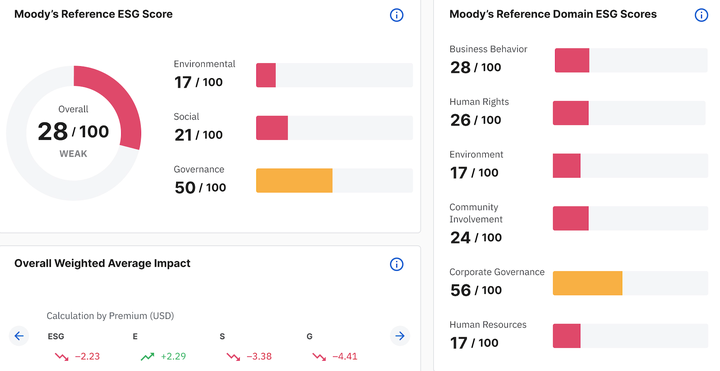

Screenshot of Moody's RMS ExposureIQ application displaying ESG factors

Conclusion

With the release of ESG analytics as part of the ExposureIQ application in June, (re)insurers will be equipped with the tools and capabilities to help take a significant step forward in delivering upon ESG commitments set by company leadership.

Shaheen has over a decade of experience delivering risk management solutions to insurance and reinsurance companies. As Vice President - Product Management at Moody's, he is responsible for introducing new, innovative applications to the market.

Before joining Moody's, Shaheen was Risk Aggregations Business Unit Manager at Room Solutions Ltd. and led a department that designed and developed Exact Advantage, a popular, next-generation offshore energy risk aggregation tool. At Room Solutions Ltd, he then managed a global development team that built and successfully implemented several contract and exposure management solutions for large European commercial insurance organizations.

As a regular speaker at industry events, Shaheen often gives presentations about the business value technology delivers to organizations that manage catastrophe and non-catastrophe risk.

Shaheen holds a master’s in business and information technology from Kingston Business School.