Insurance-Linked Securities: Demonstrating Resilience Through Tough Times

Callum O’RourkeDecember 01, 2020

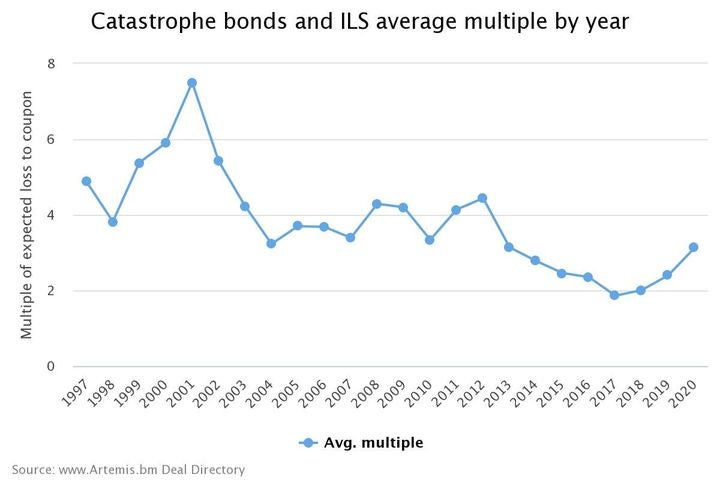

Despite being a relatively new asset class, the insurance-linked securities (ILS) market has had its fair share of milestones when it comes to the spreads available at issuance. Spreads are defined as the “coupon,” or interest payments, that are in excess of a high-quality or risk-free collateral return. Figure 1 charts the average coupon/expected loss multiple for catastrophe bond transactions issued each year from 1997 to the present day. This shows the multiple of the expected loss that investors are receiving in terms of coupon; higher uncertainty can act as a potential driver for investors to demand a higher risk premium.

Looking at Figure 1, 2001 represented a watershed moment for the market as the average expected loss multiple hit a peak of 7.5. After 2001, the market followed an overall pattern of decline through to 2017, but with some notable brief increases, such as the years following high-frequency losses (e.g., Hurricanes Katrina, Rita, and Wilma in 2005).

The year 2017 saw the lowest multiple in the history of the asset class. On average, a transaction issued in this year could have expected a coupon of 1.86 times the expected loss. This was a 300 percent reduction compared to 2001, and a 9 percent decrease year-on-year. But since 2017, the market has been on an upswing. This intrigued me.

Figure 1: Average multiple of catastrophe bond and insurance-linked securities (ILS) deals issued by year (Source: Artemis)

These consistently decreasing multiples from 2012 that bottomed out in 2017 can be explained by a combination of factors: low loss years and availability of capital. As ILS became more understood as an asset class, more capital entered the market. Multi-asset investors, such as pension funds, were attracted to the diversification benefit and the relatively attractive spreads when compared with other opportunities in a low-interest, “money-is-cheap” world.

This abundance of capital, compounded with relatively low losses between 2010 and 2017, created a constant downward pressure on spreads until the historical minimum average multiple of 1.86 was reached in 2017. A hurricane season that included Harvey, Irma, and Maria – plus the emergence of wildfire as a peak peril, meant 2017 proved to be a challenge for ILS investors. Multiple catastrophe bonds were triggered that year, or even exhausted – resulting in the complete loss of bond principal.

Due to the losses experienced in 2017, many ILS managers witnessed increases in their assets under management (AUM) as the investor community anticipated that spreads would rise in 2018. However, although 2018 spreads were more attractive (as shown by the uptick in Figure 1), the increases were below expectations. Further noticeable losses came in 2018 with Hurricane Michael, Typhoon Jebi, and a second record-breaking California wildfire season. These combined losses then resulted in another spread rise in 2019 which was not in-line with expectations, prompting a decrease in capital availability. Some investors exited the ILS market altogether. However, it was clear in the 2020 January renewals that ILS investors would now be demanding more return for their risk to account for recent loss years.

Since the World Health Organization declared COVID-19 a global pandemic in March 2020 – with subsequent lockdowns and restrictions across the world and over 63 million confirmed COVID-19 cases to date – financial markets saw an inevitable increase in volatility across several sectors. However, the prospect of effective vaccines has recently brought hope of normality, and a potential stock market rally.

Traditionally, the wisdom of holding an allocation in ILS transactions is the diversification benefit it affords multi-asset portfolios. But as the pandemic took hold, many ILS investors with multi-asset portfolios, slightly counterintuitively, sold their positions in their 144a bonds to take advantage of tactical opportunities in other markets, such as distressed equity. This activity should be celebrated as a success of the liquidity available within the asset class, since the prices of most 144a transactions remained stable (except for some bonds explicitly covering excess mortality and morbidity risk), as investor confidence in their value remained.

Examining life risks against the backdrop of COVID-19, there have been a flurry of notable new life transactions including Matterhorn 2020-2 A, La Vie 2020-1, and Vitality XI 2020. Many ILS managers operate a life strategy alongside their property and casualty (P&C) funds, and as the risks become better understood, COVID-19 is likely to accelerate this development and interest.

RMS® is well respected in the ILS community for modeling life transactions, as reflected in the deal execution for the Matterhorn and La Vie transactions for which we provided the risk analysis. RMS used our suite of excess mortality and morbidity models – which cover infectious disease, pandemics, terrorism, earthquakes, and other perils – including a contribution to the expected loss from the COVID-19 pandemic.

But even as potential vaccines for COVID-19 bring hope, the world continues to face significant challenges in tackling this pandemic. What implications does the ongoing situation have for the ILS market? These current conditions, with investors demanding more return for their risk and opportunities in other markets, have created an environment that has seen significant spread increases for 2020 issuances. To date, US$13.5 billion in notional capital has been issued in 2020, with the average multiple almost 40 percent higher than the midpoint of the 2018 and 2019 average multiples. Spreads are difficult to predict, so we will see if they continue to increase or flatten out in the upcoming years.

The COVID-19 pandemic has created challenges for the ILS market, but by emerging through 2020 with attractive spreads and a strong set of issuances, ILS has written another chapter in its history of resilience. ILS has demonstrated time and again that it is here to stay as an excellent diversifier against broader economic uncertainty, as shown by its emergence through key moments in its short history – in 2005 (Katrina, Rita, Wilma), the 2008 financial crash, and now with COVID-19.

Regarding risk supply, the ILS market has never been in such a healthy position with US$44.8 billion notional capital outstanding today, a peak for the asset class. Because of these factors, I and my colleagues are optimistic that ILS will see new market participants as well as returning investors for the next renewals. Leveraging a team of dedicated ILS specialists, RMS continues to innovate in this space by providing services for efficient risk transfer and insightful analytics needed to make informed investment decisions.

Callum has worked at RMS for seven years and is an expert in RMS’ Insurance-Linked Securities (“ILS”) product offering.

His work is primarily focused on enabling ILS fund managers to leverage RMS model science, to help quantify exposure to catastrophe risk, make portfolio management decisions and communicate with end-investors.

His responsibilities include business development activities as well as leading the analytics for bespoke projects to support ILS fund managers, including underwriting/portfolio management support, reporting and valuations.

Callum holds a master's degree in Applied Mathematics from Imperial College and is a Chartered Financial Analyst (CFA).