New Strategies Needed to Manage Mortgage Default Risk from Natural Catastrophes

Arnaud CastéranOctober 22, 2020

In the early hours of January 17, 1994, a Mw6.7 earthquake struck northwestern Los Angeles, causing 57 fatalities and up to US$40 billion of direct damage. The Northridge event changed the insurance landscape dramatically. According to the Insurance Information Institute, the industry ended up paying out more in claims for Northridge than it had collected in earthquake premiums over the preceding 30 years. Insurers started limiting their earthquake exposure, writing fewer new policies, and increasing rates and deductible levels. Even with the subsequent creation of the state-backed California Earthquake Authority – the largest provider of residential earthquake insurance in the U.S. – only around 11 percent of the residential market in California is currently insured against earthquakes.

RMS® analysis shows that an event of similar size to Northridge can be expected every 40 years. More extreme events could produce dramatically larger impacts; a repeat of the 1906 Mw7.8 San Francisco Earthquake would cause a total loss to residential properties twice that of the Northridge quake.

Bridging the Protection Gap

This raises the question of who pays the bill when the next event strikes: Who bridges this glaring protection gap? It will be homeowners and mortgage providers that are first impacted. Over the first five months of 1995, a year after Northridge, home foreclosures in the San Fernando Valley increased by 19 percent, and half of the foreclosures involved quake-damaged homes.

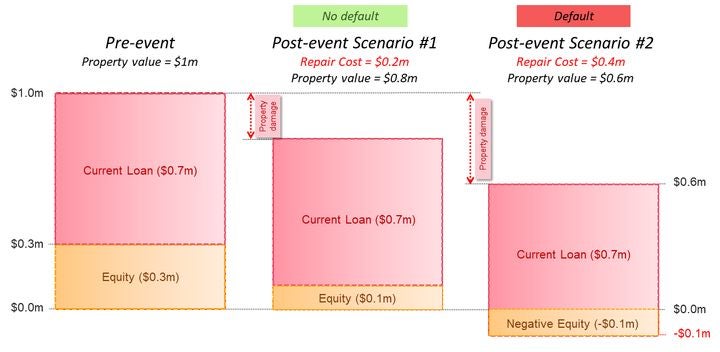

Foreclosures happen because structural damage from earthquakes causes the market value of a property to plummet. If a property value falls below the outstanding loan value, the borrower is faced with negative equity (see Figure 1). And research has revealed a strong correlation between negative equity and mortgage default.

Figure 1: Modeling negative equity and mortgage default (all amounts are in U.S. dollars)

The West Coast of the U.S. is a particularly striking example illustrating the combination of factors, with a booming mortgage market (20 percent increase in the volume of new mortgages between 2018 and 2019 in California and 26 percent in Oregon and Washington), low earthquake insurance penetration and a concentration of expensive assets in large metropolitan areas located in high-risk zones (Los Angeles, San Francisco, Seattle and Portland). Other risk factors such as wildfire and sea level rise, also impact California, and other areas in the U.S., such as the Midwest, combine high flood risk and low insurance coverage.

Data-Driven Solutions for the Real Estate Sector

Measuring natural disaster-driven mortgage default is a challenging task. Indirect effects of disasters, such as long-term land devaluation, mass unemployment, and a “ghost town” effect, are hard to predict. The scarcity of historical data, changes in insurance practices since significant events like Northridge, and rapid changes in exposures make a reliance on past experience insufficient to provide the real estate sector with an accurate view of its risk. Lenders and mortgage-backed securities (MBS) investors need a comprehensive view of the risks to their portfolios. This is where RMS stochastic models can help, as they offer a long-term view of the underlying risk, addressing issues such as the questions that follow.

What is the level of risk at a location? Insurers are well versed in using natural hazard risk scores (a rating that reflects the severity of a risk) for individual locations. SiteIQTM is an application from RMS that extracts data from RMS risk models and extensive exposure datasets to provide location-specific risk scores. This enables mortgage providers and investors in mortgage debt to combine natural hazard risk scores with their internal risk scoring system and compare risk scores across assets in their portfolio, to help make informed investment and loan underwriting decisions. For example, RMS is partnering with Trepp, a leading mortgage data provider, to produce risk scores for earthquake, flood, hurricane, wildfire, and other key climate perils. These risk scores will help Trepp’s clients assess physical risks – a key component of Environmental, Social and Governance (ESG) scores – for commercial real estate investments.

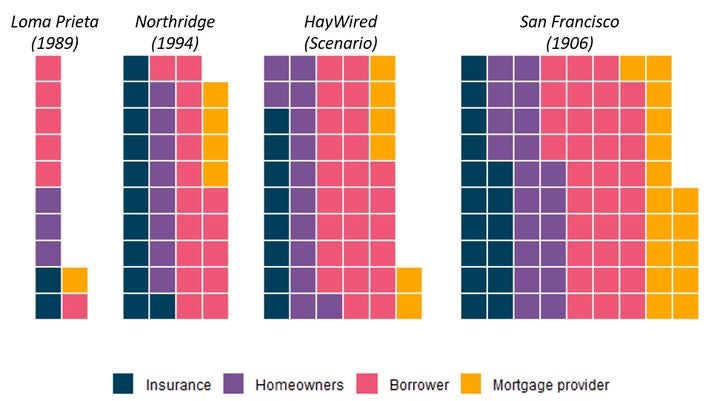

How much would I lose under a given event scenario? Looking at the risk across an entire portfolio, mortgage providers can identify risk hot spots and analyze contributions to total risk by geographies, investment types, business lines, etc. RMS applies the latest scientific research to convert the hazard characteristics of an event into a loss to different stakeholders. Modeling results for re-creations of the Loma Prieta (1989), Northridge (1994), and San Francisco (1906) Earthquakes and the hypothetical HayWired earthquakes scenarios are provided in Figure 2.

Figure 2: Stakeholder share of the total scenario loss to the residential market. (Methodology: exposure and insurance penetration as of 2018, assumes 71 percent of mortgaged homes and 65 percent loan-to-value ratio. Data: RMS Economic Exposure Database, 2018; RMS Industry Exposure Database, 2018.)

How likely is my portfolio to suffer a loss due to natural catastrophe – and how large could it be? RMS stochastic models combine thousands of realistic scenarios and their associated probability of occurrence. The result is a long-term, realistic view of mortgage default losses that can uncover previously unidentified sources of risk and inform suitable strategies to manage and transfer them.

RMS data and analytics support mortgage investors at each step of their risk management strategy. Lenders can use risk scores to guide their loan underwriting and define earthquake insurance requirements. Probabilistic models provide a better understanding of the risk to an investment portfolio and underpin risk transfer strategies. RMS recently enabled a mortgage credit investment company to quantify their risk from earthquake-driven mortgage default to their U.S. portfolio. The client was able to compare the levels of risk to their risk tolerances and ultimately transfer some of their risk through innovative risk transfer product: Sierra Ltd.

Mortgage default assumptions can be implemented in RMS probabilistic models to provide lenders and mortgage investment professionals with a view of their default risk from catastrophic events. Our models cover major risks such as flood or earthquake across markets from North America to Asia. We can provide mortgage default risk information whether it is for broader market-share analytics or detailed studies that account for location-specific details of each loan within a portfolio. Further information about our solutions for financial services can be found on the RMS website. Please contact us at sales@rms.com to find out more.

Senior Consulting Analyst, Capital and Resilience Solutions, RMS

Arnaud is a senior analyst in the RMS Capital and Resilience Solutions group. His work focuses on working with a range of private and public sector clients across the globe, to help them quantify their exposure to catastrophe risk, assess resulting business impacts, and inform effective risk mitigation and transfer measures.

His responsibilities include leading the analytics for bespoke probabilistic hazard and loss assessments for different types of physical assets and financial structure, as well as the design, evaluation and optimization of custom risk transfer products. In addition, Arnaud works on the execution of catastrophe bond risk analyses, re-modeling and market commentary.

Arnaud holds a master's degree in Risk, Disaster and Resilience from University College London.