The Moody's RMS Blog

Get expert perspectives as our team weighs in on the latest events, topics, and insights to help you demystify risk and deepen resilience.

Snaefellsnes Peninsula, Iceland

Tag: Perils

Filter by:

Lessons Learned from Winter Windstorm Season in ...

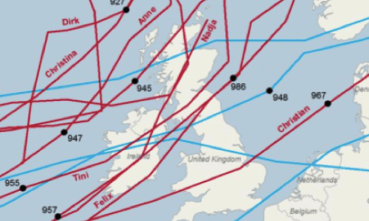

The 2013–2014 winter windstorm season in Europe will be remembered for being particularly active, bringing persistent unsettled weather to the…

One Year Later: What We Learned from the Moore T...

This week marks the one-year anniversary of the severe weather outbreak that brought high winds, hail, and tornadoes to half of all U.S.…

Uncertainty and Unknown Unknowns

At today’s inaugural ‘Catastrophe Risk Management & Modelling Australasia 2013’ in Sydney, the focus is on model uncertainty, unknown…