For everyone working in risk management, there is an implicit understanding about the wider mission underlining our work: to help create a more resilient world. But we are trying to build resilience in an era when assessing the physical impacts of climate change has become more challenging. With increasing board-level attention, stakeholder scrutiny, and regulatory pressure, businesses everywhere are struggling to understand the impacts of climate change and make better decisions.

Climate Change Is Personal

Climate change is personal to all of us. I live in Northern California, and the hotter, drier environment has aided three of the most destructive wildfire seasons in the last four years. I’m already thinking about the next wildfire season and getting stuck in my home for days due to smoky skies. Scenarios like this – where climate change is affecting everyday life – are playing out all over the world.

Just six months ago, I made one of the biggest career moves of my life. I decided to blend my background in data and analytics with my desire to fight climate change – and I joined RMS®. RMS has been modeling natural catastrophe risk for more than 30 years and leading research into the impact of climate change on losses since 2007. Since I joined, I have become increasingly optimistic about the opportunities to apply technology solutions to solve these big, global challenges.

Fighting on Two Fronts

The insuranceindustry is fighting on two fronts: managing rapidly changing risk profiles today while also adapting long-term business strategies for tomorrow. In the U.S. alone, (re)insurers are challenged by weather-related economic losses of US$500 billion over the last five years. And another US$14.2 trillion more in assets are at risk due to coastal flooding, just one of the many perils impacted by climate change.

Regulatorsalso want answers. The U.K. Prudential Regulatory Authority is running a major climate change stress test in June. And for the first time in its history, the U.S. Federal Reserve mentioned climate change in its Financial Stability Report. There are similar initiatives at the U.S. Treasury and the Securities and Exchange Commission.

But it’s not just insurers and regulators; the entire financial services community faces the same issues. How will climate change impact asset prices, loan books, portfolios – now and into the distant future? The risk is systemic and with financial instruments more connected than ever, risk is being priced into everything.

The private sector is not far behind. RMS has worked with industry leaders such as QBE Insurance Group in Australia which is already addressing climate change in their annual report. Banks, and other financial firms are doing the same. And once climate change risk is disclosed on balance sheets, you can expect investment decisions to follow.

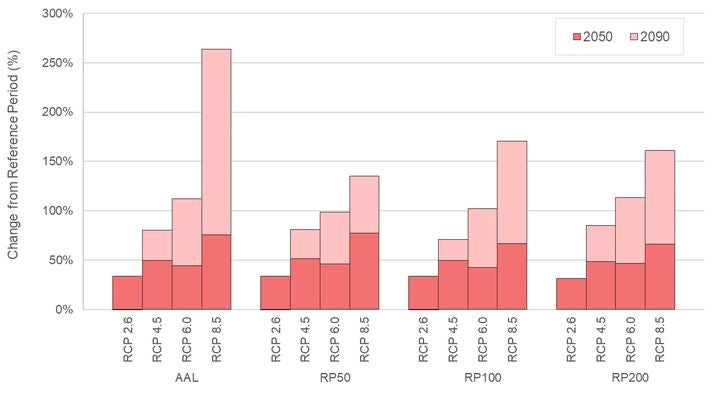

Without Mitigation, by 2050, European Flood Losses Could Rise by up to 75%

Our recent work with regulator EIOPA on European inland flood shows the impact that different emissions and carbon mitigation scenarios could make on flood losses. Using RMS Europe Inland Flood HD Models in combination with preliminary results from our ongoing research on climate change, we found that if a 2050 climate scenario was applied, estimated average annual losses (AAL) for present-day exposure from flood for the 14 modeled countries in Europe would increase by up to 75 percent.

Tail risk metrics, and therefore capital requirements, could change even more dramatically. These estimates are based on Intergovernmental Panel on Climate Change (IPCC) Representative Concentration Pathways (RCP) RCP2.6 and RCP4.5 - if no mitigation strategies are adopted (see Figure 1). RCP scenarios help us understand how greenhouse gas (GHG) concentrations in the atmosphere may evolve in the future as a result of different intervention levels.

Figure 1: Modeled climate change impact on annual average (AAL) and annual aggregate insured losses for different return periods (RP) under different IPCC RCP emissions scenarios in 2050 and 2090 (percentage change from reference view)

The Case for Resilience

Being true to the industry’s mission – to move forward with resilience – there is an urgent need to understand the risk drivers of climate change. It is complex, but this is not an industry that shies away from complexity. Look how far we have come in understanding the risks and the impacts of everything from hurricanes and earthquakes, terrorism and cyber.

Climate change is our next big challenge. The analytics we can produce today will provide insights into how physical climate change risk will impact communities, and to help us prepare for those impacts.

I’m confident that we can make the needed changes together. But we must have the right tools to do so.

Introducing New RMS Climate Change Models

Translating the impact of future climate scenarios into tangible metrics such as insured and economic loss costs, disruption statistics, business interruption, and the cost of other associated impacts has always been difficult.

As a pioneer and leader in catastrophe modeling, time and again, RMS has consistently brought technology, science, and data together to help organizations manage risk, and to outperform. Consistent with our vision to make every risk known, we’ve been working on climate change research, regulatory, and customer projects since 2008.

Today, we are proud to announce a new chapter in our climate change journey with the launch of RMS Climate Change Models.

The new Climate Change Models augment our proprietary impact modeling framework with the best climate science consensus, including the IPCC. The new models will be available this summer with the North Atlantic Hurricane Models, Europe Inland Flood Models and Europe Windstorm Models, with further models and geographies to follow.

Each time horizon – from today through to the end of the century – includes what-if scenarios to capture a range of possible future atmospheric GHG concentrations.

RMS Climate Change Models help firms address:

Shareholder communications: Corporate boards are demanding greater accountability, transparency, and action in response to climate change. The C-suite needs to provide comprehensive and credible responses.

Risk-based pricing: Across many parts of the financial services industry, including asset valuations and insurance.

Risk optimization: The growing risk from climate change is forcing the industry to reevaluate its near- and long-term approaches to risk selection, risk pricing, and portfolio management.

New regulatory requirements: Financial services firms face new sets of regulation focused on the resiliency of the current business models and the financial risks posed by climate change.

Summary

The risk management industry is truly on the front lines of climate change. The mission that drives me and, my colleagues - and I think the whole industry, is building a more resilient world. We all want to cross the chasm and move full speed ahead on the biggest issue of our lifetime.

As Bill Gates states in his new book How to Avoid a Climate Disaster, this is a crucial moment – what we need now is a plan that turns the strong momentum on many fronts into practical steps to achieve big goals.

With the launch of RMS Climate Change Models and our partnership approach, we want to help our clients to do just that.

For more information, click here to check out the RMS climate change page.

Arik leads product marketing for RMS, where he helps customers on their journey to greater resilience. Arik is a frequent speaker on becoming a digital enterprise, Internet of Things (IoT) and analytics, and has a passion for helping customers deliver the right data to the right place at the right time.

Previously, Arik led product marketing for Pentaho - a data integration startup, Hitachi Vantara, and Moody’s Analytics.

He holds a bachelor's degree in Information Management from Syracuse University, and an MBA from Indiana University’s Kelley School of Business.