In the days leading up to landfall for a major hurricane such as Irma, you will find RMS employees and clients glued to their devices. We are all reading weather blogs, studying RMS HWind snapshots, monitoring Twitter, and sharing each other’s projections and observations on LinkedIn. This is all to get the latest view on a dynamic system – what is the maximum sustained wind? What is the Rmax? Central pressure? What is the integrated kinetic energy?

In such a dynamic situation, it is important to also consider what is static: the concentration of exposure within the hurricane uncertainty cone. In the most general sense, the industry insured loss for such an event is a function of the physical characteristics of the storm and the scale of exposure that is impacted. As has been stated elsewhere on the RMS blog, loss scenarios will vary significantly depending on the concentrations of exposure underlying the event footprint. For hurricanes, a few miles can be the difference between a footnote on a quarterly earnings statement or front page headlines. This was the story last year with Hurricane Matthew after it “wobbled” to the east and spared much of southeast Florida.

While still days from a possible landfall, the “spaghetti” plots for Irma show that there is uncertainty on where it will track. With this in mind, it is important to analyze exposure across these areas and quantify how exposure concentrations — just as much as storm intensity — influence the range of losses that models provide. This analysis can be performed within Exposure Manager in the days leading up to landfall. During and following an event, RMS provides Risk Analysis Profiles and post-event footprints which can then be loaded directly into Exposure Manager, a recent example being flood footprints for Hurricane Harvey.

In addition to seeing just the Total Insured Value (TIV) within those accumulations, a unique capability of Exposure Manager is to calculate exposed limit via the RMS financial model, which means users can see exactly what is on the line for their business as opposed to estimating this from TIV or market share statistics. This is particularly important when assessing excess-NFIP coverage or for commercial and specialty business, which often have higher attachment points and complex policy terms and special conditions.

Consider two possible scenarios with respect to Irma’s track:

Irma makes a turn north along the Atlantic coast and makes a direct landfall on Miami

Irma tracks west through the Florida Keys (Monroe County), but avoids more populated counties (such as Lee) to the north as it continues into the Gulf

Of course, a third scenario is that Irma does not make landfall.

According to analyses in Exposure Manager on the RMS 2017 Industry Exposure Database…

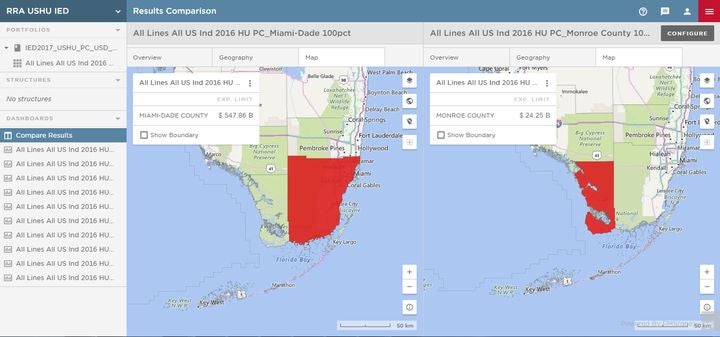

Miami-Dade County has more than 20x the exposed limit relative to Monroe County

If you just consider the exposed limit in Miami-Dade within postal codes that are less than a mile from the coast, it has 7x the exposed limit relative to all postal codes in Monroe

In fact, there is one postal code in Miami-Dade County that has nearly the same amount of exposed limit as all of Monroe County! (Beware of postal code 33131)

Considering the difference in exposure between Miami-Dade and Monroe counties is more than an order of magnitude, it is easy to see how loss distributions such as this one can show a wide spread of industry loss probabilities given different forecast tracks.

Figure 1: Comparison between industry exposure in Miami-Dade vs. Monroe counties

This analysis is just considering the RMS Industry Exposure Database. Individual client portfolios can vary significantly in geographic distribution and policy structures. Using Exposure Manager, our clients are finding the pockets of exposure ahead of time in their own books that drive uncertainty in their loss projections.

Share:

You May Also Like

Rhett Austell

Director Client Solutions team RMS

Rhett is a director within the Client Solutions team at RMS where he consults with clients on implementing RMS models, data, and technology solutions into their businesses. During his ten years at RMS, he has worked closely with reinsurers, primaries, reinsurance brokers and ILS managers. He is a graduate of Penn State University with degrees in Economics and International Politics.