NFIP Losses from Harvey Estimated to Reach US$7-10 Billion

Pete DaileySeptember 01, 2017

On Wednesday, RMS reported that, based on our modeling, the overall combined wind, surge, and inland flood losses from Hurricane Harvey will be US$70-90 billion. My colleague, Daniel Stander, had previously also pointed out that “economic losses from Harvey will outstrip insured losses by a considerable margin.” That’s because the uptake of private flood insurance in the U.S. is very limited.

RMS continues to refine its estimate of the insured losses from Harvey. In the meantime, I think it’s worth looking in more detail at the potential exposure of the National Flood Insurance Program (NFIP) to this major hurricane.

Last Monday, Daniel wrote that it was likely that “Harvey will produce at least US$4 billion in flood claims, triggering the NFIP reinsurance program.” With NFIP up next month for reauthorization and reform, this is an important point — and not just for the 25 reinsurers underwriting over US$1 billion of NFIP’s claims.

How large, then, will the bill be that arrives at the U.S. Treasury Department via the NFIP?

In 2015, following a request under a Freedom of Information Act (FOIA), RMS obtained some data about NFIP’s exposures. This data was received in an anonymized form in order to protect the privacy of personal information. From this dataset, RMS constructed a gridded representation of the NFIP portfolio of policies.

Using this exposure, RMS estimates that the gross losses accrued in the NFIP will be between US$7-10 billion. About 40 percent of those claims are expected to come from Harris County alone.

Given the extent and duration of inundation, it is not unreasonable to assume an average paid loss of US$65,000. For context, this figure is consistent with the mean claim NFIP paid out for Superstorm Sandy.

Because of the anonymized nature of the exposure data RMS received under FOIA, we do not know exactly how many of the NFIP’s policies are likely to have been impacted by Harvey. However, taking our US$7-10 billion modeled loss dividing by the assumption of a US$65,000 mean average claim, the program will receive approximately 100,000 to 150,000 claims from this catastrophic event.

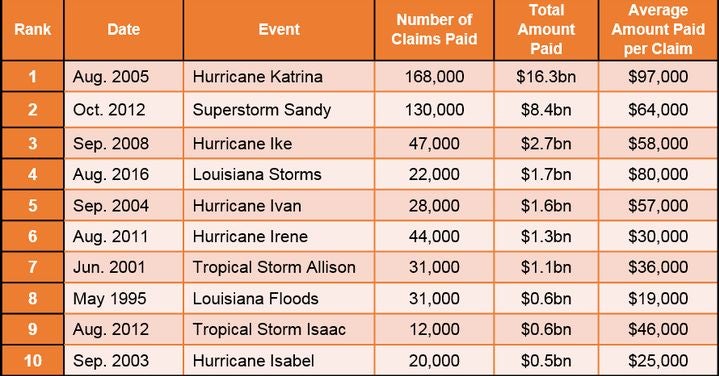

To put this into context, let’s consider the history of events which have materially impacted the NFIP’s profitability. The figure below ranks the flood events which have caused the ten most significant payouts by the NFIP. Assuming our estimates are reasonably accurate, it seems clear that Harvey will be a top three loss event for the program. While it appears unlikely the NFIP’s losses in Harvey will be as great as those sustained as a result of Hurricane Katrina (2005), there is no reason to assume that they will not be as large if not larger than those from Superstorm Sandy (2012).

Ten Most Significant Flood Events to the National Flood Insurance Program – Ranked by Total Value of Claims Paid1

1. Includes events from 1978 to November 30, 2016, as of January 18, 2017. Includes all events where NFIP paid at least 1,500 claims. Stated in dollars when occurred.

Source: U.S. Department of Homeland Security, Federal Emergency Management Agency; U.S. Department of Commerce, National Oceanic and Atmospheric Administration, National Hurricane Center.

During the first days of Hurricane Harvey, Daniel Stander and Ben Brookes drew attention in RMS’ live Harvey updates to the NFIP’s reinsurance program. This program provides the U.S. taxpayer with a little over US$1 billion of protection. That US$1 billion only kicks in once the NFIP has paid US$4 billion in claims. The program then sees FEMA sharing the cost of claims with the private market up until it has paid out US$8 billion.

Based on RMS estimates that the gross insurance losses accrued in the NFIP will be between US$7-10 billion, it’s quite obvious that the reinsurance program is going to be activated. It seems NFIP’s efforts to diversify risk into the global risk transfer market are starting to pay off.

Share:

You May Also Like

September 16, 2020

Atlantic Hurricane in 2020: Are We in Store for Another Record-Breaking Year?

Dailey is VP, Model Development at RMS and has served the CAT modeling industry for 20 years. He is responsible for delivering Global Event Response products to RMS clients before (forecast products), during (real-time response) and following (event reconstruction) all major natural catastrophes worldwide.

Pete manages teams in London, U.K. and Florida, dedicated to providing 24/7/365 support as events unfold. Pete is also actively involved in formulating RMS’ strategy for developing climate change risk analytics and solutions.Pete has presented and published on various topics important to risk management including tropical cyclones, severe convective storms, coastal and inland floods, and the relationship of our changing climate to the dynamic landscape of insured and economic risk.

Pete holds degrees in Econometrics and Systems Engineering from Penn and a M.S. and Ph.D. in Atmospheric Science from the University of California, Los Angeles.