Flood Re has been tasked with creating a risk-reflective, affordable U.K. flood insurance market by 2039. Moving forward, data resolution that supports critical investment decisions will be key

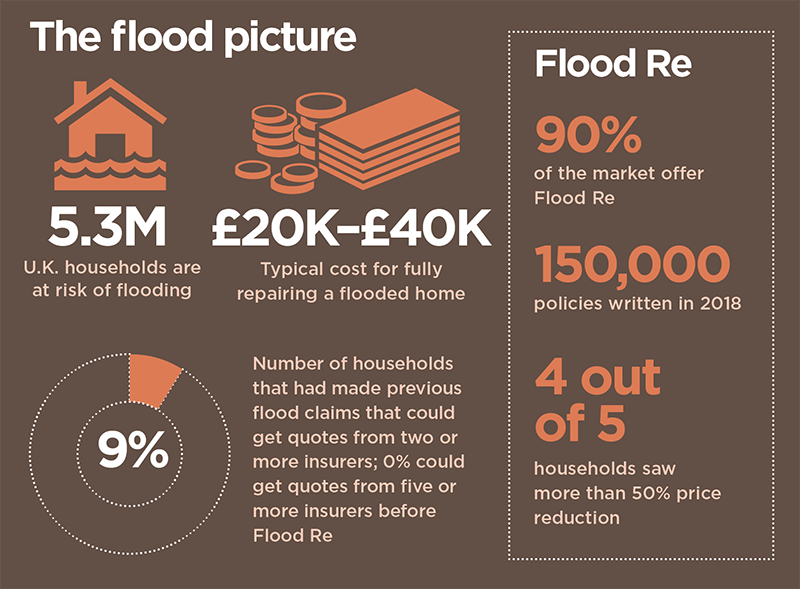

Millions of properties in the U.K. are exposed to some form of flood risk. While exposure levels vary massively across the country, coastal, fluvial and pluvial floods have the potential to impact most locations across the U.K. Recent flood events have dramatically demonstrated this with properties in perceived low-risk areas being nevertheless severely affected.

Before the launch of Flood Re, securing affordable household cover in high-risk areas had become more challenging — and for those impacted by flooding, almost impossible. To address this problem, Flood Re — a joint U.K. Government and insurance-industry initiative — was set up in April 2016 to help ensure available, affordable cover for exposed properties.

The reinsurance scheme’s immediate aim was to establish a system whereby insurers could offer competitive premiums and lower excesses to highly exposed households. To date it has achieved considerable success on this front.

Of the 350,000 properties deemed at high risk, over 150,000 policies have been ceded to Flood Re. Over 60 insurance brands

representing 90 percent of the U.K. home insurance market are able to cede to the scheme. Premiums for households with prior flood claims fell by more than 50 percent in most instances, and a per-claim excess of £250 per claim (as opposed to thousands of pounds) was set.

While there is still work to be done, Flood Re is now an effective, albeit temporary, barrier to flood risk becoming uninsurable in high-risk parts of the U.K. However, in some respects, this success could be considered low-hanging fruit.

A Temporary Solution

Flood Re is intended as a temporary solution, granted with a considerable lifespan. By 2039, when the initiative terminates, it must leave behind a flood insurance market based on risk-reflective pricing that is affordable to most households.

To achieve this market nirvana, it is also tasked with working to manage flood risks. According to Gary McInally, chief actuary at Flood Re, the scheme must act as a catalyst for this process.

“Flood Re has a very clear remit for the longer term,” he explains. “That is to reduce the risk of flooding over time, by helping reduce the frequency with which properties flood and the impact of flooding when it does occur. Properties ought to be presenting a level of risk that is insurable in the future. It is not about removing the risk, but rather promoting the transformation of previously uninsurable properties into insurable properties for the future.”

To facilitate this transition to improved property-level resilience, Flood Re will need to adopt a multifaceted approach promoting research and development, consumer education and changes to market practices to recognize the benefit. Firstly, it must assess the potential to reduce exposure levels through implementing a range of resistance (the ability to prevent flooding) and resilience (the ability to recover from flooding) measures at the property level. Second, it must promote options for how the resulting risk reduction can be reflected in reduced flood cover prices and availability requiring less support from Flood Re.

According to Andy Bord, CEO of Flood Re: “There is currently almost no link between the action of individuals in protecting their properties against floods and the insurance premium which they are charged by insurers. In principle, establishing such a positive link is an attractive approach, as it would provide a direct incentive for households to invest in property-level protection.

“Flood Re is building a sound evidence base by working with academics and others to quantify the benefits of such mitigation measures. We are also investigating ways the scheme can recognize the adoption of resilience measures by householders and ways we can practically support a ‘build-back-better’ approach by insurers.”

Modeling Flood Resilience

Multiple studies and reports have been conducted in recent years into how to reduce flood exposure levels in the U.K. However, an extensive review commissioned by Flood Re spanning over 2,000 studies and reports found that while helping to clarify potential appropriate measures, there is a clear lack of data on the suitability of any of these measures to support the needs of the insurance market.

A 2014 report produced for the U.K. Environment Agency identified a series of possible packages of resistance and resilience measures. The study was based on the agency’s Long-Term Investment Scenario (LTIS) model and assessed the potential benefit of the various packages to U.K. properties at risk of flooding.

The 2014 study is currently being updated by the Environment Agency, with the new study examining specific subsets based on the levels of benefit delivered.

“It is not about removing the risk, but rather promoting the transformation of previously uninsurable properties into insurable properties”

Gary McInally

Flood Re

Packages considered will encompass resistance and resilience measures spanning both active and passive components. These include: waterproof external walls, flood-resistant doors, sump pumps and concrete flooring. The effectiveness of each is being assessed at various levels of flood severity to generate depth damage curves.

While the data generated will have a foundational role in helping support outcomes around flood-related investments, it is imperative that the findings of the study undergo rigorous testing, as McInally explains. “We want to promote the use of the best-available data when making decisions,” he says. “That’s why it was important to independently verify the findings of the Environment Agency study. If the findings differ from studies conducted by the insurance industry, then we should work together to understand why.”

To assess the results of key elements of the study, Flood Re called upon the flood modeling capabilities of RMS, and its Europe Inland Flood High-Definition (HD) Models, which provide the most comprehensive and granular view of flood risk currently available in Europe, covering 15 countries including the U.K. The models enable the assessment of flood risk and the uncertainties associated with that risk right down to the individual property and coverage level. In addition, it provides a much longer simulation timeline, capitalizing on advances in computational power through Cloud-based computing to span 50,000 years of possible flood events across Europe, generating over 200,000 possible flood scenarios for the U.K. alone.

The model also enables a much more accurate and transparent means of assessing the impact of permanent and temporary flood defenses and their role to protect against both fluvial and pluvial flood events.

Putting Data to the Test

“The recent advances in HD modeling have provided greater transparency and so allow us to better understand the behavior of the model in more detail than was possible previously,” McInally believes. “That is enabling us to pose much more refined questions that previously we could not address.”

While the Environment Agency study provided significant data insights, the LTIS model does not incorporate the capability to model pluvial and fluvial flooding at the individual property level, he explains.

RMS used its U.K. Flood HD model to conduct the same analysis recently carried out by the Environment Agency, benefiting from its comprehensive set of flood events together with the vulnerability, uncertainty and loss modeling framework. This meant that RMS could model the vulnerability of each resistance/resilience package for a particular building at a much more granular level.

RMS took the same vulnerability data used by the Environment Agency, which is relatively similar to the one used within the model, and ran this through the flood model, to assess the impact of each of the resistance and resilience packages against a vulnerability baseline to establish their overall effectiveness. The results revealed a significant difference between the model numbers generated by the LTIS model and those produced by the RMS Europe Inland Flood HD Models.

Since hazard data used by the Environment Agency did not include pluvial flood risk, combined with general lower resolution layers than used in the RMS model, the LTIS study presented an overconcentration and hence overestimation of flood depths at the property level. As a result, the perceived benefits of the various resilience and resistance measures were underestimated — the potential benefits attributed to each package in some instances were almost double those of the original study.

The findings can show how using a particular package across a subset of about 500,000 households in certain specific locations, could achieve a potential reduction in annual average losses from flood events of up to 40 percent at a country level. This could help Flood Re understand how to allocate resources to generate the greatest potential and achieve the most significant benefit.

A Return on Investment?

There is still much work to be done to establish an evidence base for the specific value of property-level resilience and resistance measures of sufficient granularity to better inform flood-related investment decisions.

“The initial indications from the ongoing Flood Re cost-benefit analysis work are that resistance measures, because they are cheaper to implement, will prove a more cost-effective approach across a wider group of properties in flood-exposed areas,” McInally indicates. “However, in a post-repair scenario, the cost-benefit results for resilience measures are also favorable.”

However, he is wary about making any definitive statements at this early stage based on the research to date.

“Flood by its very nature includes significant potential ‘hit-and-miss factors’,” he points out. “You could, for example, make cities such as Hull or Carlisle highly flood resistant and resilient, and yet neither location might experience a major flood event in the next 30 years while the Lake District and West Midlands might experience multiple floods. So the actual impact on reducing the cost of flooding from any program of investment will, in practice, be very different from a simple modeled long-term average benefit. Insurance industry modeling approaches used by Flood Re, which includes the use of the RMS Europe Inland Flood HD Models, could help improve understanding of the range of investment benefit that might actually be achieved in practice.”

{kind=link}