Almost three months ago we passed a remarkable record in catastrophe loss.

And yet no one seems to want to celebrate it.

No banner headlines in the newspapers. No speeches at the Monte Carlo Reinsurance Rendezvous.

The first half of 2019 generated the lowest catastrophe insurance loss for more than a decade. The estimates come in at: US$15 billion (Munich Re), US$19 billion (Sigma), or US$20 billion (Aon). In straight dollar terms, independent of any adjustment for inflation or exposure, this is lower than any year since 2006.

The climate may be growing warmer, sea levels rising, the stress accumulating on hundreds of plate boundary faults, magma rising beneath volcanoes, forests turning into desiccated fuel for fires, dams eroding, more and more buildings being constructed in flood plains – but as measured by actual catastrophes the world has been becalmed. Extremely Severe Cyclone Fani, a Cat 4 storm during late April in the Bay of Bengal, weakened to a Cat 1 soon after landfall. The H1 2019 Cats have turned out to be Kittens.

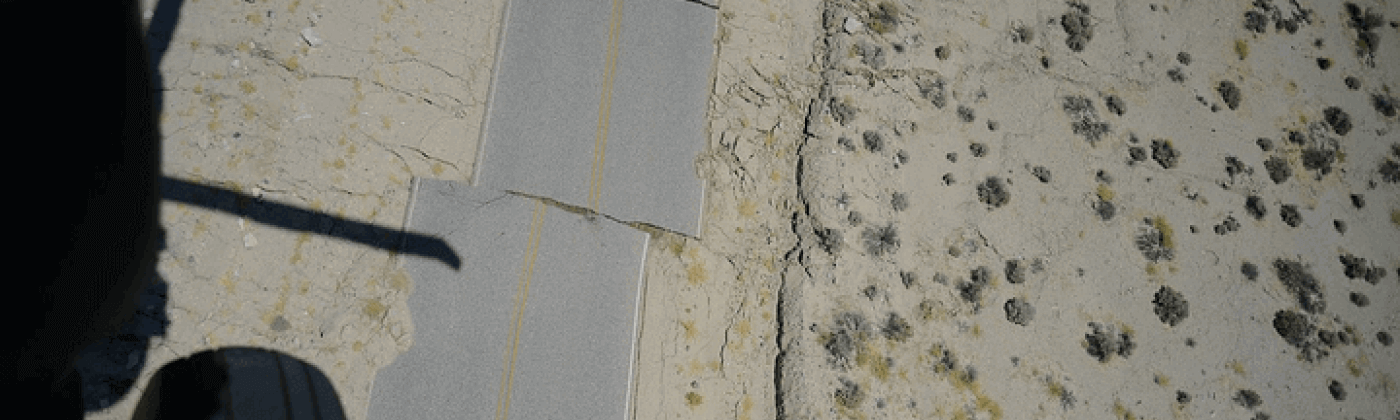

California Geological Survey and USGS geologists and geophysicists with National Guard and U.S. Navy personnel view road damage from 3-5 feet of right-lateral motion near the expected maximum slip locality along the primary tectonic rupture associated with the Mw7.1 Ridgecrest event. Image credit: Wikimedia/USGS

Into the second half of the year, the Mw7.1 Ridgecrest earthquake in California during July occurred far from any concentration of exposure. And now more than half way through the North Atlantic hurricane season, even with Dorian’s catastrophic impact on the northern Bahamas and Typhoon Faxai’s recent assault on Tokyo Bay, this still leaves the year on a low insured-loss trajectory. (The annual average global insured catastrophe loss from 2008-2018 was US$63 billion.)

What do we learn from the low level of losses in 2019? That the rising costs of catastrophes have been overblown? No, we learn the confusion of living with extreme volatility. After the summers of 2005 or 2017, it was hard to avoid concluding that Armageddon had arrived. When we are in the middle of the doldrums, like the decade when there was no Cat 3 or greater hurricane making U.S. landfall, we had to avoid the illusion that catastrophes have gone away.

The insurance-linked securities (ILS) market, with only US$1.7 billion of new non-life capacity issued in Q2 2019, is two thirds down from the average issuance of Q2 2017 (US$6.2 billion) and Q2 2018 (US$4.0 billion). It seems that ILS issuers and investors, challenged by trapped collateral, have succumbed to the “extrapolation of recent experience” rather than learnt to live with the volatility. Meanwhile the reinsurers are busy doing what they do best – writing new business when the market has hardened after the losses. We should appreciate the lulls, let reinsurers build up their reserves, and let the cat modelers focus on developing new models, for the catastrophes will return.

Robert Muir-Wood works to enhance approaches to natural catastrophe modeling, identify models for new areas of risk, and explore expanded applications for catastrophe modeling. Robert has more than 25 years of experience developing probabilistic catastrophe models. He was lead author for the 2007 IPCC Fourth Assessment Report and 2011 IPCC Special Report on Extremes, and is Chair of the OECD panel on the Financial Consequences of Large Scale Catastrophes.

He is the author of seven books, most recently: ‘The Cure for Catastrophe: How we can Stop Manufacturing Natural Disasters’. He has also written numerous research papers and articles in scientific and industry publications as well as frequent blogs. He holds a degree in natural sciences and a PhD both from Cambridge University and is a Visiting Professor at the Institute for Risk and Disaster Reduction at University College London.

{kind=link}