The Role of Catastrophe Risk Finance in Developing Nations

Daniel StanderJuly 24, 2017

We all know that prevention is better than cure. Trouble is, sometimes you catch a cold. And if you’re already vulnerable, a relatively small infection presents a big risk – especially if you don’t have timely access to sufficient amounts of the necessary medicines.

Despite the best will in the world, nobody can stop the ground from shaking or the wind from blowing. Nobody can say that the worst-case scenario will never happen.

So, when Mother Nature strikes a vulnerable, low-income country, how bad will the ensuing humanitarian crisis likely be? What will it take financially to recover and rebuild? And is there a role for insurance along with donor aid?

Tackling the Challenges of Our Generation

The U.K. government Department for International Development (DfID) posed these questions to us, commissioning RMS to conduct the first-ever comprehensive assessment of disaster losses and the corresponding financial assistance. The overarching objective was to quantify the likely potential for insurance schemes to reduce the financial burden of disaster losses on the world’s poorest.

DfID had long sensed that insurance might have an important role to play in tackling the global challenges of our time: to end extreme poverty and build a safer, healthier, and more prosperous world. To this end, the U.K. Prime Minister Theresa May announced at the G20 Summit in Hamburg earlier this month the creation of a new London Center for Global Disaster Protection. Using world-leading expertise, the center will help developing countries both strengthen disaster planning and deploy rapid, reliable finance in emergencies.

At the International Insurance Society’s Global Insurance Forum held in London last week, international development minister, The Rt Hon Lord Bates, said £30 million (US$39 million) had been pledged by the U.K. government for the center. Germany will contribute a further €20 million ($23 million) to a linked trust fund. With administrative support from the World Bank, the center will open in early 2018. The goal – to tailor country-specific disaster risk financing mechanisms to assist the world’s most vulnerable communities.

The Rt Hon Lord Bates addresses the Global Insurance Forum in London on July 20, 2017. Picture Credit: Russell Harper Photography

“Global humanitarian assistance is at record levels but it still cannot meet growing demand,” said Lord Bates in his forum address. “International assistance absorbs only a portion of this – eight percent. The rest is borne by people, businesses, and governments.”

“The insurance industry is a global risk pool – with trillions in capital that can absorb the costs of big, rare shocks like natural disasters… Our job as development partners is to support countries to design and use the instruments that are right for them in managing their own risks.”

One of the roles of the center will be to provide neutral advice – supporting countries in making decisions about which financial instruments are right for them.

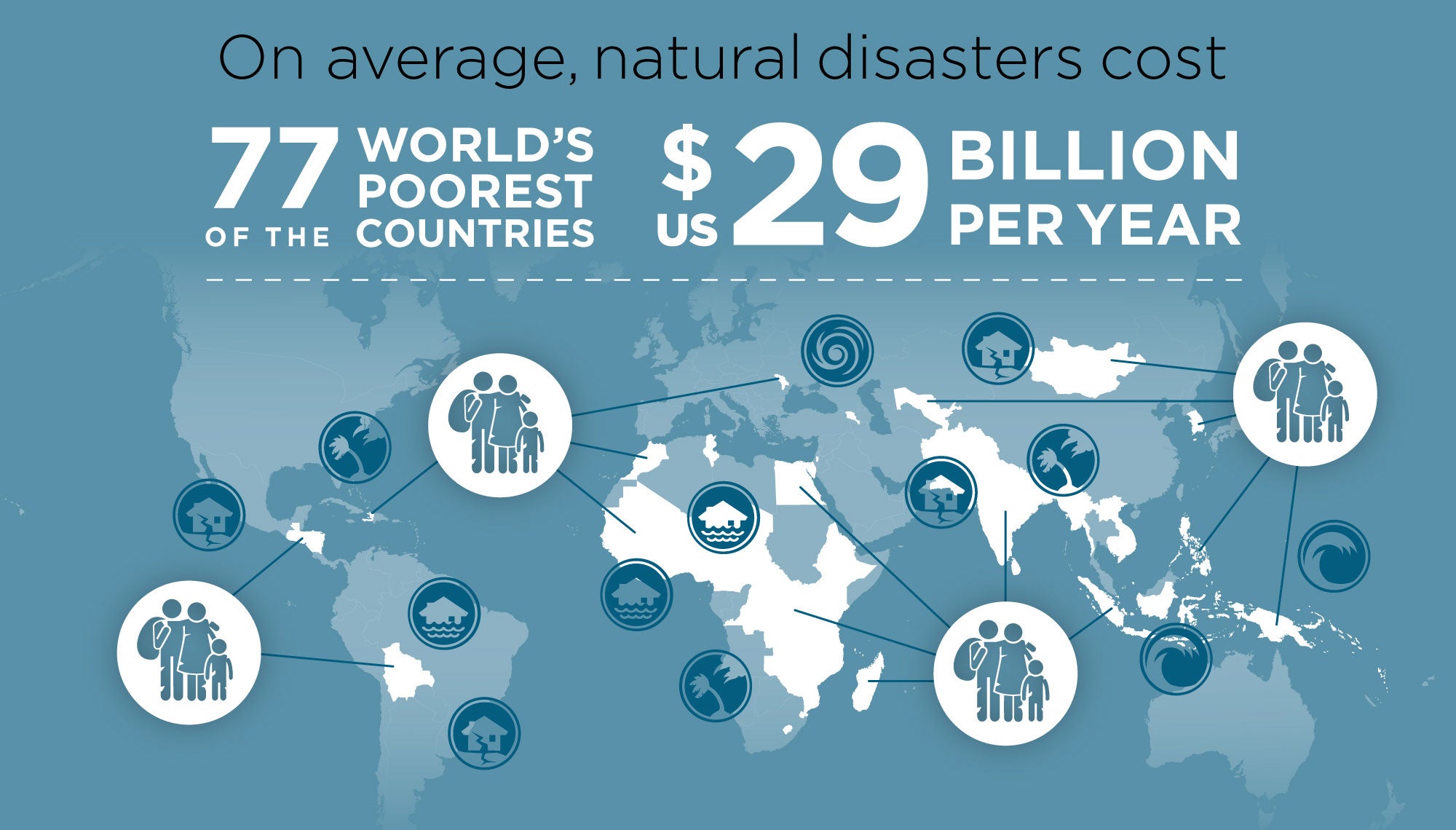

Of the $47 billion in economic losses, RMS research shows that $6 billion (12 percent) are met by humanitarian aid. Only $2 billion (5 percent) are covered by insurance. This means that a difference of $39 billion must be shouldered by the people directly affected, or their governments, which are among the world’s poorest. What can be done to meet this $39 billion shortfall?

Annual aid expenditure for low and low-middle income countries in response to natural disasters for the period 2000 to 2015 averaged $2.2 billion. Much of this aid came from global appeals and was focused on 2004 Indian Ocean tsunami ($15 billion raised) and the 2010 Haiti earthquake ($8 billion).

Disaster relief aid by its very nature is reactive, pledged during and after the event, and the amount generated is unpredictable. Pledges made can also be slow to materialize, with examples of payments taking months or even years.

The role of insurers currently focuses mainly on the reconstruction of private assets. Most of the cover is provided via traditional indemnity products. Some sovereign states have put parametric schemes in place, which, if well-designed, can provide much needed help with post-event reconstruction. The report examined the potential for expanding the use of insurance not just to rebuild public and private assets, but also to deliver emergency response and social protection.

Building Strong Insurance Markets

There are of course barriers to stimulating the growth of risk transfer in the world’s poorest countries. Typically, there is no mature domestic insurance market to leverage. Nor are there sufficient government resources to fund sovereign-backed insurance schemes. Without a concerted effort, the role of risk transfer in disaster recovery would largely remain at current levels.

Positive steps are required for risk transfer to expand. The governments of developing countries need to embrace the very idea of insurance as an effective way of protecting assets and livelihoods at risk. They need to actively support the growth of domestic insurance markets, encouraging regulation that enables both the financial stability of insurers, and increases consumer confidence that claims will be paid.

Increasing insurance participation will ultimately reduce the dependence on humanitarian aid, reassure private investors and help people rebuild their lives. If linked to ex-ante disaster risk reduction measures and predicated on realistic and actionable recovery plans, it could drive the kind of resilience-building investments which stimulate greater financial independence.

DfID hopes that the London center will provide £2 billion in risk financing. This “unique opportunity” is just the beginning, but it’s an important step. If done well, it could ensure that the high costs of disasters aren’t borne by the world’s poorest, liberate people, businesses and governments from cycles of poverty, and boost economic development where it’s needed most.

Share:

You May Also Like

March 17, 2019

Exposure Trending

A postcard from Manila…

Situation: rapid, uncontrolled urbanization and limited enforcement of building codes.

Complication: unwieldy administrative procedures, limited funding, a lack of technical expertise and #NIMTOO.

Result: an alarming rise of building vulnerability in hazard-prone communities putting millions of low-income people at extreme risk.

While many local government officials recognize this problem, progress is painfully slow. Housing vulnerability continues to rise. What to do?

The Issue of Our Age?

According to my favorite bricklayer, Dr. Elizabeth Hausler, housing vulnerability is the defining issue of our age. By 2030, three billion people will live in substandard homes. That’s one third of the world’s population.

Just ask Santiago Uribe Rocha, the first Chief Resilience Officer employed in a non-OECD country. In Colombia over the past 20 years, more than ten million people have moved to major cities like his, Medellín. The lack of affordable housing has led many of these low-income families to settle on the outskirts, often building haphazardly with poor quality material.

According to CENAC (Centro de Estudios de la Construcción y el Desarrollo Urbano y Regional), three out of every five new homes built in Colombia today are of “informal origin”. In other words, 60 percent live in homes that are built without any legal procedures or formal design process.

Despite acknowledging the issue, city governments often lack the means to effectively deal with increasingly vulnerable housing stock. Cumbersome bureaucracies complicate matters. In some neighborhoods, city officials require over six months to approve the retrofit of a single home.

The result: hundreds of thousands of low-income families remain significantly at risk of death, injury and destitution in an earthquake.

Change Is Building

RMS has been working closely with Build Change since 2013. By sharing research, expertise and resources, we’ve been supporting the non-profit’s preventive programs in Latin America, the Caribbean, Nepal and, most recently, Southeast Asia.

The partnership, focused on promoting the benefits of retrofitting homes for low-income families living in informal neighborhoods, is closely aligned with RMS’ overarching, societal purpose. After all, for the last 30 years, RMS’ mission has remained the same: to make communities more resilient through a deeper understanding of the impacts of extremes.

With RMS’ support, Build Change has been able to develop the basis for successful retrofit projects. Shared value abounds…

The local governments have been convinced to effect and enforce changes to urban planning and building ordinances.

The local construction industry has been upskilled and employed.

The local insurers are finding new opportunities to offer affordable policies.

The local residents now have disaster-resilient homes and insurance coverage.

Quantifying Resilience; Increasing Institutional Urgency

Catastrophe risk models have been vital to this process. By combining science, technology, engineering and data to simulate the potential impacts of future disasters, RMS modeling puts a number on the potential impacts of “informal” housing. Moreover, the models can be used to evaluate how risk might reduce if mitigating measures are put in place.

A virtuous circle often results: quantifying the value of building practices drives funding; funding helps protect more communities; more communities protected demonstrates the value of resilient building practices; more funding follows.

For example, in 2016 RMS quantified the cost-effectiveness of a proposal for a scaled retrofit program in Bogotá, Colombia. Preliminary analysis showed that over 120,000 deaths and US$2.8 billion could be avoided in a 1-in-200-year event by retrofitting homes in the five neighborhoods studied.

RMS and Build Change also demonstrated that the project would deliver an attractive return on investment. Analysis showed that the retrofits could be completed using existing local skills, with minimal training, and for less than half the price of demolishing to rebuild.

In this case, the modeled output did not just increase the institutional urgency to deal with the problem of vulnerable housing. The analytics also contributed to the wider acceptance in Colombia of retrofitting as a viable solution.

Now What?

In approximately five years of formal partnership, RMS and Build Change have collaborated to greatly improve the safety of seismically-vulnerable communities. By combining our risk modeling expertise and institutional support with Build Change’s technical knowledge and grass roots approach, we’ve not only demonstrated that retrofitting in vulnerable neighborhoods is possible. We’ve also shown it’s a cost-effective way to save lives and livelihoods.

As a result, the Government of Colombia recently made the retrofitting of 600,000 homes an urgent, national priority.

Of course, our work in Latin America is by no means done. And collaborations with Build Change continue in Haiti and Nepal as well.

Immediate attention, however, has shifted to the Philippines. It’s too early to judge the outcomes. But with 69 million low-income people living in 15.6 million vulnerable homes today, the potential to make a difference is huge.

By quantifying that potential, we hope to develop a compelling business case to address what is arguably the issue of our age. By putting a number on the resilience dividend, we hope to attract the #ResilienceFinance needed to make some of the world’s most densely populate cities significantly safer.…

Almost one and a half million people have died in natural disasters over the past 20 years. This is a waste of life; a waste of potential.

Natural disasters also have a massive economic impact. Our models suggest natural catastrophes cost the world’s poorest countries almost US$30 billion a year on average. Hard-won development gains are regularly wiped out — and it is the poor and the vulnerable who are most impacted.

In case anyone had forgotten the crippling impacts of natural disasters, 2017 served a painful reminder. Hurricanes Irma and Maria left vulnerable people in the Caribbean devastated. Somalia, Ethiopia and Kenya struggled with drought. Floods and landslides wrecked lives and livelihoods in Sri Lanka and Bangladesh. And then there was Hurricane Harvey which, along with the California wildfires, made 2017 the costliest on record in the United States.

Whenever and wherever catastrophe strikes, our thoughts are with those so profoundly affected.

We did not, however, need last summer’s tropical cyclones to understand that something is not working. We did not need Irma and Maria to learn that investments in resilience reduce losses from natural disasters. And we did not need the events of 2017 to know that incentives are too often insufficient to drive action in the most vulnerable regions.

These truths are at heart of the Centre for Global Disaster Protection. Innovation is required to solve such complex humanitarian, political and economic problems. The impacts of recent disasters — and the need to finance reconstruction — have heightened the innovation imperative. They provide an opportunity to deploy financial instruments which catalyze investments in resilience; financial instruments which enable vulnerable communities to recover faster.

RMS too knows that it is possible to stop manufacturing natural disasters. And RMS knows that financial mechanisms could in theory securitize — and therefore incentivize — the potential “resilience dividends” from investments in disaster risk reduction. After all, RMS has been intimately involved in some of the best-known thought-leadership in this space.

Yet equally well understood is the fact that financial structures which incentivize resilience are difficult to implement in practice — in developed and in developing countries. There is no shortage of challenges.

To move from theory to practice; to redirect capital at the required scale, ideas need to be fleshed out, structures need to be robustly designed and cash flows need to be tested. Any new financial mechanisms must pass muster with all stakeholders, lest the intended benefits evaporate.

Since 1988, RMS’ mission has remained constant: to make communities and economies more resilient to shocks through a deeper understanding of catastrophes. Now, with the Centre’s help, experts from the finance, humanitarian and development communities have for the first time come together to refine financial instruments, address practical challenges and provide the interdisciplinary buy-in which mobilizes action.

In this collaborative environment, innovation has happened. The recent launch of a new report on Financial Instruments for Resilient Infrastructure is a product of that innovation.

RMS was commissioned by the U.K. Government’s Department for International Development to run the Centre for Global Disaster Protection’s first “Innovation Lab.” With support from Vivid Economics, re:focus partners and Lloyd’s of London two reports have been published — a 100-page technical report and a 50-page innovation report. Both are freely available here.

The four new financial mechanisms examined in the report can help monetize the resilience dividend, thereby incentivizing both resilient building practices and risk financing. The outcome: less physical damage, fewer lives lost and faster economic recovery whenever nature proves too much.

More is needed, of course. Policymakers and donors have a crucial role to play, not least in sponsoring pilots, funding the quantification of resilience, promoting risk-based pricing, supporting risk finance and advocating duties of care around life, livelihood and shelter.

Thankfully the significant public benefits of resilience justify the investment. And now we have four new financial instruments for donors and the market to pilot in real-world situations.…

Daniel has spent 20 years bringing new ideas to the risk industry. He has responsibility for driving innovative, strategic solutions across RMS’ entire client base. He is also the Global Head of RMS’ Public Sector Group, leading RMS’ relationships at all levels of government.

Daniel has worked closely with public and private entities around the world, advising them on a variety of complex risks, including natural hazards, environmental stresses, malicious attacks and pandemic outbreaks. Deeply committed to education, his work is motivated by a desire to make communities and economies more resilient to acute shocks.

Prior to RMS, Daniel managed the group strategy and development function at an 80,000-employee, £10 billion global healthcare group, serving 30 million customers in over 190 countries. He also has considerable start-up experience, having been a founding team member of an award-winning, SaaS company.

The driving force behind 'Resilience', he received a City of Miami Proclamation recognizing his commitment to delivering urban resilience in the face of sea-level rise and extreme flooding. Daniel has served on the management boards of several charities in areas as varied as education, disability, interfaith social cohesion, grassroots sport and the arts.

Daniel graduated from Oxford, double-first with Honours. He also studied for a Masters at the Humboldt in Berlin and is a graduate of the Center of Creative Leadership.