The debate over whether the Act should be extended a third time is likely to be acrimonious given partisan divides over financial legislation. If the renewal fails, the banking, construction, and insurance sectors will be impacted in a significant and troubling manner.

RMS: TRIA Program Highlights, August 2013

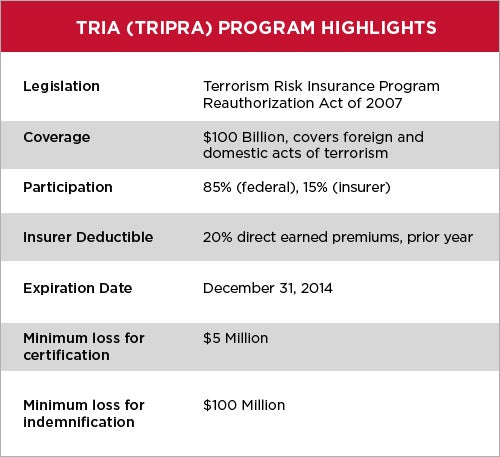

TRIA was first passed in 2002 and has since been extended and amended, twice. Each extension of the Act has led to tightened coverage by raising deductibles, increasing minimum losses, and reducing the pro-rata government share of losses (currently 85% of a $100 billion layer).

Sponsoring members from both parties have proposed the upcoming 2014 extension three times in Congress this year. This is a hopeful sign of bipartisan support. But the potential for strong opposition should not be underestimated.

Opponents of a TRIA renewal will be quick to label the legislation a “subsidy”. They will correctly point out that TRIA’s federal guarantee has been provided—and insurer money collected—for over ten years without incident. And opponents would be remiss to not mention the U.S. insurance industry surplus, which has grown to almost $600 billion as of this writing—compared to only $290 billion at the time of the September 11, 2001 attacks. From this, they will argue that the insurance industry is sufficiently capitalized to absorb the losses from a catastrophic terrorist incident without government assistance.

This argument against a further TRIA extension is likely to fall on the receptive ears of an electorate (and many freshman lawmakers) that has been galvanized by recent federal involvement in the financial and automotive sectors. In order to successfully counter this narrative, the parties’ case must be reframed to include a discussion of the public benefits of terrorism insurance, of which there are many.

Additionally, when the bill approached its first expiration in 2005, many property insurers inserted sunset clauses into their contracts, enabling them to alter or revoke terrorism cover in the event of a TRIA non-renewal.

The demand for financial protection against terrorism is as undeniable as the insurance industry’s reluctance to provide it.

The impact of a TRIA non-renewal would be felt the most by cities perceived to be appealing terrorist targets. The RMS® Probabilistic Terrorism Model classifies the most terrorist-prone cities as New York, Washington DC, Chicago, San Francisco, and Los Angeles.

Without TRIA, these cities can expect a shortage of terrorism insurance capacity and corresponding rate increases at the very least. At most, construction and lending activity will be compromised; and the economic consequences (lost jobs, stalled projects, missed opportunities) would surely follow.

TRIA must be viewed in the context of the government’s broader role in the insurance industry. In additional to terrorism insurance, the federal government provides billions of dollars annually in subsidized coverage for lines of business including flood, crop, mortgage, pension, and health— sometimes as a direct primary insurer, other times as a reinsurer.

Occasionally, as in the case of TRIA’s recoupment provision, the federal government’s role is similar to that of a bank, whereby losses are indemnified and then recovered, with interest, through future policy surcharges.

Is terrorism fundamentally different from other perils in regard to how the federal government should approach it?

What is public benefit of terrorism coverage, and can it be quantified?

Can the demand for coverage ever be met by private means alone?

These are critical questions, and they must be addressed directly and publicly by stakeholders in order to justify TRIA’s renewal.

Chris Folkman is a senior director of product management at RMS, where he is responsible for specialty lines including terrorism, casualty, wildfire, marine cargo, industrial facilities, and builders' risk. He has extensive experience on both the broker and carrier sides of insurance, where he has led many aspects of property and casualty operations including underwriting, pricing, predictive analytics, regulatory affairs, and third-party commercial coverage and claims.

Prior to RMS, he was a managing director at CompWest Insurance Company, a workers’ compensation start-up that was acquired by Blue Cross Blue Shield of Michigan. Chris holds a bachelor's degree from Stanford University. He is a licensed insurance broker and a Chartered Property and Casualty Underwriter (CPCU).